Low volatility spurs risk-on. Cross-market volatility levels remain compressed as expectations of early rate cuts from the Federal Reserve (Fed) sway. Despite hawkish repricing after the blowout US jobs report at the start of February, US equity benchmarks continue to record fresh record highs, with the S&P500 hitting the psychological 5000 level. Upbeat corporate earnings and easing geopolitical fears along with calm conditions in bond markets, likely helped risk appetite remain cautiously upbeat. The US inflation revisions at the end of the week also turned out to be a damp squib. A raft of top-tier data points due next week could shake things up though, particularly if yields advance further following this consolidation period.

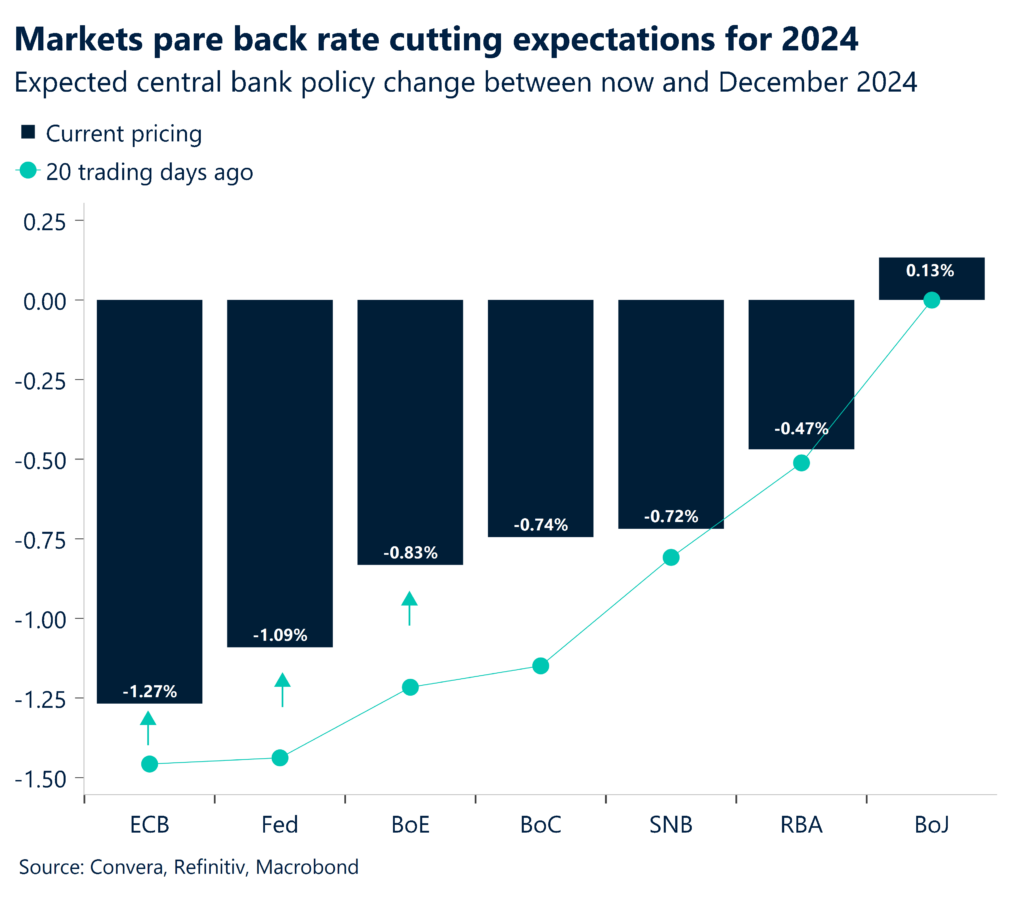

March cut off the table? The Fed is in a holding pattern and the likelihood of a rate cut in March is priced at less than 20%, a significant decrease from the approximately two-thirds chance anticipated at the beginning of the year. This week, yet more US economic data has surprised on a positive note supporting this narrative, though yields remain stable. The services sector expanded in January by the most in four months and the key employment component jumped back above 50, which separates expansion from contraction. Comments from several Fed officials also reinforced the view the Fed will not cut interest rates as soon as next month, but markets are still pricing significant easing for 2024.

