The US dollar rebounded from the six-week lows seen in the middle of May with another round of stronger-than-expected US economic data underlining that US growth remains exceptional.

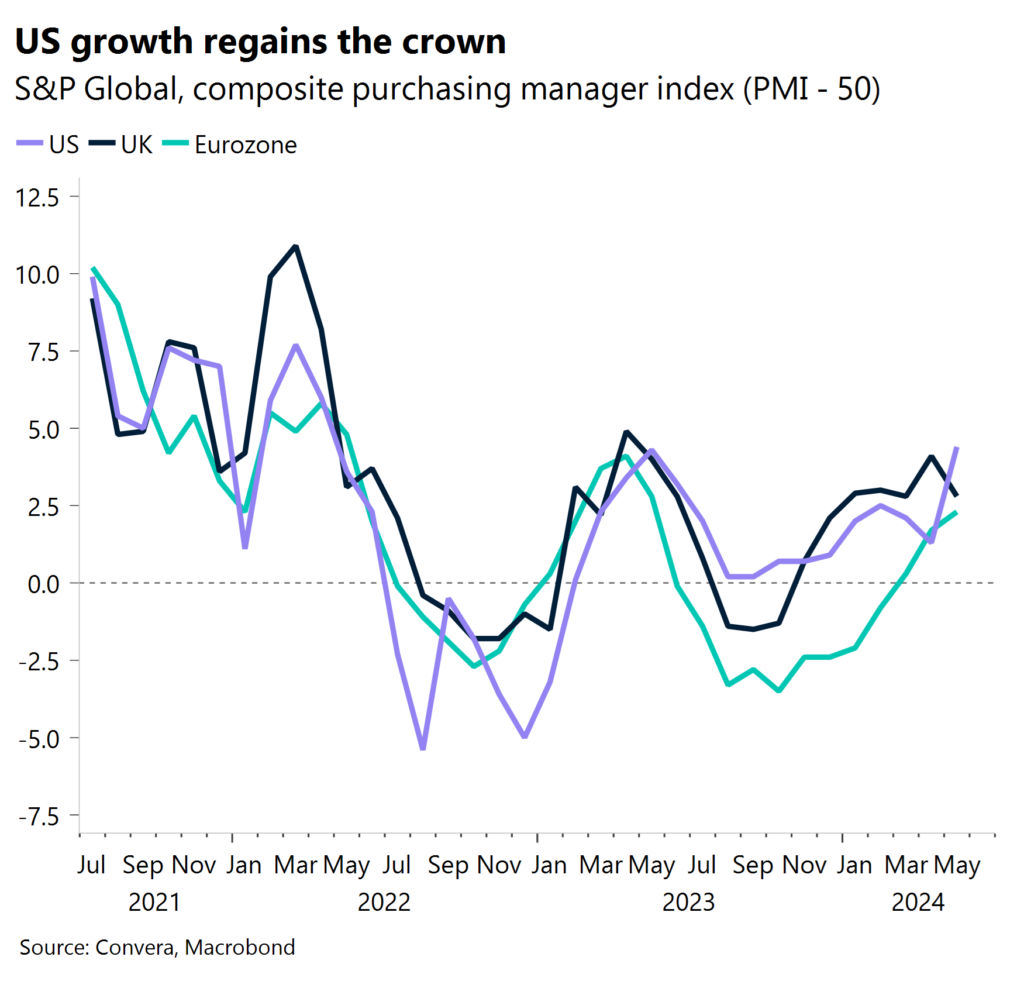

US purchasing manager index (PMI) numbers sharply beat expectations with the manufacturing PMI at 50.9 versus 50.0 expected while the services produced a massive result – at 54.8 versus 51.2 expected. The PMI numbers were another example of the US economy’s outperformance – recently less impressive but still markedly stronger than its peers.

