Sterling sentiment snaps as bond turmoil bites

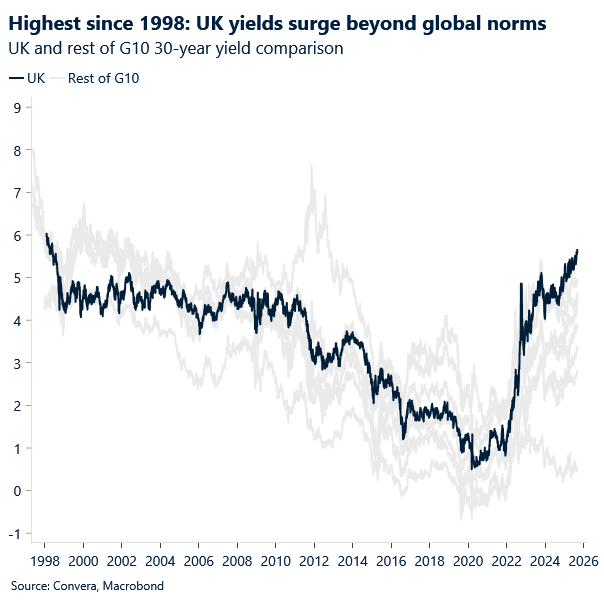

Bond market stress is once again haunting the pound despite the lack of dysfunctional moves. indeed, the issue is global in nature too. Long-end yields are rising across major economies, curves are steepening, and investor anxiety over sovereign debt and inflation is intensifying. But while UK 30-year gilt yields didn’t move dramatically yesterday, they’ve quietly reached levels last seen in 1998 – a milestone that’s hard to ignore.

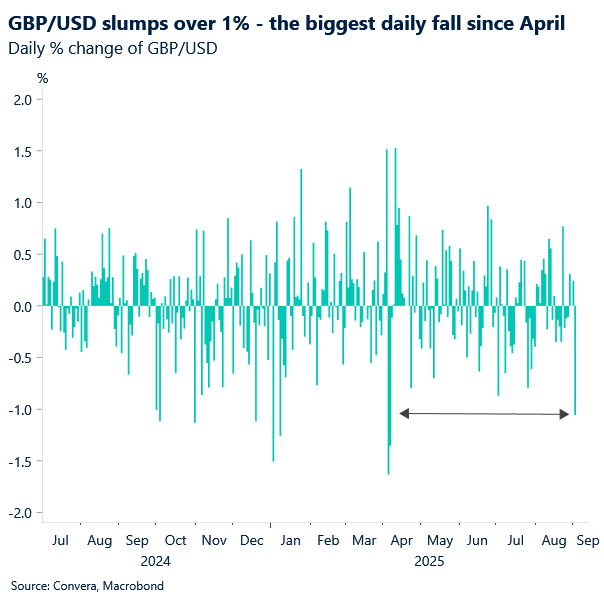

Sterling’s sensitivity to rising yields is striking as it is underperforms across the G10, with GBP/USD suffering its steepest one-day drop since April, when Liberation Day headlines triggered a broad risk-off move. The pair has broken below $1.34, with limited support until $1.32, while GBP/EUR has slipped back under €1.15, leaving it nearly 5% lower year-to-date.

Markets don’t always react to new information – they move when old risks become impossible to ignore. We’ve long warned that the UK’s stagflation backdrop and the Bank of England’s (BoE) hawkish stance meant sterling’s gains were resting on shaky foundations. Now, fiscal concerns are taking centre stage.

The government’s estimated £51 billion fiscal gap is fuelling investor unease. Chancellor Rachel Reeves faces a tough balancing act: finding savings amid internal party tensions and likely needing to raise taxes again in the autumn budget. These concerns are driving long-end yields higher and amplifying sterling’s fragility.

There may be some relief later this month. The BoE’s September 18 policy meeting is expected to include a review of its bond-selling pace. Governor Andrew Bailey has previously flagged concerns about illiquidity and curve steepening, suggesting the central bank may slow its quantitative tightening – particularly at the long end.

