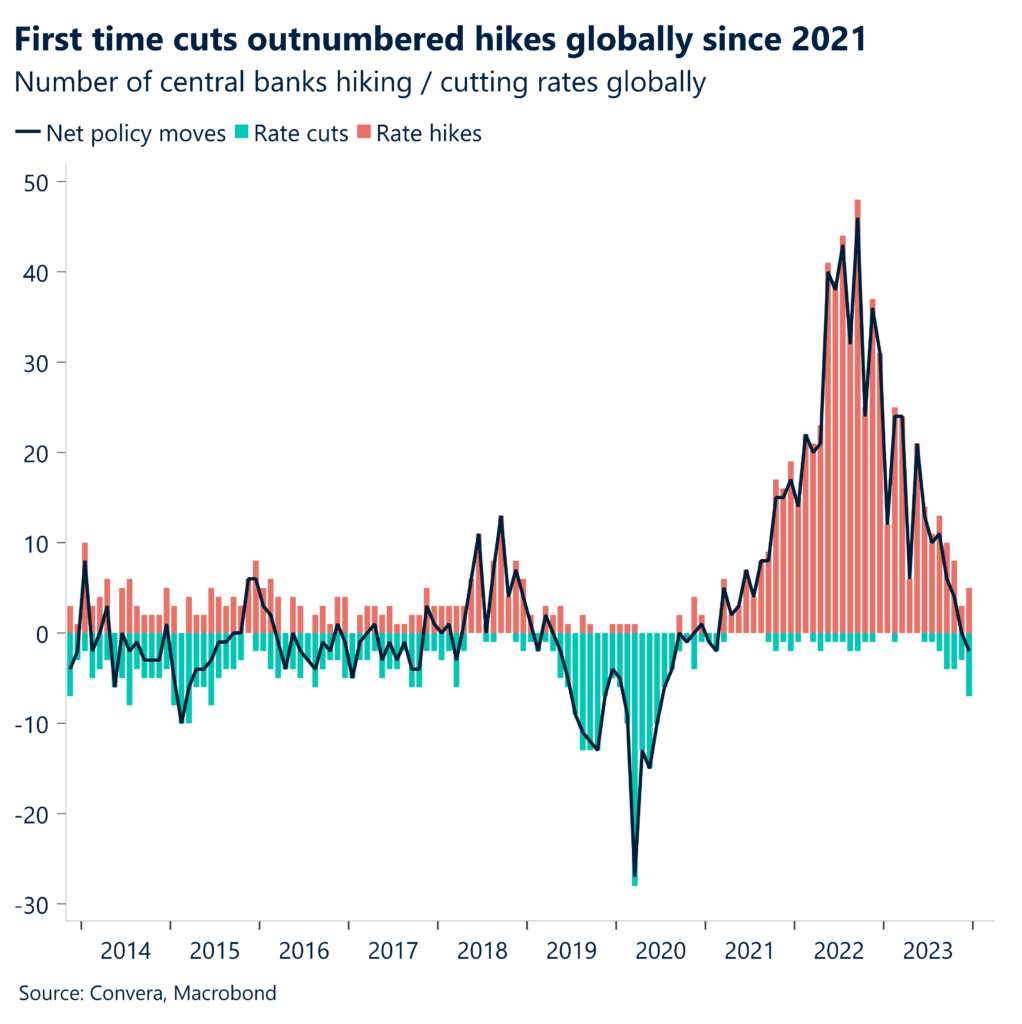

Global Macro The big picture

Most of the week has been about waiting on an event that didn’t cause any volatility in the end. US inflation remained hot but has not risen enough to change neither markets, nor the Fed’s perspective on monetary policy. Equities benefited from falling yields as FX markets remained muted. Geopolitics continues to make headlines, without impacting broader market pricing. It’s still all about the expected policy pivot from central banks. However, we see three risks emerging to the broad macro consensus.

