USD: When higher yields start to bite

The macro backdrop is starting to shift in a way markets can’t ignore. The Trump–Xi meeting delivered little beyond optics, especially on Iran, leaving geopolitical risks simmering while oil pushes higher and keeps inflation pressure alive. At the same time, 10-year yields across the US, UK and Japan have broken higher in unison, unwinding ranges that held for months or even years. Equities have brushed it off so far, supported by a strong earnings season, but that cushion is fading. As earnings roll behind us, the focus is drifting back to macro, where inflation expectations are creeping higher and financial conditions are tightening through rates rather than policy.

History shows that markets can tolerate rising yields for longer than expected, until they can’t. In 1987, equities surged through the first half of the year even as bond yields and rate expectations moved higher, before confidence cracked abruptly into October. The late 1990s followed a slower burn: the Fed took policy rates up to restrictive levels into 2000, while long yields held high, yet equities kept rallying on productivity gains and strong earnings narratives, until the peak finally gave way. The common thread is not simply higher yields, but the moment when higher yields start to undermine the equity story investors are relying on.

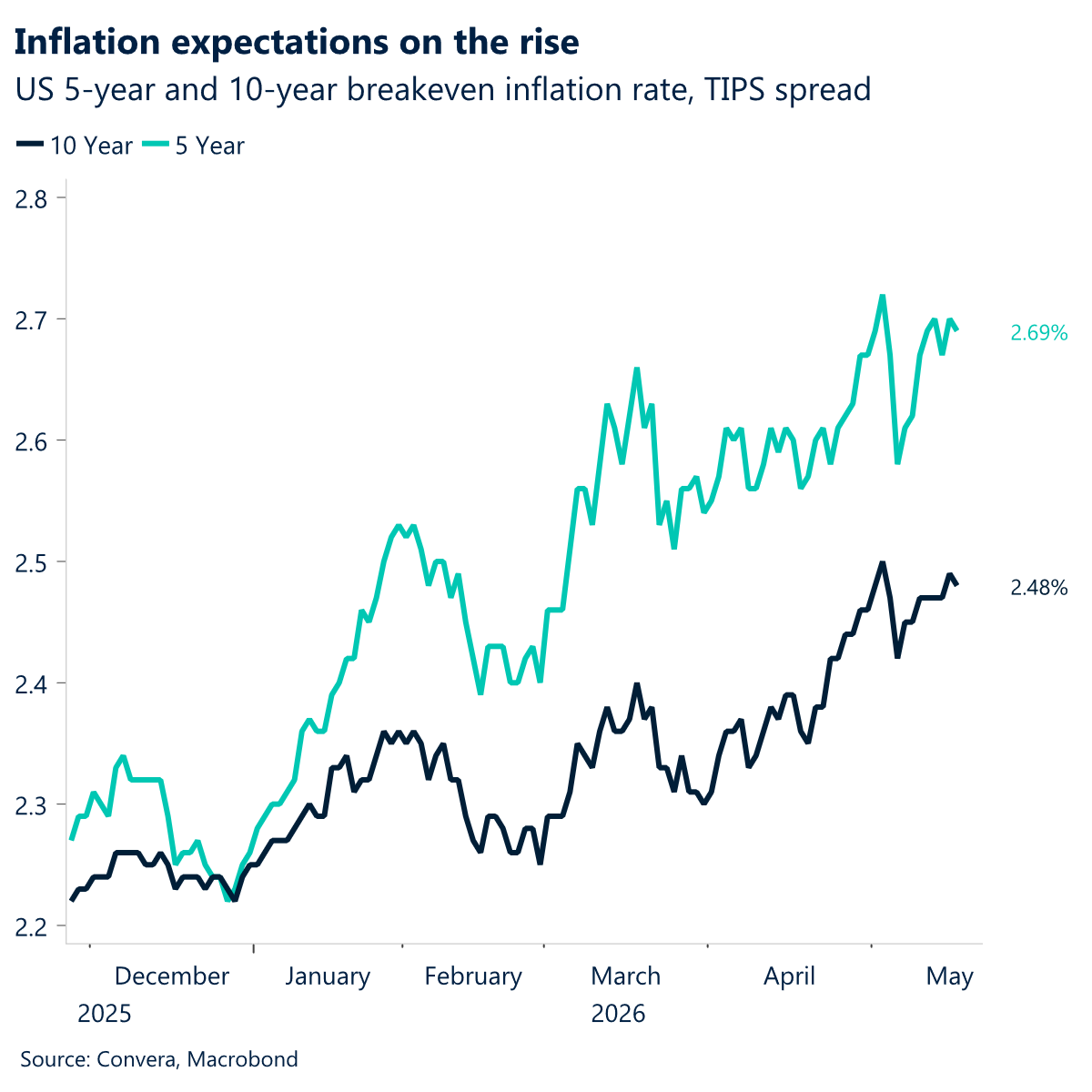

That brings the focus to financial conditions. Policy does not need to hit an exact level to become restrictive; it becomes restrictive when the combination of rates, spreads, and liquidity begins to slow activity enough to pressure earnings and demand. Economists often frame this through the idea of a neutral rate, where policy above that level restrains growth, even if the exact number is hard to pin down in real time. In practical terms, the tipping point tends to come when higher real yields compress valuations, while the consumer, especially lower-income cohorts, starts to feel the squeeze from energy and inflation. That dynamic looks increasingly relevant now, with inflation expectations drifting higher at the same time as yields rise.

