Volatility strikes again

It’s been another dramatic stretch of volatility across asset classes, with the US dollar rebounding, metals and crypto crashing before staging sharp reversals, and equities sliding. US stocks remain among the worst performers this week and are now at the bottom of the global leaderboard year‑to‑date: the S&P 500 fell 1.2% on Thursday, while the Nasdaq dropped 1.6%.

Tech remains the pressure point. Amazon shares tumbled 11% in extended trading after the company outlined plans to spend $200 billion on artificial intelligence this year — a colossal outlay that has fuelled concern the long‑term payoff may fall short of expectations. The sector’s sensitivity to AI‑related capex is increasingly dictating broader risk sentiment.

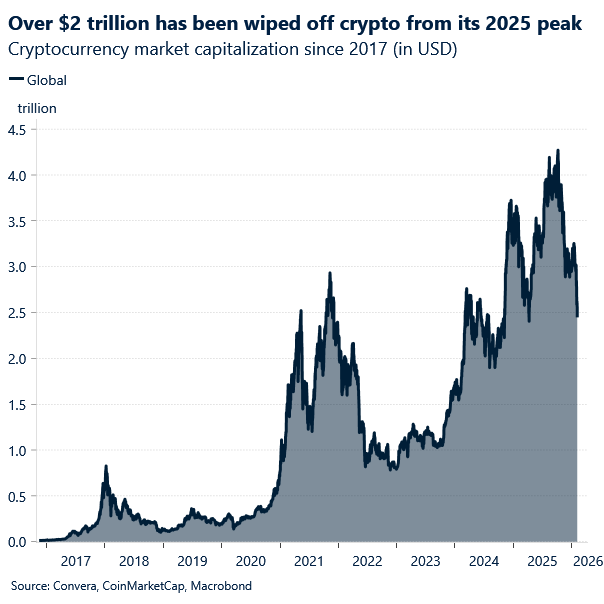

Volatility has been just as intense in metals and crypto. Silver has rebounded about 3% this morning after Thursday’s extraordinary 20% plunge, gold gained 1.6%, and Bitcoin bounced more than 3% after briefly sliding toward $60,000 — less than half its October peak.

There was no clear catalyst for Friday’s stabilisation beyond the sheer speed and depth of this week’s selloff. Most assets caught support at roughly the same time, pointing to positioning and exhaustion rather than a shift in fundamentals. That synchronised rebound is welcome, but it also highlights a risk: if one leg of the market starts to wobble again, the rest may follow. This week has underscored how tightly correlated risk assets have become — and how fragile sentiment remains heading into the weekend.

USD: What it means for the dollar

A tougher equity backdrop would normally support the USD as investors rotate out of risk and out of pro‑cyclical currencies. That dynamic is likely behind the dollar’s modest resilience this week. But the scope for further gains looks limited. A US‑led equity correction would ultimately hit US activity hardest, force the Fed into more aggressive easing, and weaken the dollar rather than strengthen it.

At the same time, the broader diversification theme — or at least the rise in dollar‑hedging demand — still hangs over the currency. That structural flow is unlikely to disappear quickly and may cap any sustained upside. The result is a dollar supported in the near term by risk aversion, but facing medium‑term headwinds if the equity correction deepens and the Fed is pushed toward a more forceful policy response.

Meanwhile, on the macro front, the latest US labour data added to the cautious tone. The Challenger report showed companies announced 108.4k job cuts in January, the highest for that month since 2009. Initial jobless claims also rose to 231k, a two‑month high and well above expectations of 212k. The softness extended to the ADP report, where private‑sector job growth fell well short of forecasts.

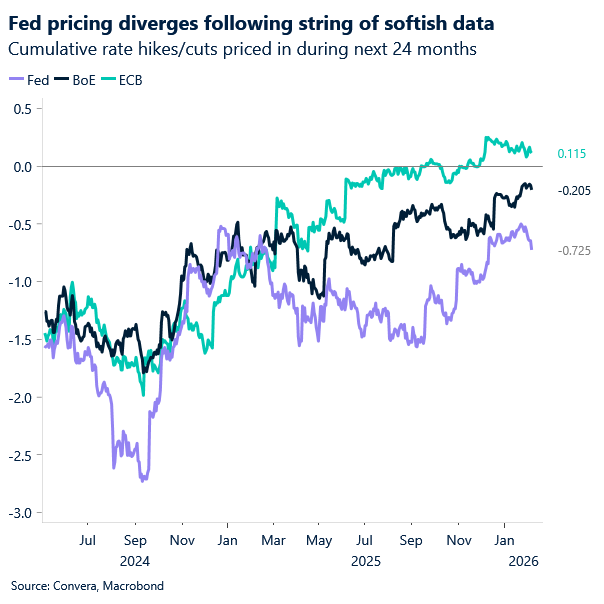

Taken together, the run of weaker labour indicators reinforced expectations of Fed easing this year. Markets continue to price a first rate cut in June, with a second potentially following in September.