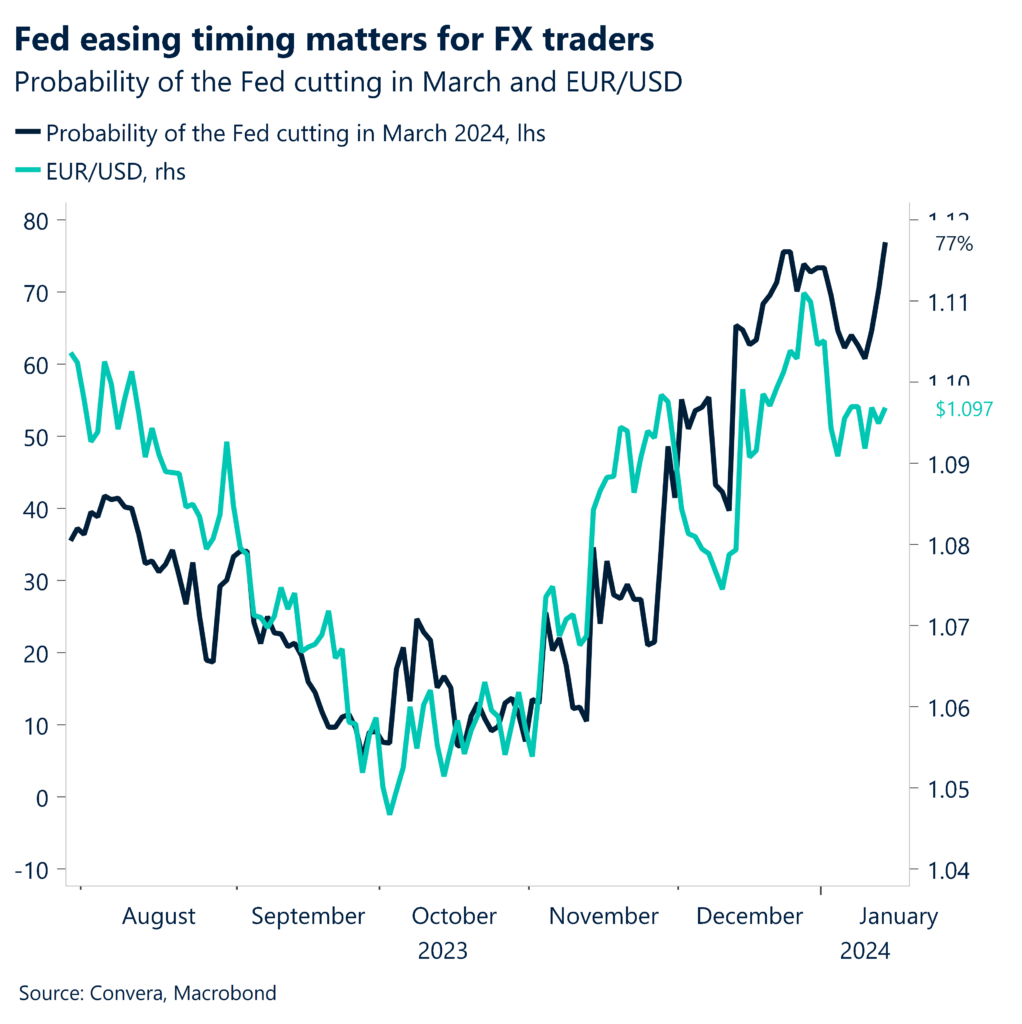

Entrenched positioning. The recent outperformance of US macro data in the form of the non-farm payrolls report and yesterday’s inflation print have made it less likely that the Federal Reserve would cut interest rates in March. While both data releases have been ambiguous and left room for interpretation, showing some pockets of continued weakness, the strong headline numbers will be enough for policy makers to push back against market pricing. Investors remain convinced of their believes and didn’t budge after yesterday’s data with six rate cuts still being priced in for 2024.