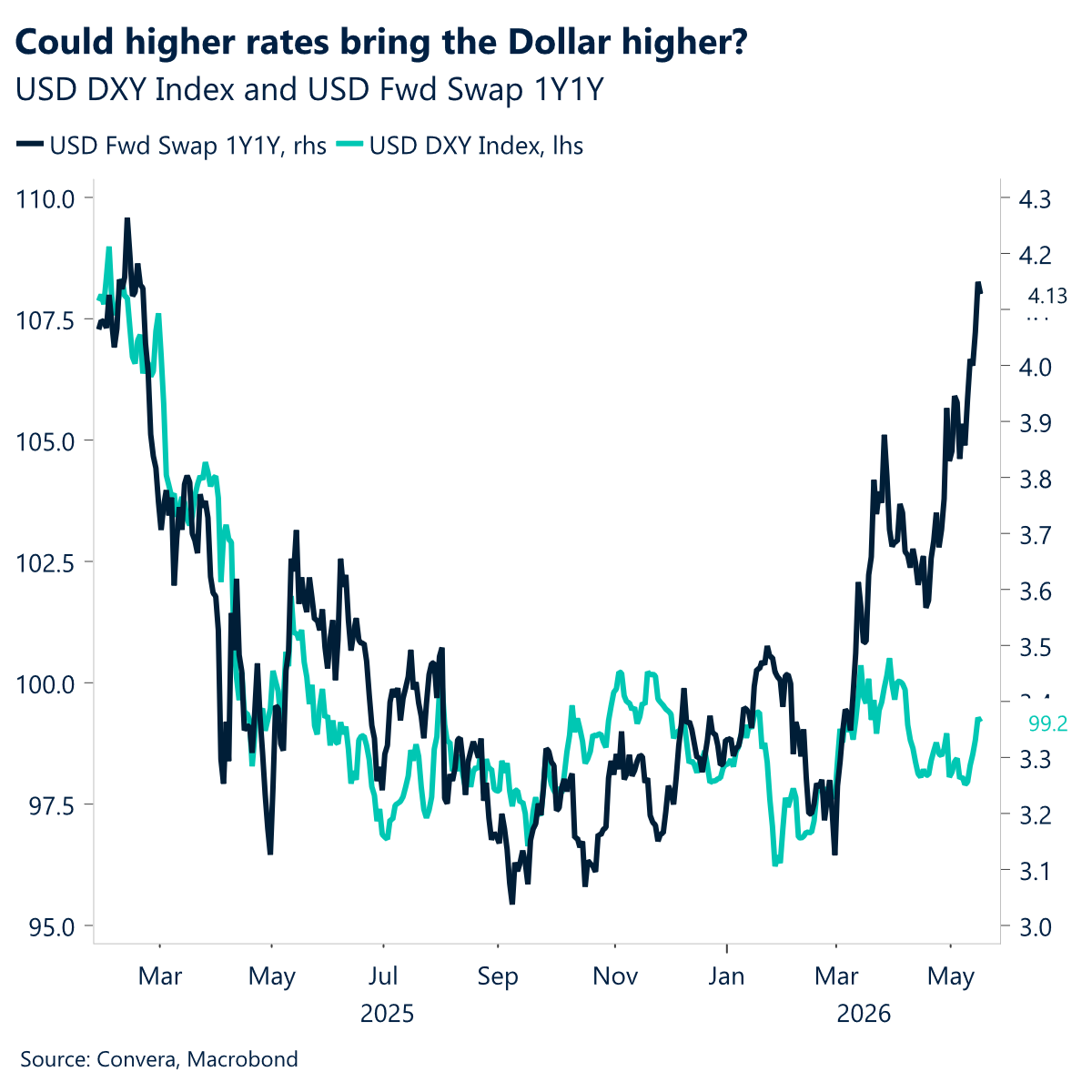

For the USD, the signal is not straightforward yet. Strong risk appetite and solid earnings have prevented the dollar from fully reflecting higher US yields, while rising rates abroad have diluted the usual relative advantage. But if financial conditions tighten further and equities begin to roll as the earnings impulse fades, the dollar’s defensive characteristics should reassert themselves. The path higher may not be linear, especially with global yield moves sharing the load, but in a scenario where macro takes over from earnings, the bias for the USD still points higher.

The rates market is reinforcing that view. Forward pricing for US policy has shifted higher, particularly in the one-year, one-year horizon, pointing to a more persistent inflation regime than markets had been assuming since the start of the war. That matters beyond valuations. When inflation is being driven by commodities and supply-side shocks, the adjustment process tends to be uneven and disruptive, with capital gravitating back toward the dollar as volatility rises. In that sense, the recent disconnect between higher US yields and a still-rangebound USD looks increasingly fragile. If the combination of elevated forward rates, tighter financial conditions, and commodity-driven price pressures starts to bite simultaneously, the transition from an earnings-led market to a macro-dominated one is unlikely to be smooth.

EUR: Hopes rise, then fade

Yesterday’s rebound in EUR/USD may have been more of a technical washout following four consecutive days of heavy selling, rather than driven by any meaningful shift in sentiment. Short-lived hopes of an imminent deal between the US and Iran may have triggered the move. Ultimately, however, fresh proposals from both sides were deemed insufficient to seal an agreement.

Developments around the Strait of Hormuz remain the euro’s dominant driver, given the eurozone’s dependence on imported energy. Conflict-related headlines are therefore likely to continue driving short-term price action in the currency, particularly in the aftermath of the Beijing Summit, as markets assess whether China may step up in advancing stalled negotiations.