GBP: BoE tone undercuts sterling

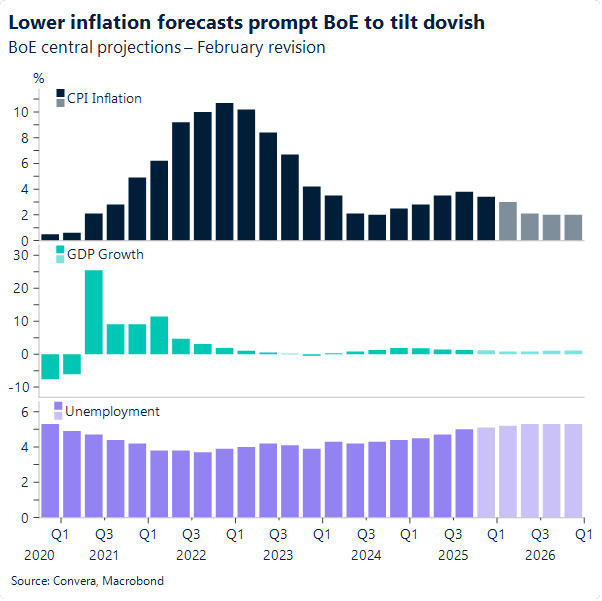

While a steady Bank of England (BoE) was widely expected (rates unchanged at 3.75%), what we hadn’t anticipated was a stronger dovish tilt, clearly illustrated by the 5–4 vote split, with four dissenters favouring a cut. The shift in tone carried through to the press conference as well. Supported by updated forecasts pointing to inflation falling below target by spring, Governor Bailey sounded more confident in the UK’s disinflationary outlook, noting that “there should be scope for some further reduction in Bank Rate this year.” The dovish stance is reinforced by the broader backdrop of slowing growth and rising unemployment. According to the projections, inflation does not rise above 2% again from April until the start of 2029 and spends four consecutive quarters below target.

The tone marked a clear contrast with the more hesitant, hawkish‑leaning stance of previous meetings. Traders responded by sharply increasing the probability of a March cut from around 20% to roughly 65% – a sizeable shift. That said, with inflation still at 3.4%, the dovish tone remains highly sensitive to incoming data that confirm the softening in price pressures.

Sterling shed ground across the board, with losses compounded earlier in the day by renewed political tensions surrounding Starmer’s leadership. The rates market was instructive, however, in showing how the rate‑outlook narrative dominated sterling’s price action. Long‑end yields had pushed higher before the meeting, triggering a bear‑steepening setup, and the BoE’s dovish hold extended that steepening across maturities.

The shift clearly jeopardises short‑term bullish momentum in sterling, particularly against the euro, where the UK rate outlook is most cleanly expressed given the neutrality of the euro leg. The key data release now is the January inflation report, due 18 February, which will be crucial in gauging whether inflation developments align with the BoE’s projected disinflationary path, shaping sterling’s near‑term direction in turn.

EUR: ECB keeps rates on hold

The European Central Bank (ECB) kept rates unchanged at its first meeting of 2026, as expected, and reiterated that inflation should converge toward its 2% target over the medium term. The Governing Council again described policy as being in a “good place,” noting a resilient euro‑area economy but acknowledging that the outlook remains clouded by global trade uncertainty and geopolitical tensions.

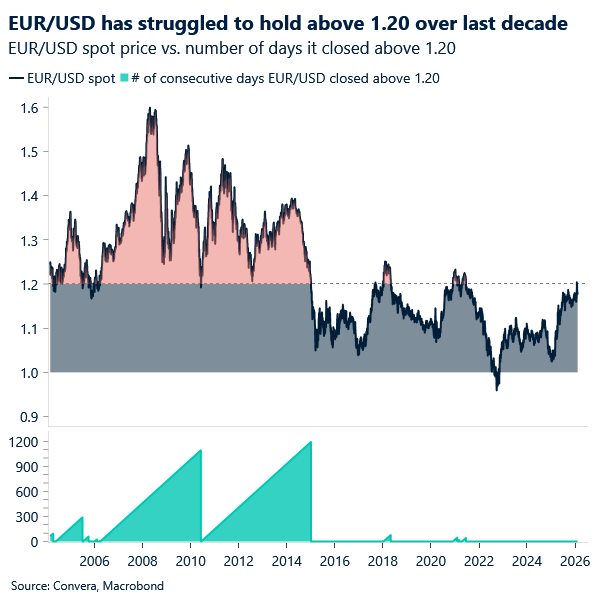

The stronger euro was a key talking point. The ECB’s nominal trade‑weighted euro is sitting at multi‑decade highs and appreciating at a 7–8% y/y pace, but President Lagarde pushed back against the idea that policymakers are alarmed. She stressed that the currency is broadly in line with historical averages and that recent moves were already embedded in the ECB’s baseline — including an assumed EUR/USD rate of $1.16 for this year. With EUR/USD having backed a few handles away from the feared $1.20 mark last week and now trading around $1.18, the urgency for the ECB to lean against euro strength — or reopen a policy debate via rate cuts — has faded.