China’s troubles are growing. Despite reaching its growth target for 2023, sentiment remains downbeat heading into the Lunar New Year. Consumer spending power is weak, and a real estate slump has dented confidence. Meanwhile, Chinese authorities introduced an array of measures, like cracking down on short-selling, in a bid to temper the bruising equity sell-off which dragged the CSI300 to five-year lows. China stocks have rebounded since, but the mood remains fragile as the Chinese economy continues to grapple with a property crisis, declining demand, and foreign outflows.

Global Macro

Central banks push back against markets

Surprise hawkish tone from RBA. The Reserve Bank of Australia (RBA) kept its cash rates unchanged at 4.35% during its first meeting in 2024, as widely expected. The RBA acknowledged that inflation has eased more than expected in the fourth quarter but was uncertain on when inflation would return to its 2-3% target and did not rule out further hikes if needed. The slight hawkish surprise saw rate cutting expectations for 2024 pared back slightly. Markets are pricing just over 40 basis points of easing this year, much less than economies like the US or UK, and this should help the Australian dollar recover through the year.

BoJ rules out rapid rate hikes. Deputy Governor Shinichi Uchida of the Bank of Japan (BoJ) signaled that any policy tightening would be gradual. Perhaps not a surprise as the latest Tokyo core CPI data has fallen below 2% for the first time since May 2022. Although the high-ranking official indicated an end to negative rates is coming, Japanese government bond yields fell across maturities and the Japanese yen came under renewed selling pressure. Low volatility levels are also encouraging carry trades, borrowing low yielding currencies like the yen to invest in higher yielding assets. These calm conditions may continue weighing on the yen going forward.

Deflation fears are rising. China’s consumer prices fell by 0.8% y/y in January 2024, the steepest decrease in more than 14 years, and food prices declining at a record pace. Prices have fallen for three consecutive quarters, the longest deflationary streak since the Asian Financial Crisis in the late 1990s. Could this be the bottom though? China is expected to boost fiscal stimulus again this year, but its plans won’t be clear until a national budget is released in March. The Chinese economy’s ongoing slowdown has seen the Chinese yuan weaken with the USD/CNH near three-month highs.

Europe’s bottoming out. Europe’s STOXX 50 continued to hover at 23-year highs and German 10-year bond yield stabilized around 2.3% in the aftermath of the largest two-day sell-off in almost a year. European economic data came in mixed, exposing a weakened domestic European economy. On the one hand, survey data from the ECB revealed that Eurozone consumers reduced their expectations for inflation over the next 12 months in December to 3.2%, marking the lowest level since February 2022. Meanwhile, retail sales in the bloc fell the most in a year, dropping by 1.1% m/m in December 2023. Nevertheless, the Sentix investor confidence index revealed that Eurozone investors’ morale improved for the fourth straight month in February, the highest level since April, signalling the region is heading for a mild recovery.