FX waiting on catalysts. The US dollar has been in a clear downward since November and has shed 4.7% of its value over the course of the past 12 weeks. While the Greenback has started the year strong, this week was more nuanced. The pound continued to outperform the broader market as the Australian dollar suffered from the effects of the last disinflationary print.

Intertwined risks. Looking for new catalysts for another breakout, we mention three (intertwined) risks to be aware of. (1) Inflation starting to trend higher again, (2) US growth underperforming expectations and (3) geopolitical tensions flaring up. We expect political uncertainty to pick up materially, given that uncertainty tends to rise in the months ahead of an US presidential election, peaking in the month of November.

Global Macro

Major events. US inflation, geopolitics and more

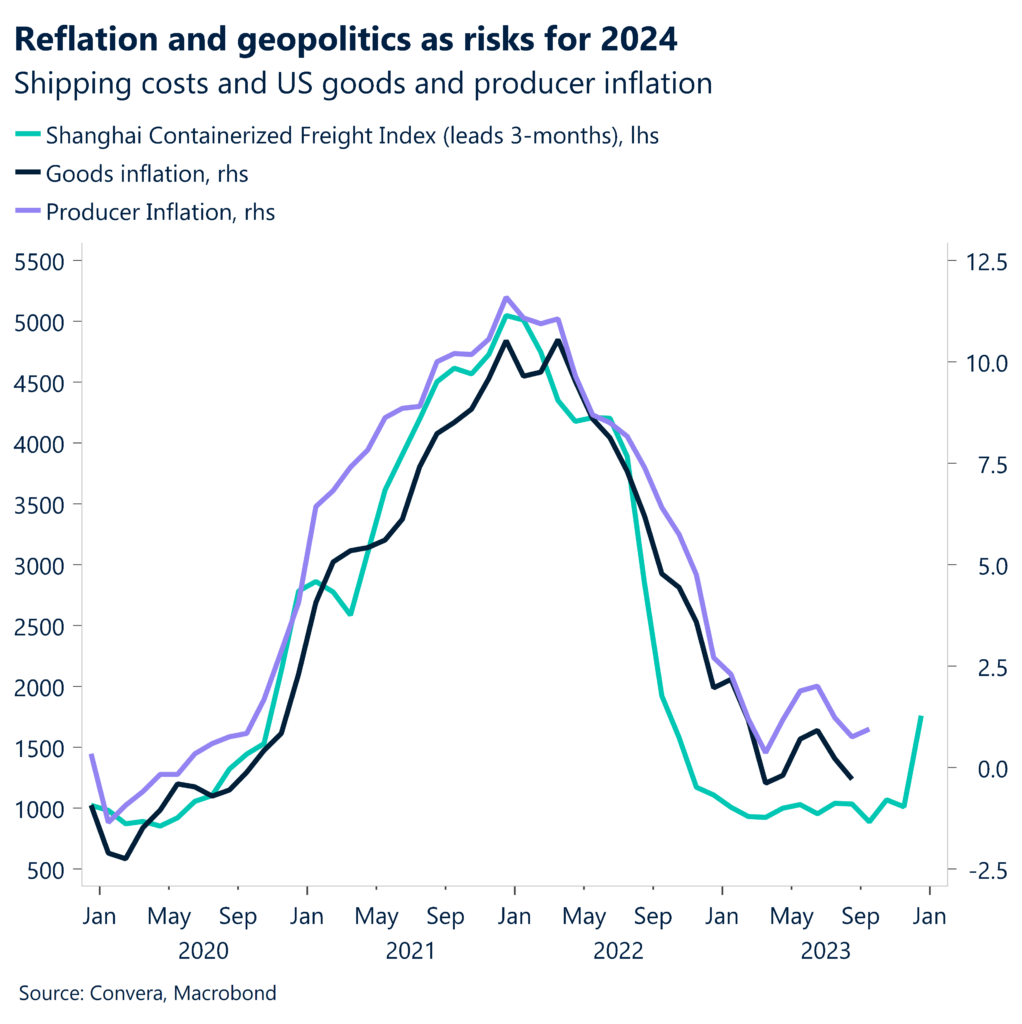

Shipping costs are rising. Markets are struggling to price in the implications of the US and UK launching strikes against Houthi rebels in Yemen, with the Iran-backed militia having already responded with confirmation of further escalations. This comes at a time when the conflict in the Red Sea has already put pressure on freight costs, which have been rising for some weeks now. This is the reason for why we have mentioned the reflationary scenario – inflation picking up over H1 – as one risk factor going into 2024. Especially against the backdrop of some leading indicators pointing to price and wage pressures starting to mount again.

2024 as the election year of the century. China will be important two-fold this year. The economic rise of China in the 21st century and its more aggressive stance on the global political stage have moved us to a bi-polar world. The war in Ukraine has been a prime example of the split that is forming between different groups of countries. The conclusion is that politically driven macro volatility will be something to watch out for. Especially given that the economic dependencies that have been strengthened by the globalization wave over the past 30 years have intertwined politics and economics. And with Taiwan voting on the upcoming weekend at a time when the world has never been as dependent on Taiwanese exports as now and with European and US elections coming up as well, this topic will stay with us during the year.