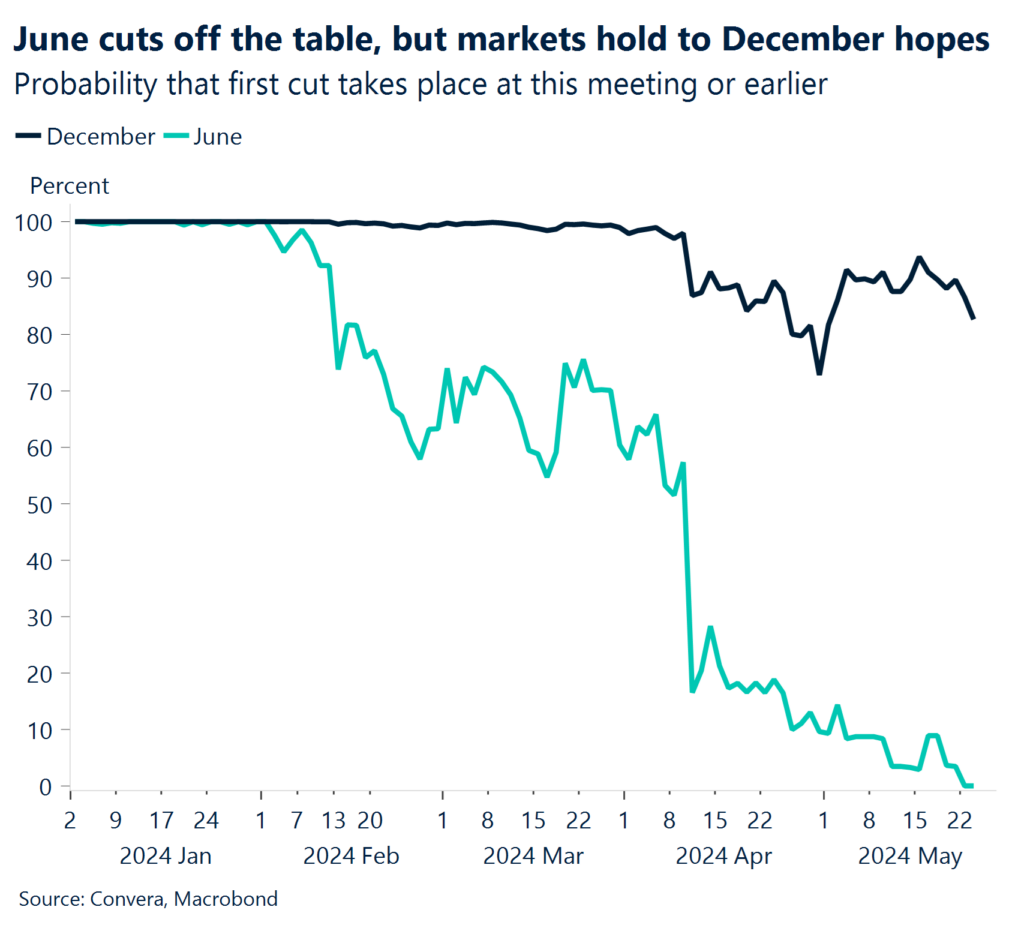

US money markets now have only one 25-basis point rate cut fully priced in by the end of 2024 (source: Reuters). Falling rate cut expectations have boosted the greenback this week with the USD index seeing a four-day winning streak.

The British pound was initially stronger after UK Conservative Prime Minister Rishi Sunak called a snap general election for 4 July that seems likely to see a change of government. Sunak was required to hold an election by January 2025 and is currently 20 points behind the opposition Labour party.

NZD/USD jumped to two-month highs after Reserve Bank of New Zealand decision, but the move was short-lived. The RBNZ said it considered raising rates and that sticky inflation means the central bank might need to tighten policy further – another sign that inflation remains persistent and rate cuts might be some time away.

Regional outlook: US

Don’t doubt US growth story

US reaccelerates in May. The US PMI numbers dominated the macro picture over the last week with the manufacturing index climbing back above the boom-bust level of 50 (at 50.9) after briefly dipping below this level in April. The services sector saw a sharp acceleration – jumping from 51.3 in April to 54.8 in May. The services number was the best result since May 2023.

US jobs also show improvement. US jobs numbers also improved with the weekly unemployment claims falling from 223k to 215k over the last week. This was the first weekly claims result to beat expectations since last April.

US shares ease but earnings remain buoyant. The global equity story remains buoyant after a bumper result from AI chipmaker Nvidia — the last of the so-called “Magnificent Seven” technology stocks to report after the companies fuelled a 27% rally in the S&P 500 over the last year. US shares saw a sharp sell-off mid-week, however.

Fed talks tough. The week also saw a heavy calendar of Federal Reserve speakers that mainly indicated that interest rates would likely need to remain higher for longer. The Fed minutes, mid-week, noted “that it would take longer than previously anticipated for them to gain greater confidence that inflation was moving sustainably toward 2 per cent.”