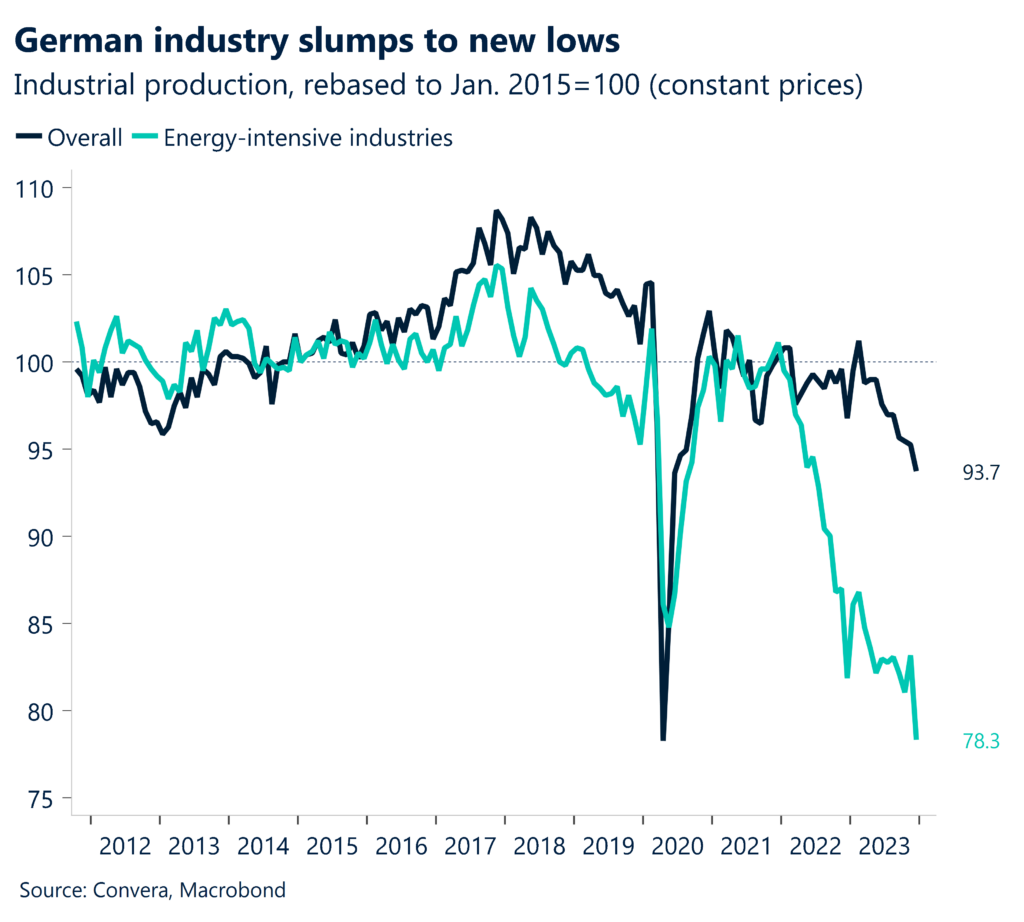

Germany still sick though. However, deepening pessimism in Germany remains a concern as the country remains a drag on the region, pointing to a persistent economic crisis in the country. Its economy has shown no growth in the best part of two years. German industrial output contracted for a fourth month running in December 2023, but markets largely ignored as the lagging indicator fit into the same story we have seen thus far, namely that the bloc’s largest economy landed itself into a recession setting in 2023. On a brighter note, German factory orders surged by 8.9% m/m in December, the most in over three years, driven by “an exceptionally” high number of aircraft orders

More evidence supporting BoE hold. New UK labour market data revealed the unemployment rate was 3.9% in the three months through November, well below the 4.2% estimated using previous data. As the labour market has not loosened as much as thought, possibly putting more upward pressure on wages and prices, this might persuade the Bank of England (BoE) to wait a few more months before starting to cut interest rates. Further supporting this hawkish story is the fact British house prices rose 2.5% in the year to January, the strongest annual growth rate for a year, providing tentative signs of recovering momentum in the housing market.

NZ hikes back in play. While central bankers around the world were pushing back on rate cut hopes, traders in New Zealand are worried about further hikes after another hot employment result. The NZ employment market grew by 0.4% in the December quarter while the unemployment rate came in at 4.0% versus expectations for 4.3%. Importantly, wages are also putting pressure on the RBNZ, with the labour cost index up 1.0% in the December quarter – up from 0.8% in the September quarter. The RBNZ next meets on 28 February. NZ money markets see a 40% chance of a hike (source: Refinitiv).

BoC joins the “pushback” party. Bank of Canada (BoC) governor Tiff Macklem echoed recent comments from other major central banks and said while rate hikes have slowed demand, monetary policy needs to remain tight and more time is required to bring down inflation. Headline annual inflation climbed from 3.1% to 3.4% in December.