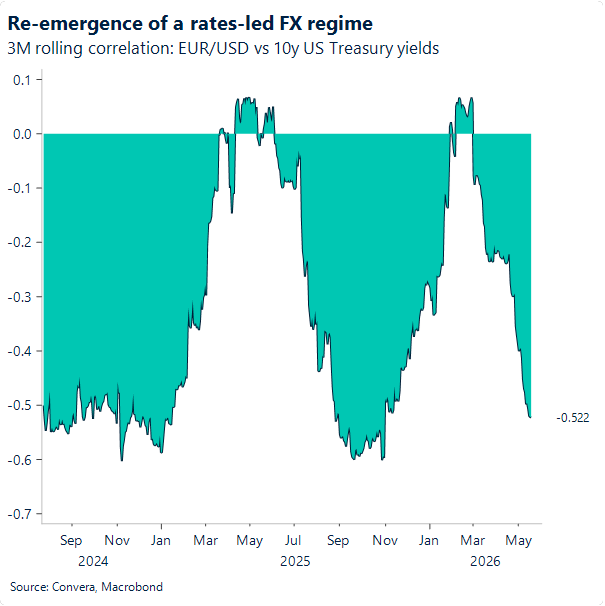

Friday’s bond sell-off offered another lens through which one can view the euro’s structural downside sensitivity to the ongoing conflict. A combination of rising real yields and inflation expectations pushed long-end bond yields higher globally, preserving some attractiveness in fixed income, as the move was not driven by a risk premium alone. The euro’s bearish reaction, however, signalled limited investor appetite to engage with higher European yields, given the region’s uncertain macro outlook amid the conflict, especially with the 2022 energy crisis still fresh in memory. Meanwhile, EUR/USD has closely tracked the inverse of US 10-year yields in recent sessions, with their inverse relationship reaching its strongest level since late 2025 on a three-month rolling basis. The pair’s bearish reaction, alongside Fed hawkish repricing and higher US inflation expectations, reinforces the view of a more credible Fed reaction function relative to the ECB, leaving the euro structurally more vulnerable in the current conflict-ridden environment.

EUR/USD appears to have consolidated around the 1.16 lows for now, as markets await clearer directional momentum from developments in the conflict narrative. That said, amid repeated failed attempts at de-escalation and thinning market patience, as illustrated by Friday’s bond sell-off, a test of 1.16 therefore appears likely even in the absence of meaningful progress in the coming days.

GBP: Pound firms as Burnham fears recede

Sterling outperformed on Monday, strengthening against all major peers despite a broad global bond sell‑off weighing on risk assets. The move appeared sterling‑specific, driven by a partial unwinding of the political risk premium that had built around the prospect of an Andy Burnham leadership challenge.

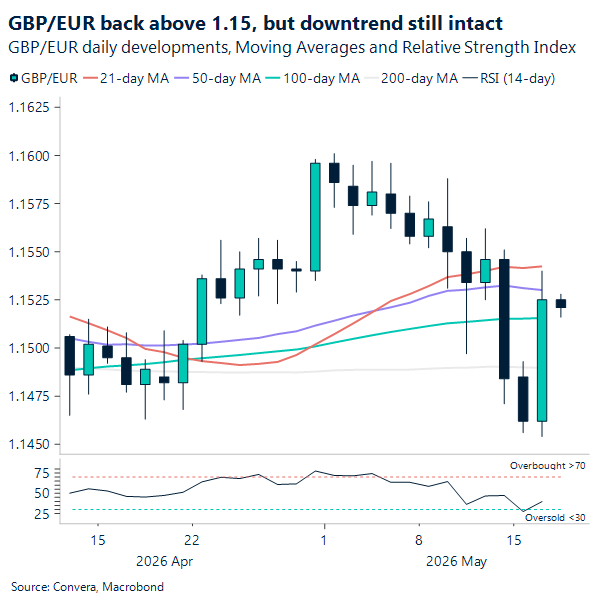

Concerns had escalated last week after Burnham, who must first win a June by‑election to be eligible to stand, reiterated support for higher public borrowing, unsettling gilt markets and dragging GBP/USD from the high‑1.36s into the 1.33 area. However, those fears eased after Burnham clarified that he would adhere to existing fiscal rules if he were to become prime minister. That reassurance stabilised UK assets, with gilt yields falling modestly across the curve and sterling retracing part of last week’s losses. GBP/USD has moved back above 1.34, while GBP/EUR has reclaimed the 1.15 handle, with both pairs tentatively back above their 200‑day moving averages.

That said, UK political uncertainty is far from resolved. A full leadership contest is likely to play out over the summer, and the lack of clarity around potential outcomes is likely to keep some investors cautious toward UK assets.