Regional outlook: UK

Election risk overshadowed by inflation

Election clock ticks. The big news out of the UK is that Prime Minister Rishi Sunak announced a general election to take place on 4 July, much sooner than many had anticipated. Opinion polls suggest a win for the opposition Labour party, which has held a steady lead of around 20 percentage points over Mr Sunak’s Conservatives since the turn of the year. While markets usually prefer continuity over change, it seems a Labour government is expected to usher in a period of political stability and the prospect of a tighter relationship with the EU will help to unwind at least some of the pound’s Brexit discount. Plus, the Labour party’s shift to a more pro-business, center-ground position could further support sterling.

Sticky services inflation. Arguably more important for the pound was the fact UK inflation neared the Bank of England’s (BoE) 2% target but failed to slow as much as expected. Headline annual inflation came in at 2.3% (versus 2.1% expected) and core inflation at 3.9% (versus 3.6% expected). Services inflation, which the BoE is watching carefully, was expected to slow to 5.5%, but remained little changed at 5.9% after a 6% reading the month before. This is important and is the main reason why a June rate cut might be off the table, sending UK yields surging higher and lifting GBP to multi-month highs.

June rate cut off the table? We shouldn’t assume the Bank of England (BoE) won’t cut rates in June just because there’s an election coming. A rate cut has been telegraphed long before the election was called, but the higher-than-expected services inflation sent the probability of a June rate cut from 50% to 10%. Money markets now only price in 12 basis points of easing by August, down from 25 basis points before the inflation report.

Regional outlook: Eurozone

Wage growth reinflation sends a note of caution

Recovery gains momentum. The flash HCOB Eurozone Composite PMI rose to 52.3 in May, the highest reading in a year, exceeding the market consensus of 52. Faster increases in business activity, new orders, and employment lifted the headline index, while business confidence hit a 27-month high. Meanwhile, rates of inflation for both input costs and output prices softened but remained above pre-pandemic averages. Growth continued to be centered on the services sector, but the manufacturing sector edged closer to stabilisation.