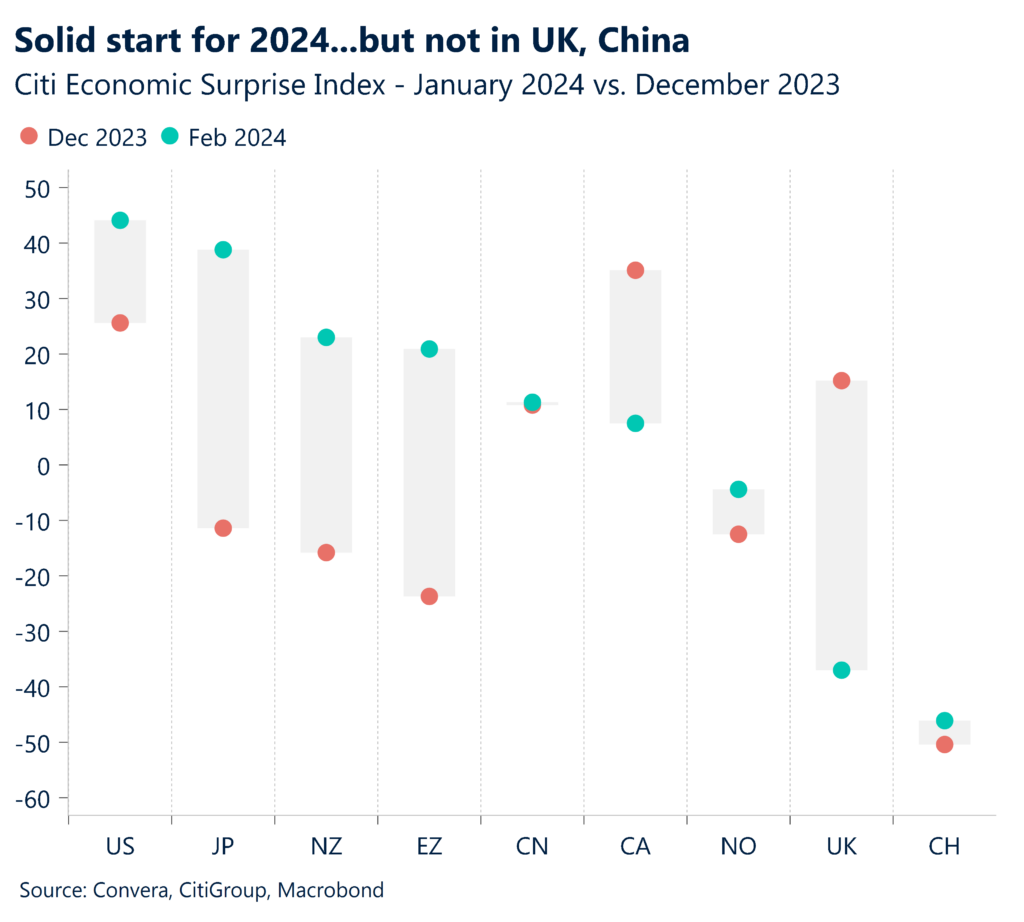

“Doctor Copper” at three-month lows. While we’ve seen an improvement in the key surprise indexes in 2024 – thanks to a pick-up in growth for the US, Eurozone and Japan – other indicators aren’t providing the same positive signal. Notably, copper, famed for its sensitivity to growth expectations, plunged to three-month lows this week. The ongoing weakness in China might be to blame – or maybe “Doctor Copper” is telling us that high interest rates are starting to bite.

Global Macro

US, UK CPI more important than ever

Inflation crucial for central bank moves. This week’s inflation numbers in the US and UK will be critical in determining the next steps from the Fed and BoE. US headline CPI has oscillated between 3.0% 4.0% for the last six months and explains why markets are convinced the Fed has the ability to cut interest rates sooner rather than later. UK headline CPI, on the other hand, was at 6.7% just back in September, and signals that UK authorities are likely to be much more cautious.

Wages the other part of the puzzle. While inflation is key this week, wages data helps provide more detail on the outlook for central banks. UK jobs data will be closely watched, while the US’s weekly unemployment claims has become more important after the US’s huge January US jobs report.

Retail sales likely to be soft. US consumer spending has been a major bright spot, but a modest softening is expected, whilst in the UK, it looks like the plunge in retail sales in December might have been enough to nudge the economy into another very slight contraction. No sign of recovery in January will raise recession fears.