Strong inflation but no game-changer. Looking at this week’s anticipated macro highlight more closely, consumer prices came in hotter than expected. US inflation increased from 3.1% to 3.4% from a year earlier in December, beating expectations of a 3.2% rise. However, core inflation continued to fall, moderating to sub 4% levels. The 3-month annualized inflation rate has fallen to below 2% for the first time since 2020 in a sign that the CPI report has not been as bad as the headline would suggest.

UK economy returned to growth in November. The British economy returned to growth in the month of November, after having fallen in the previous period. The fall of economic activity in October raised fears about the UK falling into recession. However, Friday’s GDP report showing a monthly rise of 0.3% in November is in line with the recent recovery of the purchasing manager index and will be welcomed news for British policy makers. The 3-month average growth rate dipped into negative territory for the first time in 2023, after having been flat for two consecutive months. Both industrial and manufacturing production disappointed, with the former falling by 0.1% and the latter rising by less than expected (1.3% vs. 1.7% exp.)

Services strength. The British economy fared better than economists had expected at the end of last year, with the composite purchasing manager index rising for a second consecutive month in December. While the economy had not grown for two quarters in a row (Q2, Q3), it seems unlikely that the United Kingdom will fall into technical recession in Q4. The strength of the services sector has compensated for the weakness in industrial production and construction and has recently re-accelerated after some months of falling momentum.