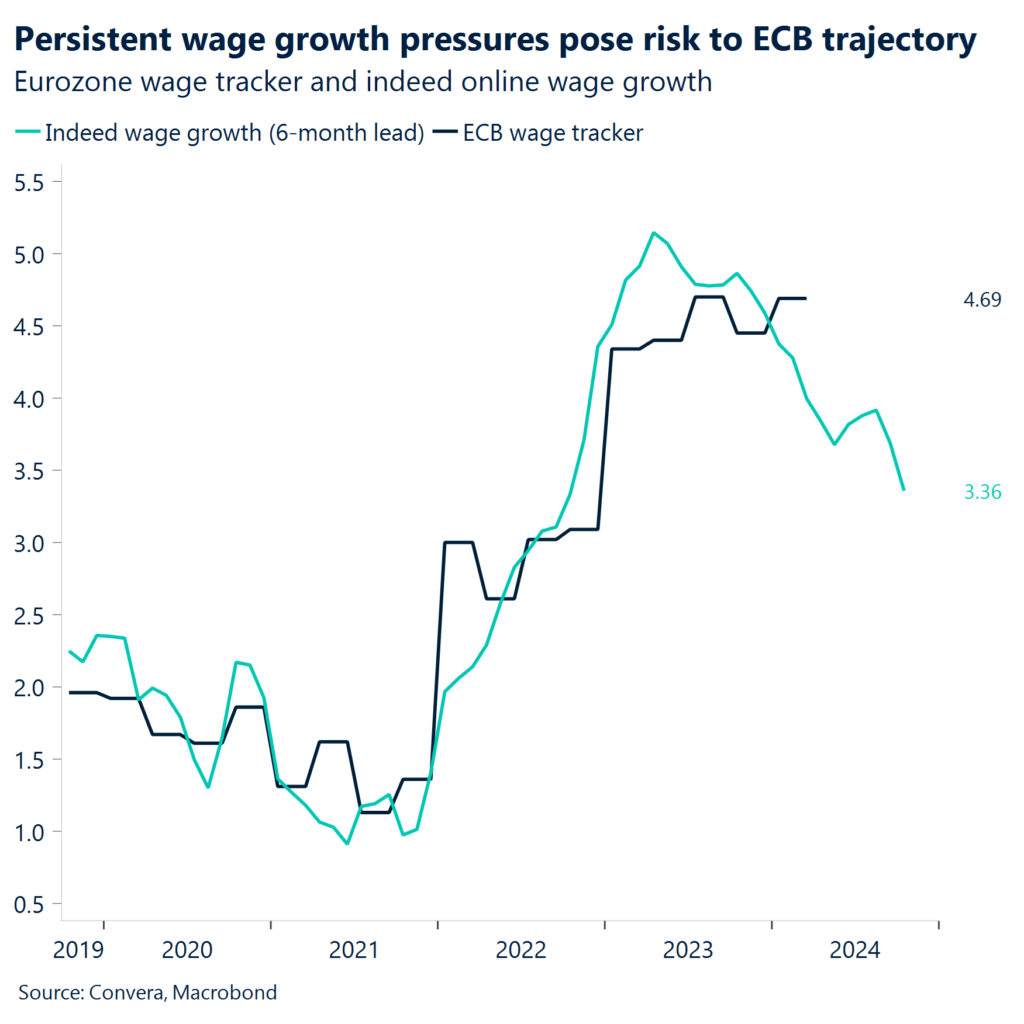

Wage growth ticks up again. Contrary to expectation, negotiated pay increased 4.7% y/y in Q1 2024, up from 4.5% observed same time last year, matching a record set in Q3 2023. Warning signs were ringing earlier this week as Germany reported a 6.2% increase in wages between January and March, boosted by tax-free one-off payments to compensate workers for soaring living costs. Negotiated wage growth is expected to remain elevated in 2024, which is in line with the persistence that has been factored into ECB staff forecasts and reflects the multi-year adjustment process for wages. However, wage pressures look set to decelerate in 2024.

ECB to push ahead with June cut. The ECB’s Villeroy reassured the markets that the ECB remains confident that inflation is easing enough for a June interest rate cut and urged not to over-interpret data on wages. The ECB wage-tracker data for the first few months of the year, when most agreements take place, indicate that negotiated wage pressures are moderating. However, the upside surprise sent a note of caution to expectations that price increases are definitively retreating. Markets scaled back on year-end ECB rate cut expectations to 60 basis points, down from 67 basis points at the start of the week.

Week ahead

US PCE key for Fed’s next move

We might see a quiet start to the week with the US Memorial Day and UK bank holiday on Monday, but the economic data picks up later. German retail sales and IFO business survey will provide insights into the Eurozone’s largest economy. In the US, Q1 GDP along with personal income and spending data will be watched closely by markets. The PCE inflation reading is the Federal Reserve’s preferred measure of inflation. Finally, a host of European data including economic sentiment, unemployment, inflation, and GDP revisions are on the calendar.

German retail rebound? Germany’s retail sales for April are expected to show a rebound after softness in March. This will be an important data point as consumer spending has been a key driver of growth amid the broader economic slowdown in Europe.

US GDP revision. The US Q1 GDP is due out on Thursday. Consensus expects 1.2% vs previous reading of 1.6%. Markets will watch for any revisions that could shift the growth trajectory. The US personal consumption and expenditure reading, due Friday, will be crucial for the Fed’s view of inflation.

European inflation update. Preliminary May inflation figures from the Eurozone are scheduled for Friday. Price pressures have been easing but remain elevated, keeping pressure on the ECB to maintain tight monetary policy. The core reading will be closely watched.

Asian inflation. Key inflation data from Australia and Japan will provide insights into ongoing price pressures in the Asia-Pacific region. Other releases on retail sales, industrial production and GDP will also offer clues on economic momentum.

Note: All times BST.

FX Views

Risk rally fizzles out

USD Dollar gains as rate cut bets trimmed. US dollar strength has significantly cooled this month, with the world’s reserve currency appreciating against just 25% of its global peers. However, it made a comeback against most of its major counterparts of late, with the US dollar index clocking its largest weekly rise in over a month, edging back above its 100-week moving average and briefly reclaiming the 105 handle. Hawkish Fed minutes and the consequent cooling off in global risk sentiment allowed for a moderate restrengthening of the dollar across the board, further supported by strong US economic data which pushed out the timing of the first Fed rate cut to December. The growth convergence story seems to be losing steam too, evidenced by the strong S&P PMIs for the US. Thus, the dollar retains its high growth and high yield appeal, so we cannot rule out further gradual appreciation going into the important PCE inflation data due next week.