Macro risk events.

Monday (12.02) – US consumer inflation expectations

Tuesday (13.02) – UK jobs report & US CPI

Wednesday (14.02) – UK inflation & EZ Q4 GDP

Thursday (15.02) – UK Q4 GDP & US retail sales

Friday (16.02) – UK retail sales & US sentiment index

All dates GMT

FX Views

Sleepy scenes in the currency space

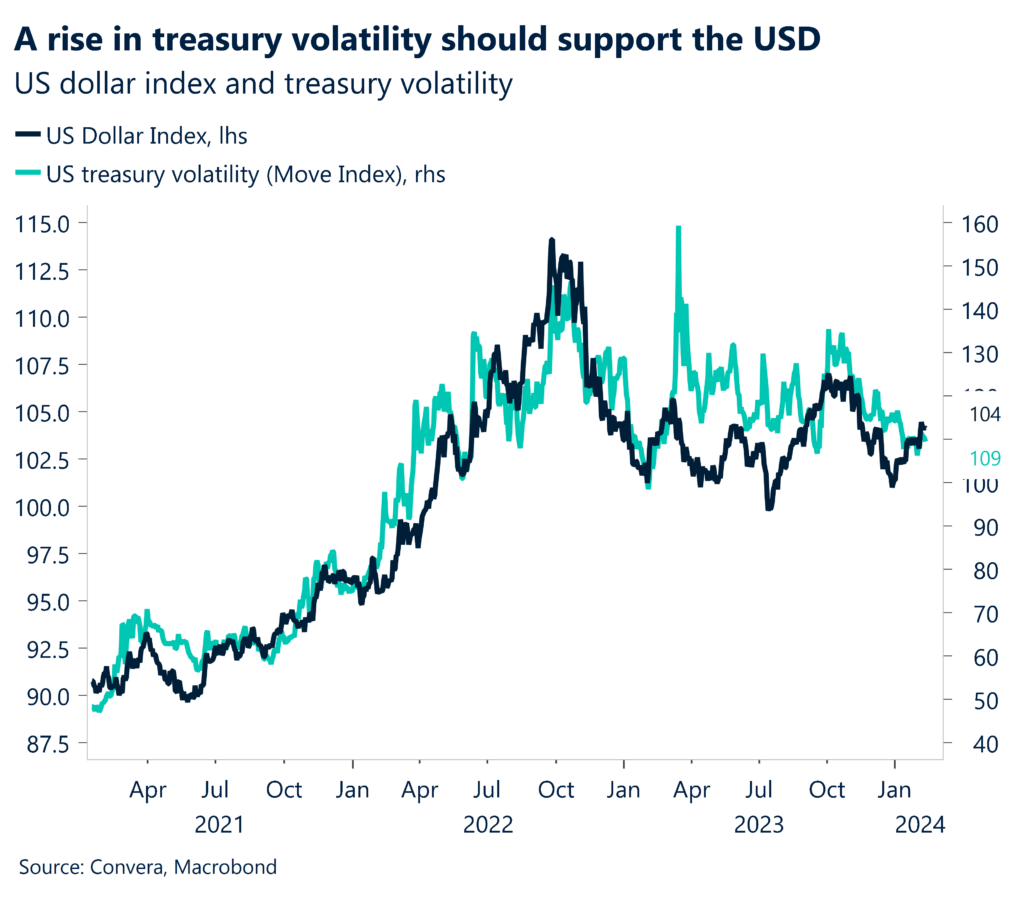

USD Holds onto its crown. A quiet week in FX markets has seen the US dollar surrender about 40% of its gains made in the wake of last Friday’s strong jobs report, though the Greenback remains the top-performing major currency year-to-date. The lukewarm risk-on climate, helped by hopes of an Israeli-Hamas ceasefire, has dented dollar demand somewhat, but the DXY is still primed for a modest weekly uplift, supported by slightly higher US yields. We see upside risks in yields though and a spike in volatility could support the dollar further. These low volatility periods also encourage interest in carry trade strategies, helping the USD gain more ground against low-yielding peers like the yen, which makes up almost 14% of the USD index. But with 1-week implied volatility spiking after capturing flash US inflation data next week, we expect some choppy price action as expectations of early easing from the Fed continue to ebb and flow. Any dollar weakness may be limited though as the China Lunar New Year holiday may see investors reluctant to carry short dollar positions in an uncertain geopolitical environment.