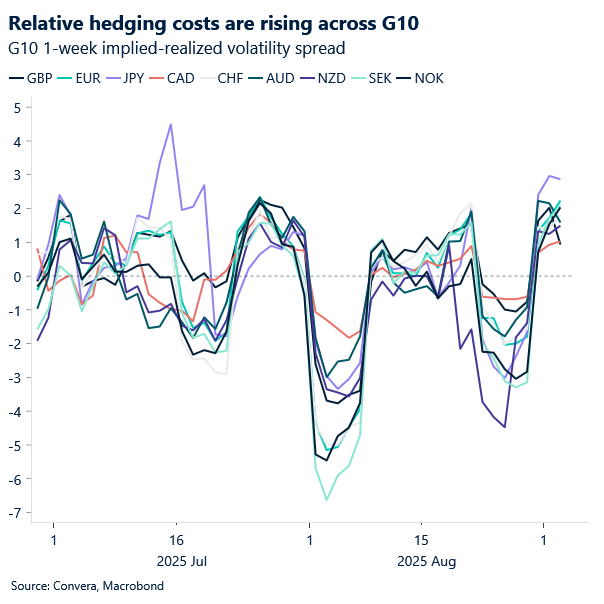

Still, the UK remains at the epicentre of global bond stress and in the FX options market, the volatility skew is flattening, signalling traders are pricing in further near-term downside. Elevated realised volatility is keeping hedging costs high, reinforcing the cautious tone around GBP.

Summer’s lull looks over

Volatility is back, and this time it’s not driven by fresh headlines but by a long-simmering repricing of risk. Global long-end yields are grinding higher, yield curves are steepening, and investors are finally confronting the structural threats – fiscal fragility, inflation persistence, and policy uncertainty – that have been building for months.

The shift in tone is partly seasonal. With summer behind us and institutional desks fully staffed, liquidity has returned – and so has price sensitivity. What was tolerated in August is now triggering defensive repositioning across asset classes. FX options markets are flashing caution, with demand rising for downside protection and hedging costs staying elevated.

The dollar’s recent bounce looks more like a reflection of fragility elsewhere than a confident bid for safety though. The Japanese yen, for instance, remains weighed down by domestic political noise, and gold has lost momentum despite its record highs. We doubt the dollar’s rebound has legs in it unless backed by a more supportive US economic backdrop.

On the data front, the ISM manufacturing survey offered a mixed picture: new orders showed signs of life, but employment remains worryingly soft. If these trends persist, the Fed may have room to ease, but global crosscurrents could blunt the impact.

Today’s US JOLTS report will be closely watched. Job openings are expected to have dipped slightly in July to around 7.37 million. But even at these levels, demand for labor remains well above the pre-pandemic average of 7 million seen in 2018–19 – raising fresh concerns about labor market tightness and its implications for wage inflation and Fed policy.

All eyes are also on Friday’s payrolls report. A weak print would reinforce rate cut expectations, while a hold risks reigniting political pressure on the Fed, adding another layer of uncertainty to an already fragile macro backdrop.

Amid tepid sentiment and a global bond sell-off

The euro falls within the group of currencies grappling with mounting fiscal concerns and rising long-term yields – a theme that featured prominently in yesterday’s global bond sell-off. Following France’s recent political shake-up, with a confidence vote just days away, the country’s 10-year bond yields now hover roughly 80 basis points above Germany’s, underscoring the widening spread.

While last week’s headlines didn’t immediately pressure the euro, yesterday marked a wake-up call for global investors, highlighting how widespread these rising fiscal pressures have become – with FX markets reacting sharply (see GBP). Although the initial shock was broad-based, we expect the longer-term implications of rising yield risk premia to become more country-specific, shaped by idiosyncratic factors.