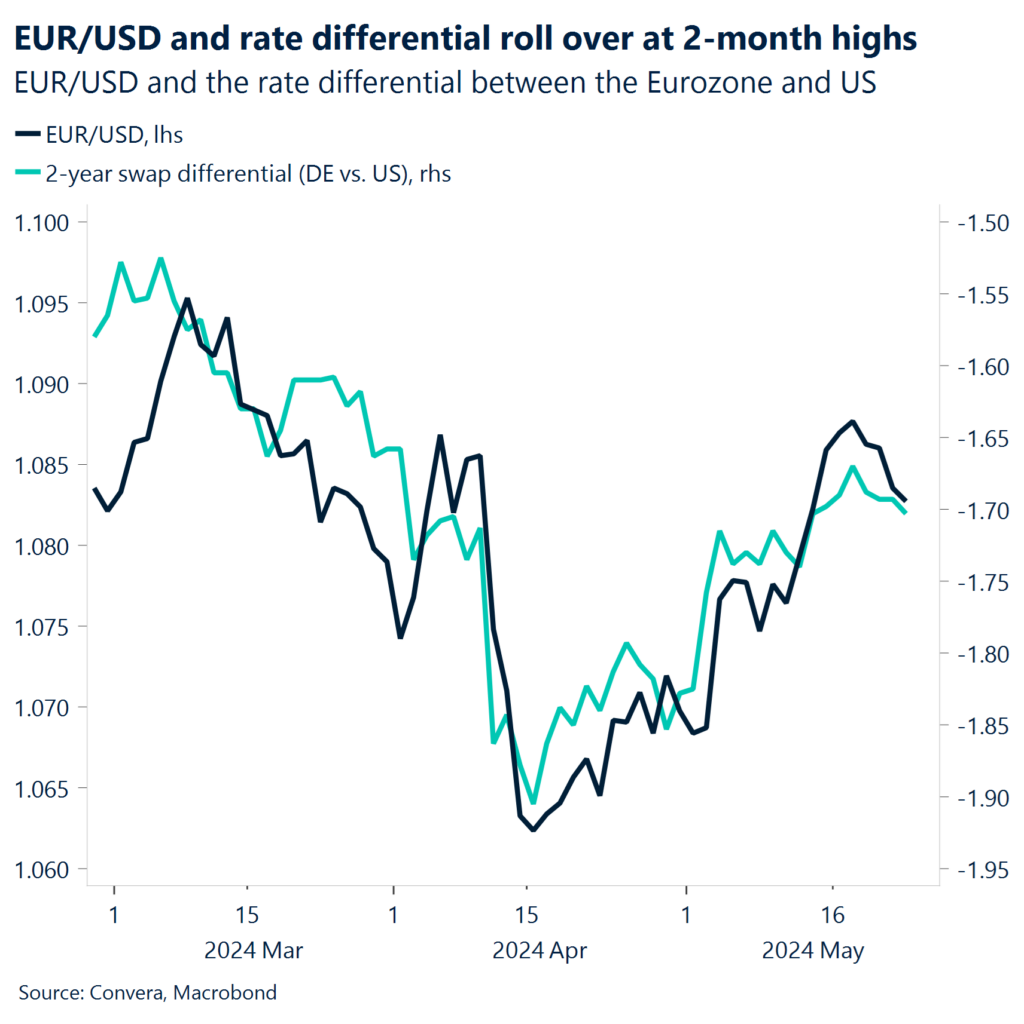

EUR Euro optimism fades. Despite ECB policymakers’ reassurances that the ECB remains confident that inflation is easing enough for a June interest rate cut, 2-week implied EUR/USD volatility spiked close to 5.2%, a 1-week high, as a reversal in wage growth disinflation cast doubt on the ECB’s rate trajectory. Investors priced out some near-term easing. The swap-implied probability of a June cut dropped to a 3-week low of around 90%, and investors trimmed their year-end expectations to 59 basis points, down from 67 basis points at the start of the week. Despite remaining resilient across most G10 peers, the euro declined in four out of the past five trading sessions against the US dollar and closed the week nearly 0.5% lower – the first weekly drop since mid-April. EUR/USD spot depreciated by over 0.6% from its May high ($1.0894) and is currently trading at a 2-week low, supported by the 100-day SMA. The 14-period EUR/USD RSI drifted below 60 and the 1-week risk reversal skew flipped in favour of euro puts for the first time in two weeks, suggesting mid-month bullish momentum has faded and near-term euro sentiment is bearish. The three-month EUR/GBP risk reversal turned the most bearish in five weeks after the UK snap general election was called.