Outside the ECB, market dynamics matter. Volatile swings in precious metals are spilling into EUR/USD, with sharp silver sell‑offs giving the dollar a lift. The 20‑day correlation between EUR/USD and both gold and silver now sits in the 75th percentile of the past five years — a reminder that metals sentiment is exerting an unusually strong pull on the pair at present.

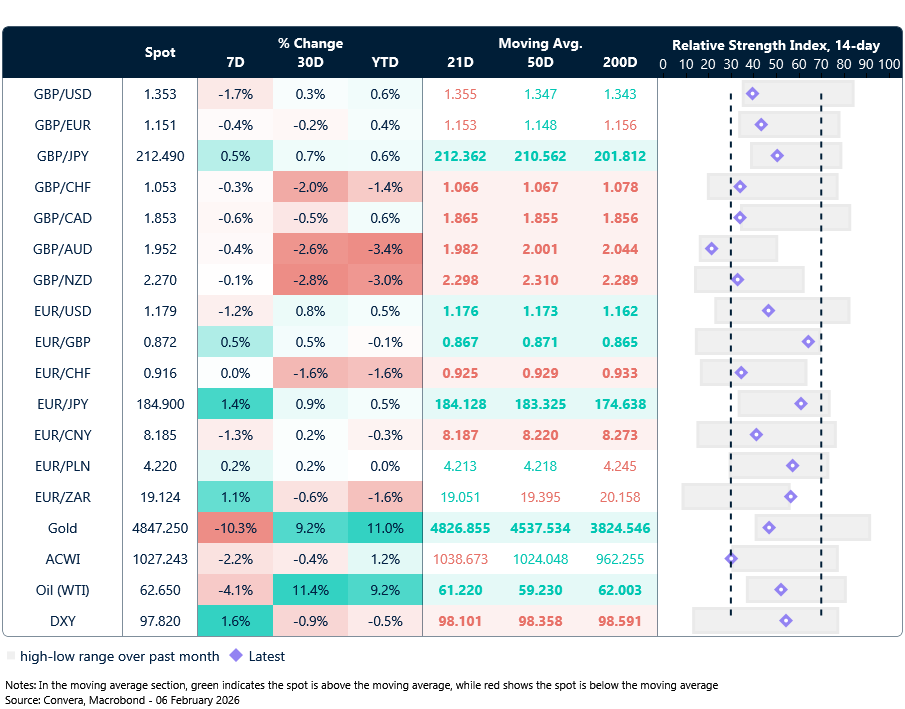

Market snapshot

Table: Currency trends, trading ranges & technical indicators

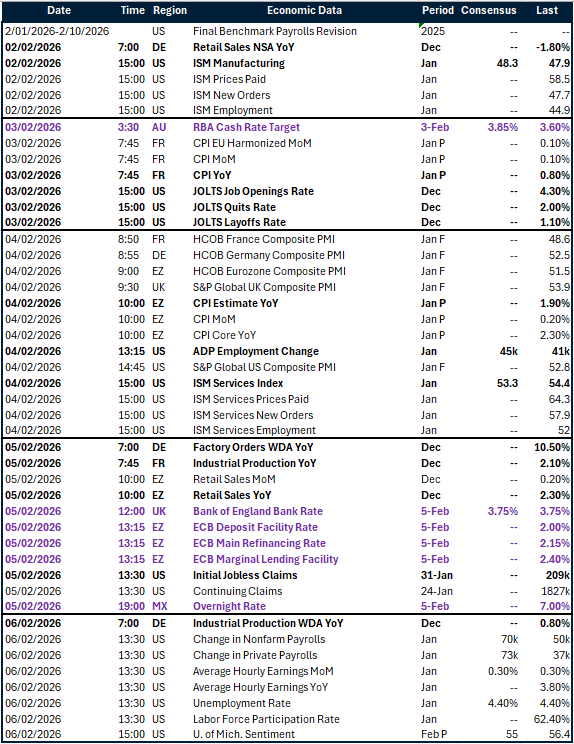

Key global risk events

Calendar: February 2-6

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.