EUR ECB April rate cut a coin-toss. Earlier in the week, EUR/USD touched a fresh 13-week low at $1.0721 and Germany’s 10-year bond yield surged by 18bps over Friday and Monday combined – the largest two-day uptick since the SVB crisis March 2023 – as the unwinding of early Fed interest rate cut bets continues to favour the Greenback. Investors have pulled back on rate easing expectations across board, with the market implied probability of an ECB April rate cut dropping to 51%. Cumulative rate cuts bets fell to115bps worth of easing by year-end, down from 140bps from the beginning of the week. The rest of the week can be characterized by an unusual spell of calm, as weekly EUR/USD volatility fell close to a 5 ½ year low. Mixed European data was not enough for euro to break past the 100-day SMA barrier at $1.0786. For now, we are in a new EUR/USD holding pattern at slowly lower levels, with the pair looking to close lower for the fourth consecutive week- the longest bearish streak since end of August 2023. Across CEE markets, EUR/CZK surged to the highest level since May 2022 as CNB cut policy rates for the second time.

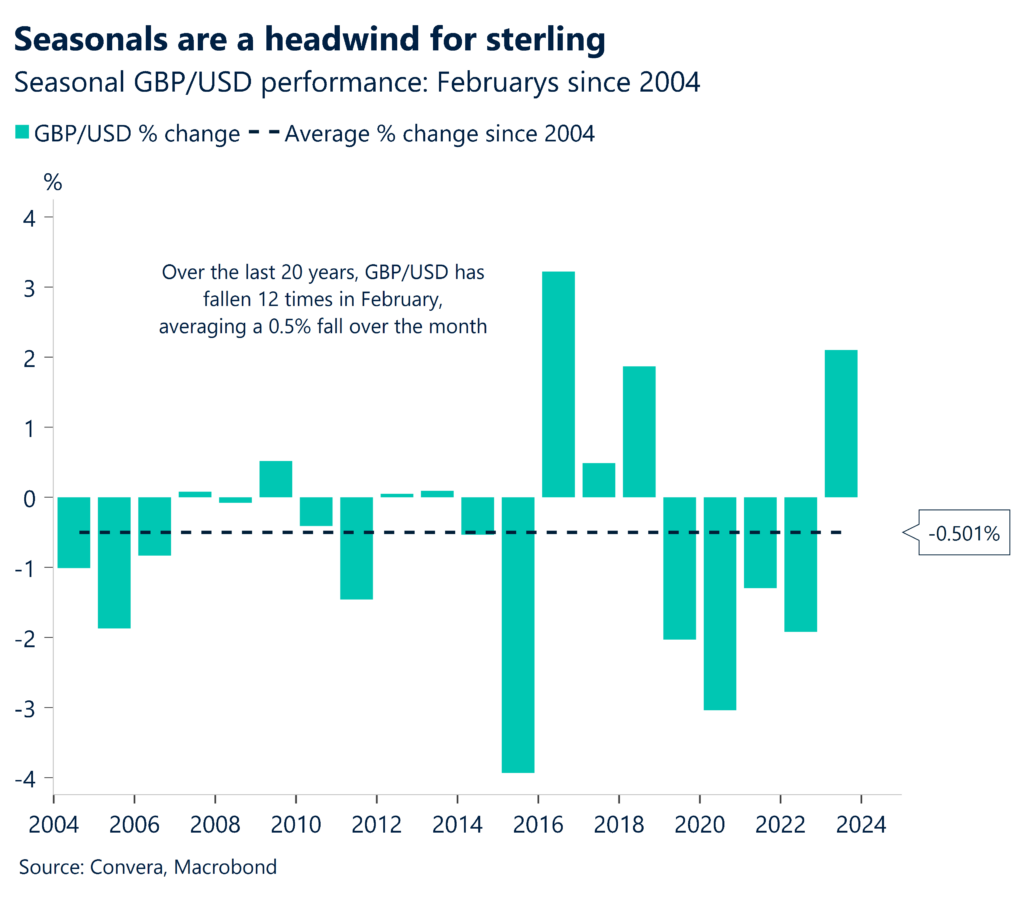

GBP Big week awaits. The pound is battling for a weekly rise against the US dollar but still nursing losses endured after stronger-than-expected US data this month. GBP/USD found support at its 200-day moving average, but downside risks still linger in the short-term due to growth differentials favouring the buck. On a more positive note, although the pound has lost around 1% in value against the dollar so far this year, it is still the best-performer among the G10 universe of major currencies. In fact, the pound is looking to clinch its seventh straight week of gains versus the euro as investors grow more convinced by the BoE’s determination to keep interest rates where they are for now. Next week could be a critical week for sterling’s direction as the UK jobs report, inflation, GDP and retail sales data are published – all of which will influence BoE policy and thus market implied rate expectations which have been a key driver of FX volatility. We note seasonal headwinds for sterling should also be considered as GBP/USD has, on average, fallen 0.5% in this month over the past 20 years.