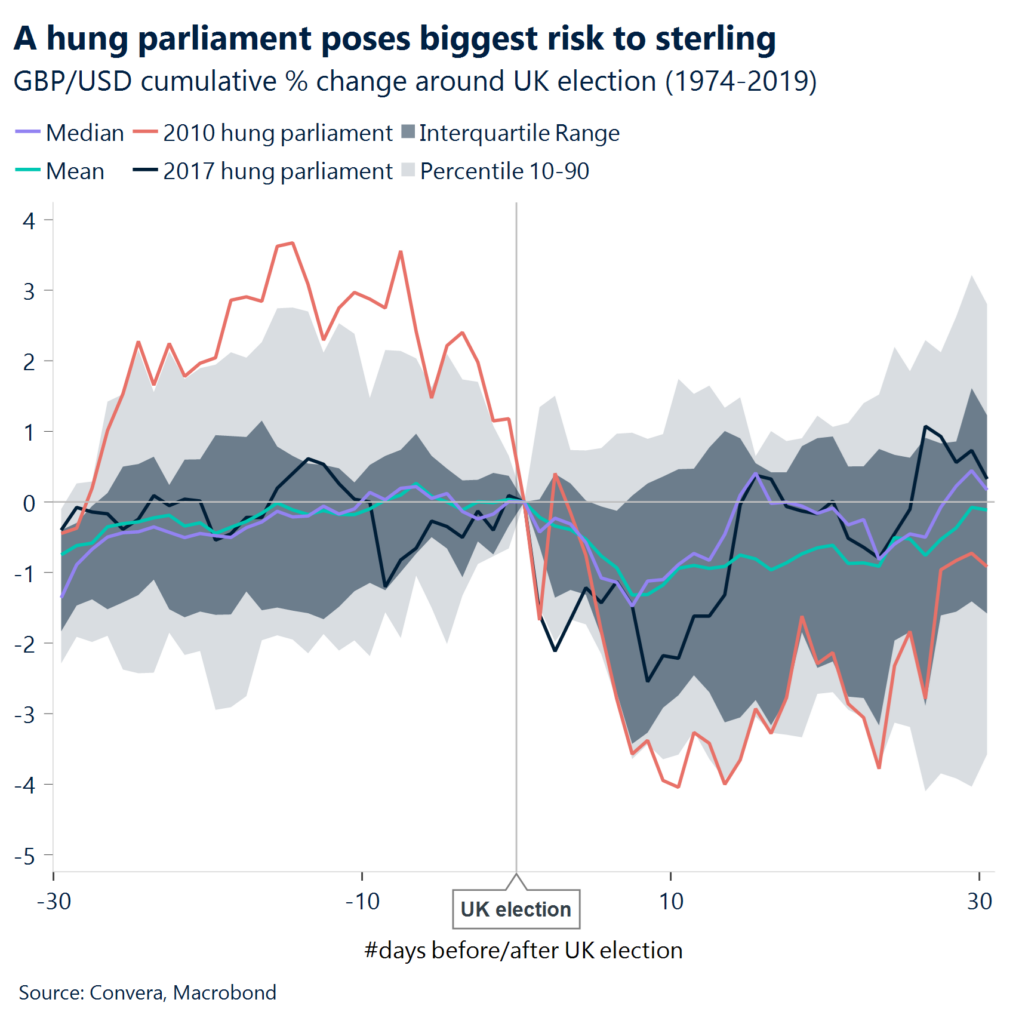

GBP Keep your eyes on the polls. The pound should have seen an eventful week after a slew of important data prints and a surprise general election being called, but sterling has largely taken it all in its stride. GBP/USD held close to 2-month highs at $1.27 and climbed to 9-months highs just 30 pips shy of €1.18 against the euro. The main driver of sterling strength was the hotter-than-expected inflation report resulting in the probability of a June rate cut by the BoE plunging from 50% to 10%. UK Gilt yields jumped to 1-month highs and the UK-US yield spread to a 2-month high, supporting the pound. Meanwhile, the election news hasn’t had a negative impact on sterling so far, but noise could pick up if polls show the incumbent Conservatives eating into Labour’s lead. Although the spot market was muted on the election news, the reaction in options market reflects the anticipation of volatility, with 2- and 3-month implied vols, which capture the election date, spiking higher. A Labour majority would likely be most beneficial for sterling. The biggest risk to the downside in the near term, which could drag GBP/USD back under $1.25, is a June rate cut by the BoE or a hung parliament result in the election, though both scenarios are tail risks at this stage.