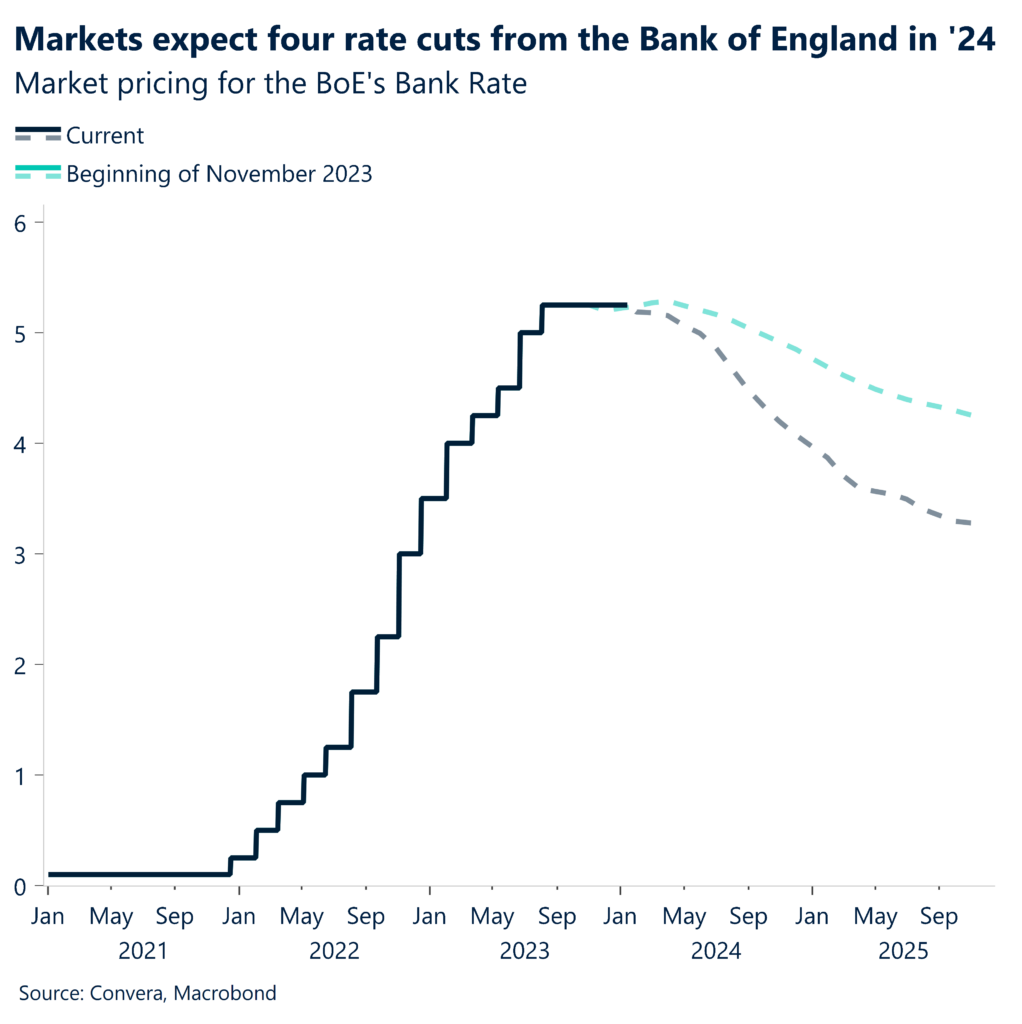

Inflation fall to justify rate cuts in May. However, we do not think that the UK is in a fundamentally different position than the US or Eurozone and see inflation falling back to the 2% target of the Bank of England around the middle of the year. We see a high probability of the BoE having to revise down its inflation forecast at the monetary policy meeting in February. This assumption is both driven by the fall of energy prices over the past few weeks and falling inflation expectations from key UK surveys. This will have implications for how investors will price the BoE’s policy path for 2024. We expect the MPC to start the monetary policy easing cycle in March with a 25-basis point cut, which could be followed by three additional cuts over the course of the year.

Rebound from historically low levels. In Europe, the Sentix Investor Confidence Index revealed that investors’ morale improved for a third straight month in December, signaling the region may be heading for a mild recovery. However, selling price expectations across all sectors increased and, apart from industry, remain significantly above their long-term average. Overall, the current situation remains fragile with momentum weak. The headline Sentix index has remained in a negative territory for a record of 23 consecutive months, superseding even pessimism post-GFC. In addition, retail sales in the Euro Area contracted by 0.3% m/m in November of 2023 to mark the sharpest decline in retail volume since August. On an annual basis, retail sales fell by 1.1%, marking the 14th consecutive contraction.

Lagged data continues to underperform. Contraction in German industrial production accelerated for a record sixth consecutive month in November by -0.7% m/m, missing market expectations of a 0.2% growth. The continued sharp drop-in activity in the construction sector is especially worrying. For the year, industrial production was down by close 5% in 2023 and is more than 9% below pre-pandemic levels. While the historically tight labour market will continue to support consumption, it complicates the matters for the European Central Bank (ECB) which is trying to gauge what impact continued tightness in the labour market will have on inflation. Several members of the Governing Council have stated that the ECB will first want to have a good view of the wage agreements in H1 of 2024 before it can kickstart policy easing.