CHF Slides to 2-month low. The Swiss franc depreciated past 0.87 per USD this week, the lowest in nearly two months. As well as broad-based USD strength, tentatively improving global risk sentiment, helped by low levels of cross-asset volatility, weighed on the longstanding safe haven swissy. Domestically, SNB Chairman Jordan noted that the central bank’s inflation expectations increased for the year, but the baseline scenario has inflation remaining below the 2% target, setting up the environment for looser policy. The franc has been supported by repeated foreign exchange selling by the SNB during this global tightening cycle, with reserves still standing near seven-year lows. However, with inflation falling globally and an end to the tightening cycle in sight, the tide is turning for the franc. Since hitting 9-year highs against both USD and EUR late last year, CHF is now 5% and 2% weaker respectively. Switzerland’s inflation report next week is expected to show consumer price growth has slowed to its lowest rate in two years, which could further weigh on the franc.

CNY Sour mood before holidays. It’s been a turbulent week for Chinese assets, with stocks falling to 5-year lows, although authorities announced a slew of measures to arrest the decline. That said, the selloff in Chinese equities did not translate into a bigger selloff in the yuan so it suggests markets are slowly coming to compartmentalise some of these Chinese equity risks. Meanwhile, economic risks continue to burden. Deflation fears are rising and although the services sector remains in expansionary territory, activity is slowing. Manufacturing has contracted for four consecutive months, fitting the broader trend of consumers favoring services over goods spending post-reopening. USD/CNH is nearing initial upside targets (re Weekly Jan 19th publication: targeting 7.239-7.2665 resistance) after consolidating between November-January. Next week’s data calendar is light amid Lunar New Year celebrations.

JPY BoJ talk dampens yen demand. The Japanese yen is this week’s worst performer, with investors reacting to comments made by BoJ policymakers. Governor Kazuo Ueda said on Friday there was a high chance for easy monetary conditions to persist even after the central bank ends negative interest rate policy. The yen slipped to a 10-week low and USD/JPY is now 6% higher year-to-date. The BoJ must now weigh the weak labor earnings against potential spring wage hikes. USD/JPY has bounced from 145.45-146.97 support but faces upside resistance around 149.442-150.80. Key upcoming data includes PPI, GDP, and industrial production.