CHF Pressured by rate cut prospects. The Swiss franc extended its decline against the euro, reaching the weakest level since April 2023, and is now down almost 4% against its European peer in less than a month. GBP/CHF hit its highest level since August 2022, up almost 10% this year, whilst USD/CHF scored its third weekly rise in a row, retesting the 0.9150 resistance area. Volatility has declined, with Swiss franc overnight volatility closing below the 4.6% threshold two days running – the first such occurrence midweek in more than three years. Weighing on the franc is the growing consensus that another quarter-point interest rate cut is coming next month with traders assigning a 76% chance of a such a move. By year-end, money markets are betting on a 215 basis-point difference in the key policy rates of the ECB and SNB, increasing the chance of EUR/CHF breaking above parity for the first time since March 2023. Swiss GDP numbers are due next week whilst the CPI data release comes on 4 June.

CNY CNY hobbled by housing havoc. The Chinese yuan has seen a resumption of its weakness as the People’s Bank of China signalled it was prepared to let the CNY fall by allowing the USD/CNY fix to climb to the highest level since January. A Reuters poll conducted between May 10-17 pointed to a deepening slump in China’s property market, with new home prices forecasted to fall 5% this year versus a 0.9% decline projected in February. Additionally, property sales are expected to plunge 10% compared to the earlier 5% forecast, while investment is seen contracting 10% versus the previous 6.1% estimate. The poll responses may only partially reflect the impact of government measures announced on 19 May to support the property market. Looking forward, the major test will be whether the Chinese government allows USD/CNY to climb above the key 7.25 level, with the offshore USD/CNH seeing resistance at 7.28. Key data releases to monitor include the composite PMI, manufacturing PMI, and non-manufacturing PMI, which will shed light on the broader economic conditions.