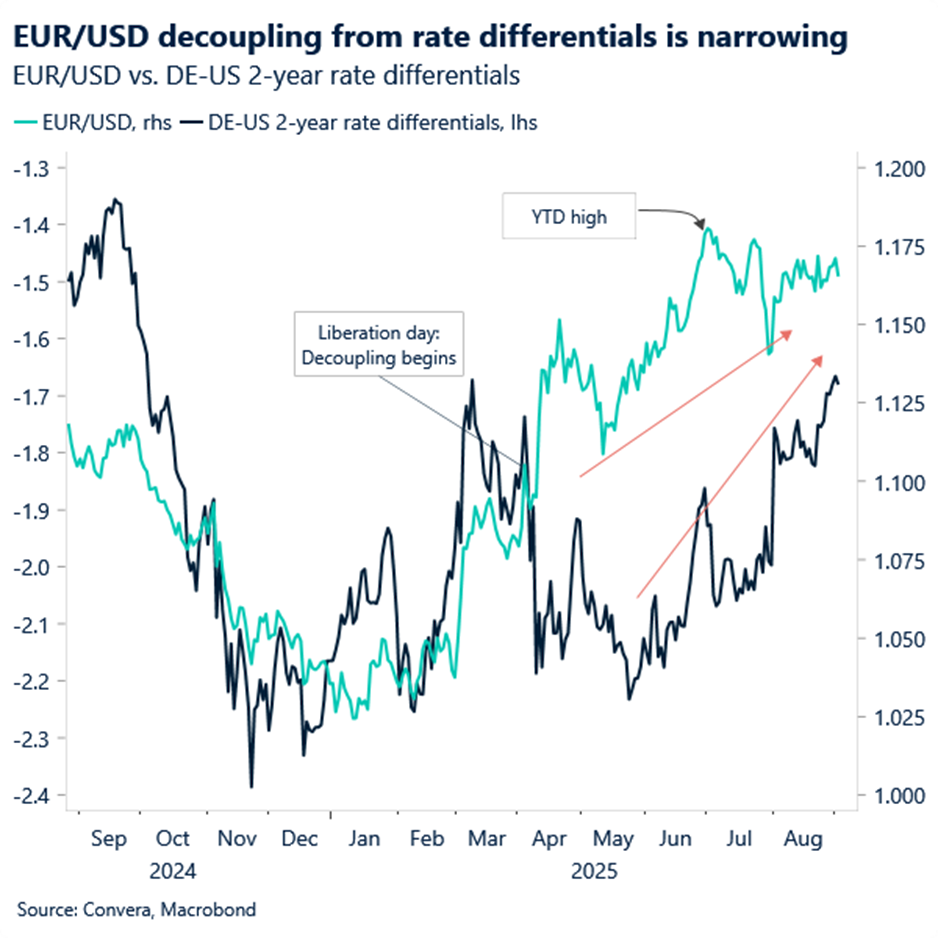

EUR/USD quickly approached the lower end of the 1.16–1.17 range it frequented throughout August, before paring losses on the back of mixed US ISM PMI data.

Our base case remains that improved US labor market data this week will push EUR/USD below the 1.16 support level in the short term, as US-driven fundamentals increasingly dominate FX price action. Meanwhile, negative USD sentiment has grown increasingly high-maintenance – only more substantial dollar-negative risk events will keep it satisfied. The narrowing gap between EUR/USD spot and rate differentials reinforces this view: unlike in April–May, when EUR/USD looked overstretched, and yet still comfortable at those +1.17 levels, on weak dollar sentiment, that divergence appears to be slowly narrowing. Looking ahead, rate differentials will need to carry more weight to propel EUR/USD back toward those YTD highs seen in July.