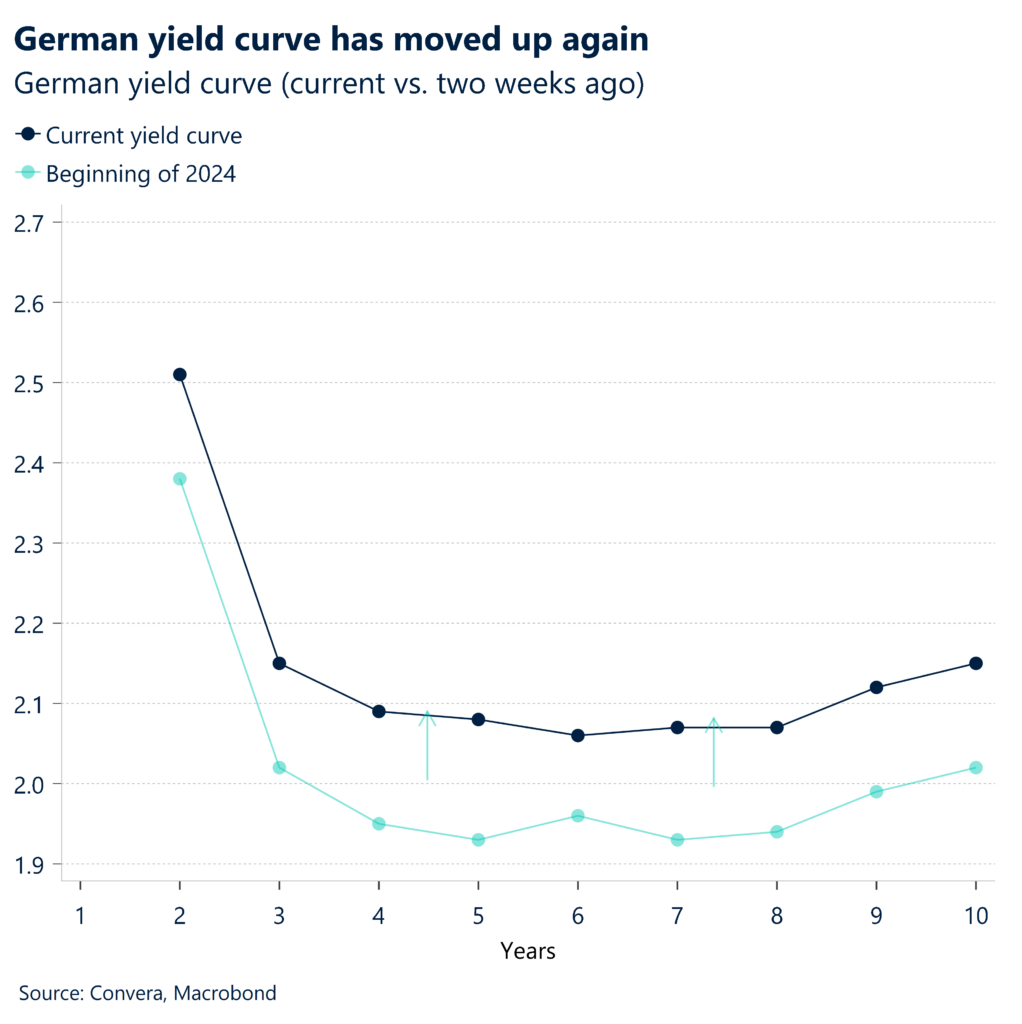

ECB pushes back against market pricing. The ECB is facing a tough dilemma during the January meeting in two weeks’ time over how early to start cutting rates when the economic outlook is fragile, and inflation remains above its 2% target. In parallel, Isabel Schnabel reinforced the message that the central bank remains data dependent and further evidence is needed before rate cuts can be discussed. Subsequently, markets downgraded their policy easing expectations are no longer pricing in a rate cut in the first quarter of 2024. Markets now see 145 basis points of rate cuts in 2024 with the first move coming in April, to be followed by a 25 basis point cuts at most if not all meetings this year.