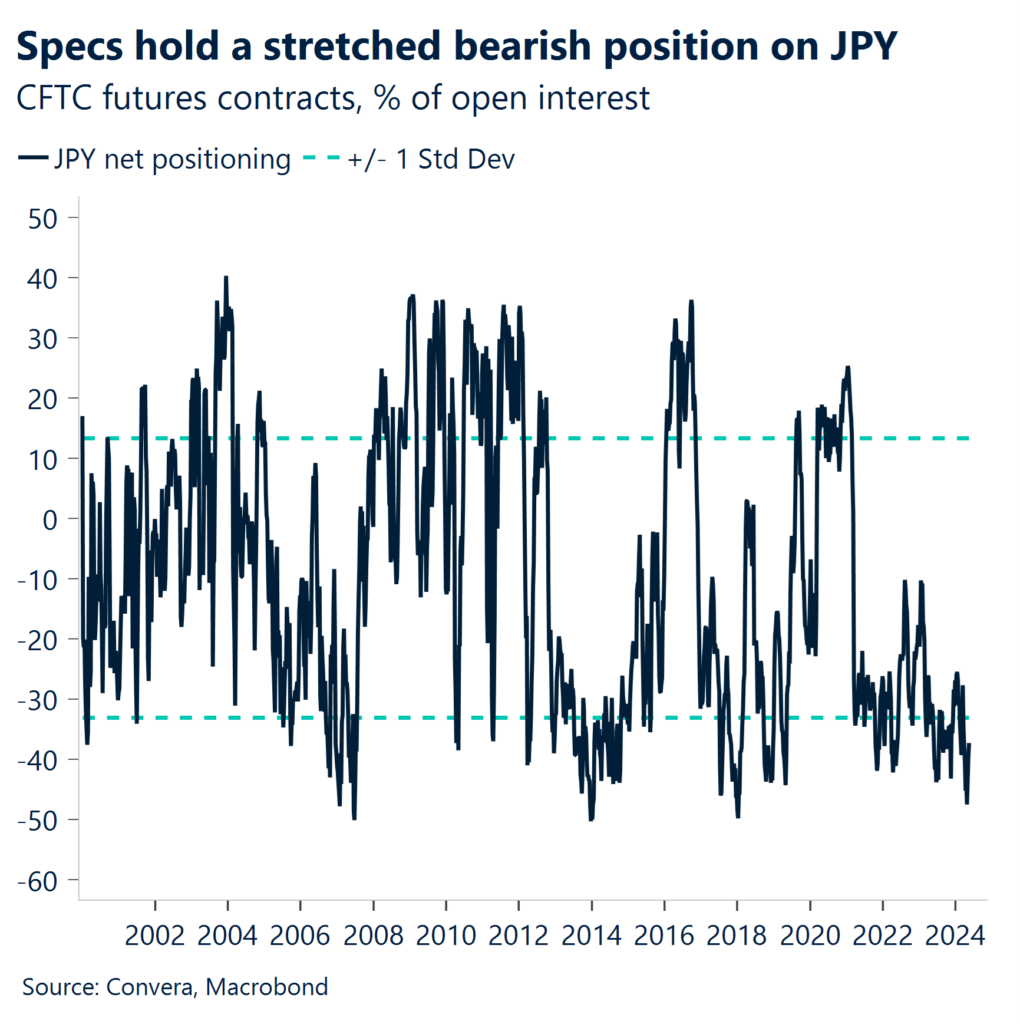

JPY Yen still weaker, despite factory revival. Japan’s manufacturing sector showed signs of revival, with the au Jibun Bank flash manufacturing PMI expanding for the first time in a year to 50.5 in May from 49.6 in April, crossing above the 50 threshold that separates growth from contraction. The composite PMI climbed to its highest level since August 2022 at 52.4, even as the flash services PMI dipped to 53.6 from 54.3. The near-stabilization of manufacturing output stokes hopes that Japan’s private-sector growth may finally broaden. While both average input costs and output prices rose at a slower pace, inflation remained well above long-run averages. Despite the better economic news, the Japanese yen remained mostly weaker. USD/JPY continues to trade above key chart support at 151.945-153.069, keeping the broader rally structure intact for now, though resistance near 160 shows clear distribution patterns. Also, Japanese authorities have clearly signaled the 160-level is the latest “line in the sand” for intervention. Any turn lower in USD/JPY might be significant – speculative positioning is extremely stretched and could lead to JPY appreciation if there is any panicked reversal. Upcoming Tokyo core CPI and industrial production data will provide further insights.

CAD Broad-based selloff amid soft inflation. CAD fell against its G10 peers after domestic inflation came in lower than expected. With all inflation measures within the Bank of Canada’s tolerance band, the pressure mounts to kickstart its monetary policy easing cycle from the current 24-year highs. The swap implied probability of the BoC rate cut in June rose to 65%, up from 43% at the start of the week. Despite markets jumping the gun with additional pricing for near-term easing, the risks are skewed for a delay in the BoC easing cycle. The central bank may wish to opt to wait until its July meeting to confirm that lower core inflation will be sustained as it will have two more CPI releases to consider. If the Bank does delay, the market will unwind recent CAD weakness. Meanwhile, the diverging rate views between the BoC and the Fed led to wider CA-US 10-year yield interest rate differential, which weighed on the Canadian dollar. USD/CAD rose almost 1% over the week, its best performance in the past six weeks. From a positioning perspective, the latest CFTC data shows that hedge funds upped short bets on the Loonie to their highest since 2017. Market sentiment turned more CAD bearish as 1-month 25-delta risk reversals, which capture both the BoC and the Fed June rate decisions, ticked to a 2-week high.

AUD Aussie caught in crosswinds. The Aussie has given up its recent strength and reversed lower. Australian economic data presented a mixed picture, with the composite PMI slipping to a three-month low of 52.6 in May, though still in expansion territory above 50. This followed evidence of an economic slowdown amid elevated interest rates. While consumer spending remained soft, acting as a drag on growth, the input price index rose at the fastest pace in six months, indicating persistent domestic inflation pressures in Q2. Notably, the employment index touched its highest level in over six months, suggesting robust private-sector labor demand. After reaching a four-month high, AUD/USD has now slipped into a short-term downtrend, with the pair now below the 21-day moving average. Next resistance levels are at 0.6747 and the broader 0.6819-0.6901 range highs. Looking forward, monthly CPI, retail sales and private new capital expenditure data will provide clarity on the economic outlook.