Pound dumped across the board

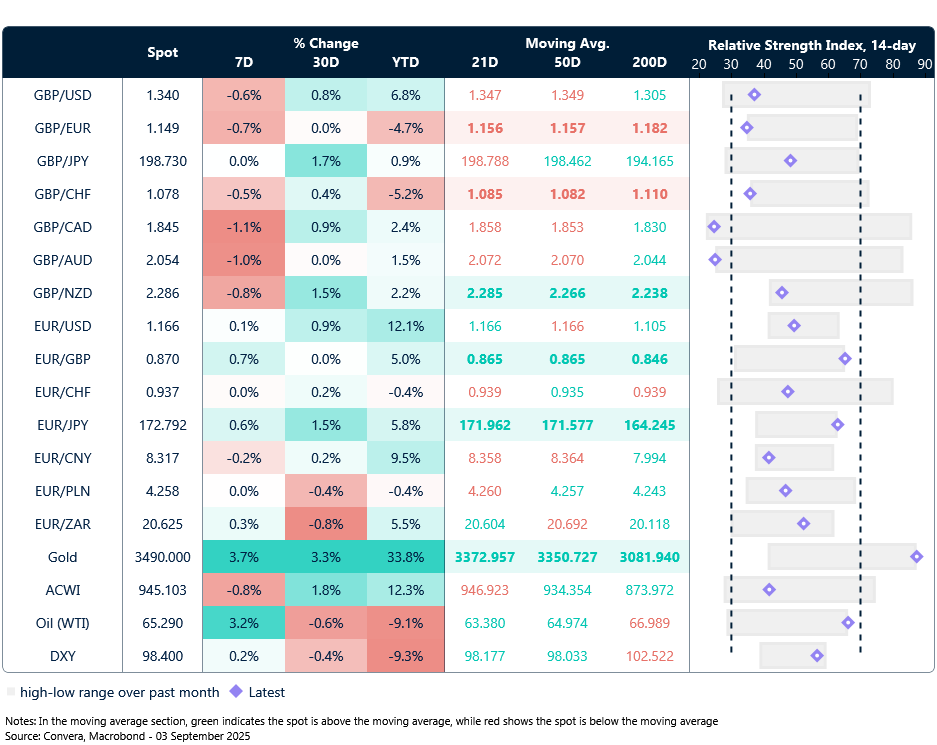

Table: Currency trends, trading ranges and technical indicators

Key global risk events

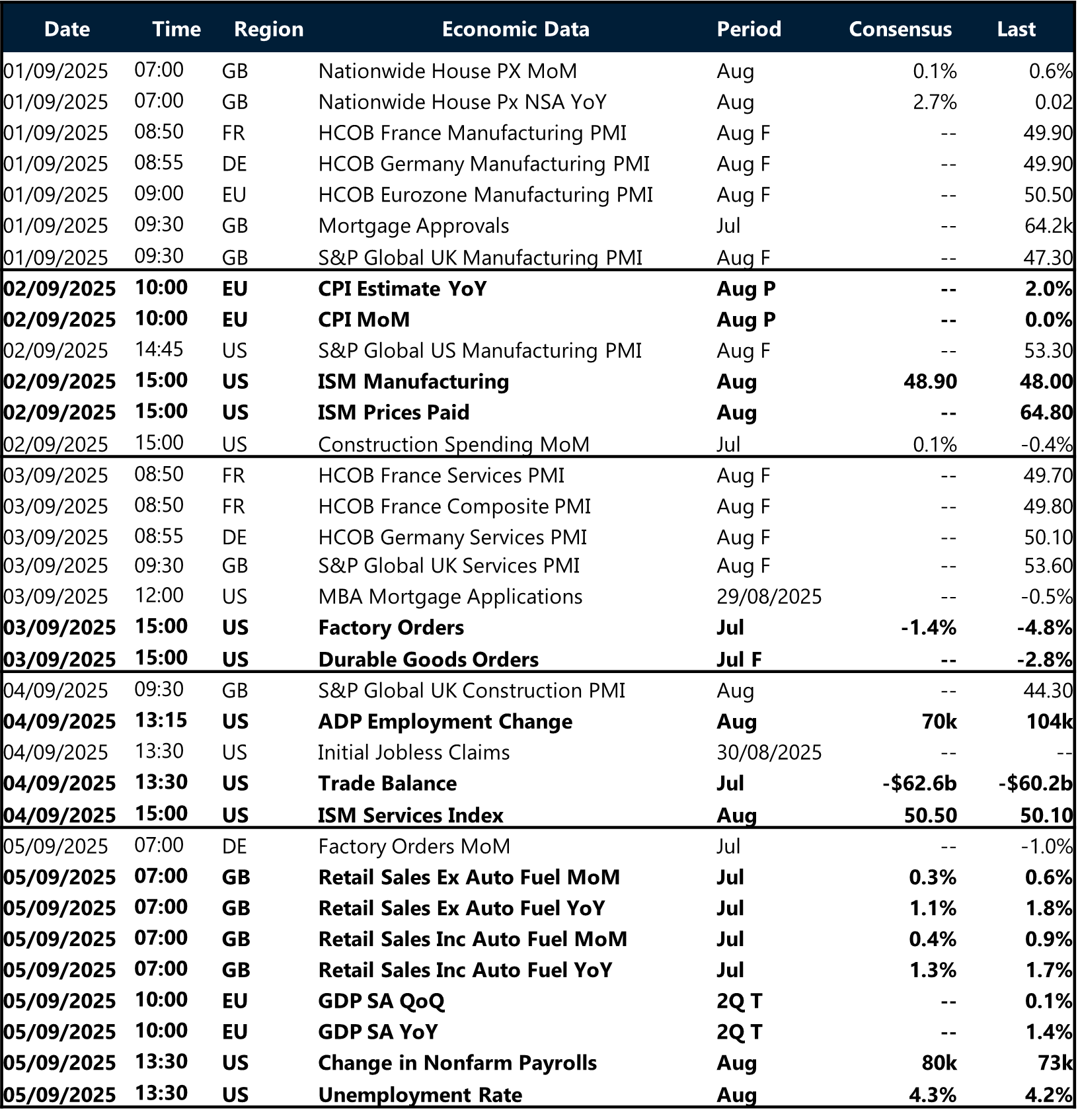

Calendar: September 1-5

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.