Global Macro

The view ahead. Inflation and retail sales

Sticking to the consensus. This week’s data did little not nothing to dispel the markets believe of significant rate cuts from major central banks coming this year. Still, inflation has rebounded slightly in the US and Europe with the outperformance of the former and underperformance of the latter versus the global average having continued as well.

Geopolitics and macro data. Geopolitical developments will be closely watched as the situation in the Middle East evolves and Taiwan heads to the polls. Macro data will continue to matter as markets and central banks seem to have diverged on their views about the path of monetary policy. We will be focusing on labor market reports from the UK and Australia as GBP/AUD has risen 2% over the past three weeks on diverging macro stories. Inflation numbers from the UK, Canada and Japan. will be closely watched as well. For EUR/USD, Monday’s Eurozone industrial production and Tuesdays ZEW sentiment index will be followed by the more important US retail sales and industrial production numbers.

Macro risk events.

Monday (15.01) – EZ industrial production

Tuesday (16.01) – UK employment report, Eurozone ZEW sentiment, Canadian inflation

Wednesday (17.01) – Chinese GDP, UK inflation, US retail sales and industrial production

Thursday (18.01) – Australian employment, US housing data (permits, starts)

Friday (19.01) – Japanese inflation, UK retail sales, Canadian retail sales

All dates GMT

FX Views

Pound outperforms G10 space, AUD weaker

USD Retracing back despite positive data. The US dollar has lost some momentum this week, after recording its best yearly start since 2011. It seems that the Greenback is finding it hard to push higher against the backdrop of rising equity markets and stagnating government bond yields. The US Dollar Index has been in a clear downward since November and has shed 4.7% of its value over the course of the past 12 weeks. However, looking at the post-pandemic trading range of the Greenback between the 2021 low of 89.00 and 2022 high of 114.00, the current spot rate of 102 places the market comfortably in the middle of that range. Investors are not budging when it comes to pricing in aggressive rate cuts from the Fed and have mostly ignored the, on average, surprisingly strong incoming data.

EUR Broad euro strength across G10. The euro continues to benefit from expectations that the ECB will keep interest rates at record highs for some time, bolstered by the expected jump in Eurozone inflation last month and historically tight labour market conditions. Several Governing Council policymakers continue to push back against market’s aggressive policy rate cut expectations, highlighting that any talk of a rate cut before crucial first quarter wage data due in May would be premature. The common currency is set to end the week higher than all G10 currencies, apart from Sterling. EUR/GBP has slipped 0.9% so far this year and is trading close to four-week lows as lower rate cut expectations by BoE continue to support British bond yields, thus making sterling look relatively more attractive. EUR/JPY reached fresh 5-week high above ¥160 amid broad JPY weakness. Mixed price action sees EUR/USD ending the week marginally higher above $1.0950 threshold, with some modest downside risks.

GBP Topping the charts this week. The outperformance of the UK macro data, following both the PMI and GDP prints, did bode well for the pound. As we have outlined in the macro section, some weakness still lies ahead. However, that doesn’t necessarily mean that the pound will come under pressure from falling inflation, as long as global equity markets are rising due to the expectations of significant Fed rate cuts. The dollar dynamic is currently responsible for driving GBP/USD price action. And while slower inflation and sooner BoE rate cuts would put downside pressure on the pound, the US side of the equation will decide the short-term fate of the currency pair. Still, UK macro will most likely not be GBP positive over the next months. For now, the upward trend established back in November remains intact. A break above $1.28 is needed for further upside potential. The pound is the best performing G10 currency so far this week, having risen against all other currencies in this category. The macro driven strength of sterling continues.