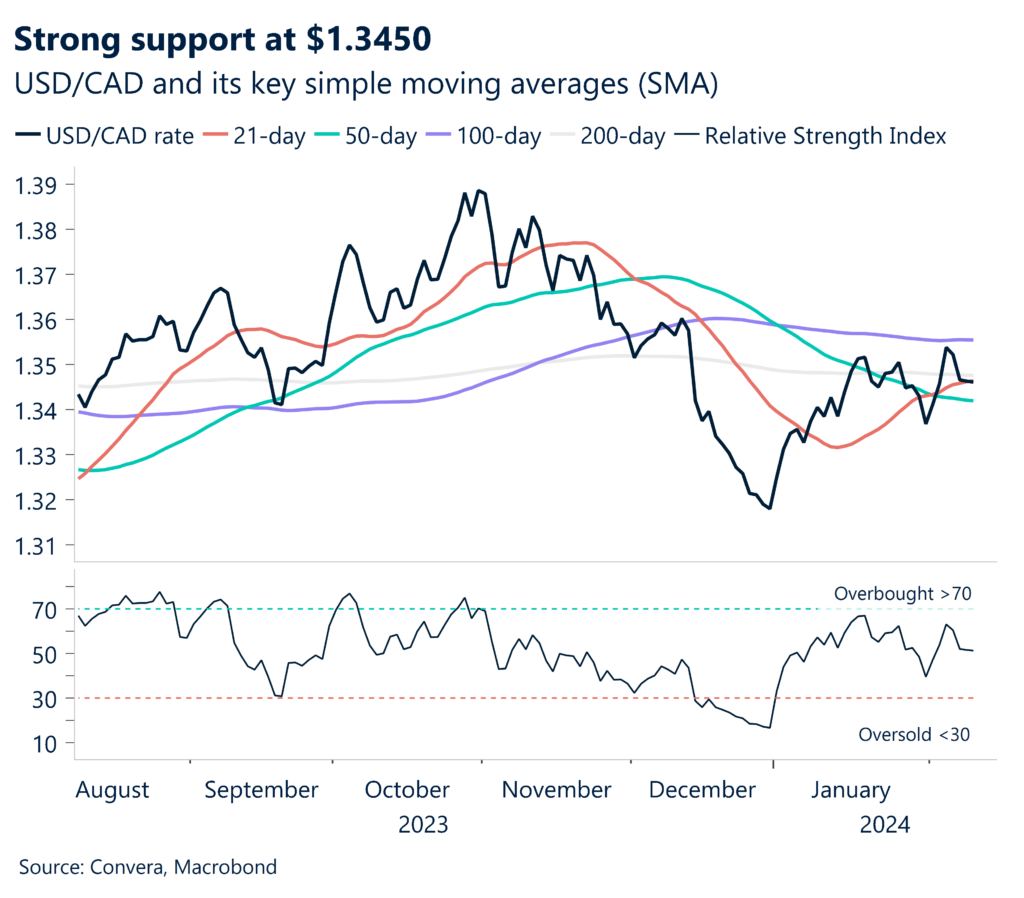

CAD Bounces sharply from 8-week low. USD/CAD kicked off the week near an 8-week high amid broad based Greenback strength. Canada’s 10-year bond yield surged by 24bps over Friday and Monday combined – the largest increase in 4-months – driven by cautious sentiments from Fed officials regarding rate cuts, coupled with robust US data releases. Resistance was met at its 100-day moving average though and demand for the CAD rebounded, helped by rising oil prices. Canadian dollar sentiment also flipped from bearish to bullish on hawkish BoC’s Governor Tiff Macklem comments with the Loonie ending a 5-week losing streak versus the Greenback. USD/CAD has remained range bound between $1.3350 – $1.3551 for the past four week, but next week’s US core CPI print might spark a breakout either way depending on any big deviations higher or lower than the consensus forecast.

AUD 3-month low despite hawkish RBA. The Australian dollar touched a 3-month low against the USD this week despite an overall hawkish policy tilt by the RBA. The RBA lowered its 2024 GDP growth forecasts but still expects rates to reach 3.9% by year-end, in line with market pricing. AUD initially reacted higher but pared gains as investors digested the nuances of the statement. Concerns about China’s economy also provided an excuse to sell the Aussie given it’s a proxy for Chinese growth expectations. The Aussie staged a strong recovery by week-end though and looked to snap a 5-week losing streak. Key data to watch next week includes Westpac consumer sentiment, unemployment, and NAB business confidence. Tactically, AUD/USD aims to reverse recent weakness but faces resistance around 0.664-0.6657.