Monetary policy remains a parallel constraint. The Bank of England (BoE) faces a familiar dilemma: persistent inflation pressures alongside a cooling labour market. Today’s jobs report showed unemployment edging up to 5% and a 100k drop in payroll employment in April, reinforcing signs of easing labour demand, even as headline earnings surprised to the upside. For markets, attention now turns to tomorrow’s inflation data, though the bar to meaningfully unwind expectations for a relatively tight BoE policy path remains high.

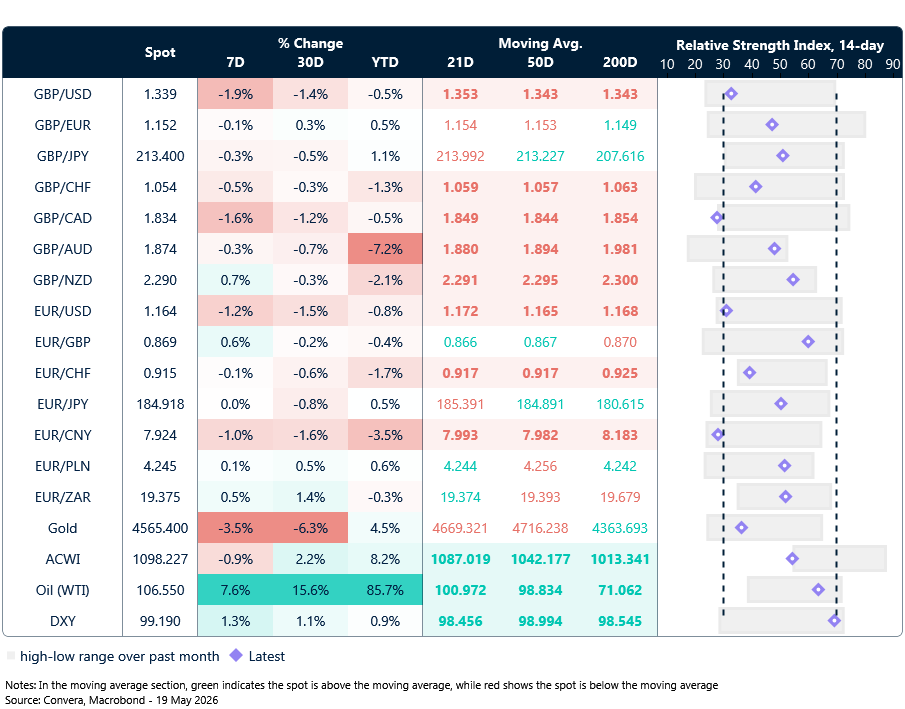

Market snapshot

Table: Currency trends, trading ranges & technical indicators

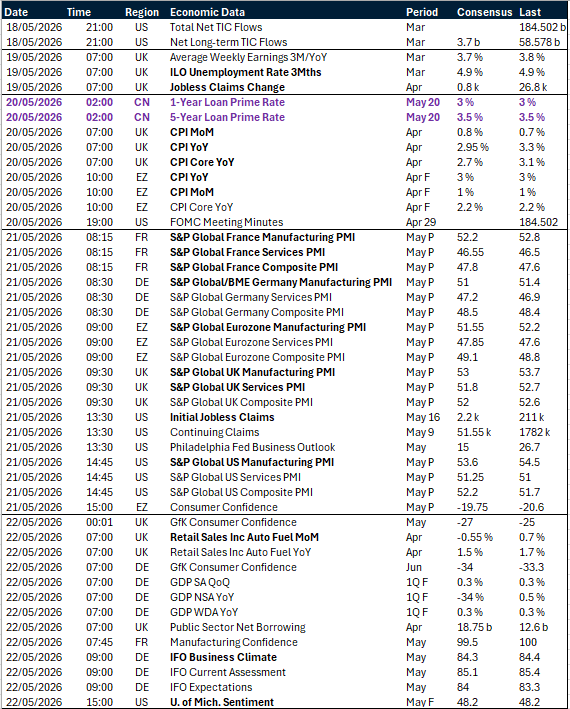

Key global risk events

Calendar: May 18-22

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.