AUD CPI growth slows. Australia’s CPI increased 4.3% year over year in November, compared to an expected 4.4% and 4.9% in October. It is the smallest annual growth since January 2022, according to the Australian Bureau of Statistics. After deducting volatile factors like holiday travel and car gasoline, it increased 4.8% year over year compared to 5.1% the previous year. A key indicator of core inflation, the trimmed mean, increased 4.6% year over year in November after rising 5.3% the month before. After the dovish FOMC statement in mid-December, the AUD/USD rise was stronger than anticipated, pushing out of the Aug-Nov base pattern and rising over 2023 channel resistance. The surge formed larger range support near 0.62. It will take breaks below the support zones of 0.6606-0.6642 to change the momentum of the fourth quarter trend. Key data to watch next week include Westpac Consumer Sentiment, Employment change, Unemployment Rate and Total Reserve Assets.

CNY PBoC may cut RRR soon. The chairman of the PBoC’s monetary policy department, Zou Lan, told the state-run Xinhua News Agency that the central bank may employ reserve requirements, medium-term lending facilities, and open market operations to give strong support for appropriate growth in credit. The statements increase chances of a 25-50bp decrease in reserve requirement ratio soon given similar comments were made in July last year before the September RRR cut. However, considering the shaky attitude in the market, greater policy catalysts are still needed, even though the prospect of an impending RRR drop can provide some respite. Following the fourth quarter downturn, we’re looking for another upward retracement for USD/CNH, with a minimum target zone close to the Aug-Nov pattern breakdown in the 7.2390-7.2665 range. Core focus for next week include GDP, Industrial Production, Retail Sales, and Unemployment Rate.

JPY Inflation cools, USD/JPY faces resistance. Japan’s headline CPI inflation for December in Tokyo dropped to 2.4% y/y from 2.6% last month, while the core CPI, which does not account for changes in the price of fresh food, was unchanged at 2.1% from 2.3% last month and was in line with forecasts. Thus, the figure is marginally above the BoJ’s 2% annual objective, which is a crucial factor in the central bank’s decision to begin tightening its extremely dovish stance. National inflation is predicted by the Tokyo CPI to follow a similar pattern and is expected on 19 January. The core CPI, which does not include gasoline or fresh food costs, decreased from 3.6% to 3.5%. While we anticipate the immediate harm to the economy to be minimal from the earthquake that struck the Noto Peninsula, we are still worried about a possible blow to inbound tourism and see a low possibility of a January rate rise. This also explains the steep decline of the yen following the catastrophe. Anticipated resistance at 146.10-147.48 is swiftly approached by the USD/JPY rebound from the late-year test of the 141.81 Sep-Nov pattern target and other surrounding support levels. This might provide a short-term top as the pair may reject this resistance zone. All eyes will be on PPI, Core Machinery Orders, Industrial Production, and National Core CPI.

CAD Oil price surge rescues Loonie. The Canadian dollar is looking to end the week on a positive note as higher oil prices offset US dollar strength. Earlier in the week, CAD weakened to a fresh three-week low of $1.3442 against the US dollar amid hotter-than expected US inflation print for December and a downside surprise to the weekly jobless claims report. However, the Greenback surrendered its gains soon after as sustained bullish positive movement in oil prices supported the Loonie. Crude oil surged to a two-week high past the $74/barrel mark attributed to escalating tensions in the Middle East following military attacks by the US and UK on Iran-backed Houthi locations in Yemen on Thursday night. The 14-day SMA of $1.3311 is seen as the immediate support for the USD/CAD pair. If this level is breached, it could potentially lead the pair to test the psychological level at $1.3300, with further downside potential towards the major support at the $1.3250 level.