CAD: The myth of Venezuelan displacement

The USD/CAD is currently trading around 1.3770, showing a retracement from its highest level in a month (1.3815) as markets digested the geopolitical “shock” of the U.S. military ousting the Maduro regime in Venezuela. While initial headlines triggered a knee-jerk reaction in the Canadian Dollar, amid fears that a revitalized Venezuelan oil sector would immediately displace Canadian heavy crude, the reality of energy infrastructure provides a much sturdier floor for the Loonie than the “noise” suggests. The U.S. Midwest (PADD 2) remains almost entirely dependent on Canadian oil delivered via a vast, existing pipeline network (such as the Enbridge Mainline and Keystone). PADD 2 (U.S. Midwest) is the single largest destination for Canadian crude oil exports, accounting for approximately 60% to 63% of all Canadian oil sent to the United States. Replacing these flows with Venezuelan crude would require a logistical overhaul; Venezuelan oil is tanker-borne and naturally flows to the Gulf Coast (PADD 3), not the landlocked Midwest refineries which lack the south-to-north pipeline capacity to substitute Canadian barrels. While this is a smaller share (~18%), it is the fastest-growing market for Canada and the primary area where Venezuelan oil would actually compete, as both are heavy crudes processed by the massive complex of Gulf refineries.

Furthermore, experts estimate it will take a decade and upwards of $100 billion in investment to rebuild Venezuela’s decaying infrastructure to its former glory. The primary risk for the Canadian oil industry isn’t immediate displacement, but rather a long-term loss of strategic leverage and increased price competition on the Gulf Coast, which could eventually widen the Western Canadian Select (WCS) discount if the U.S. gains a viable heavy-oil alternative.

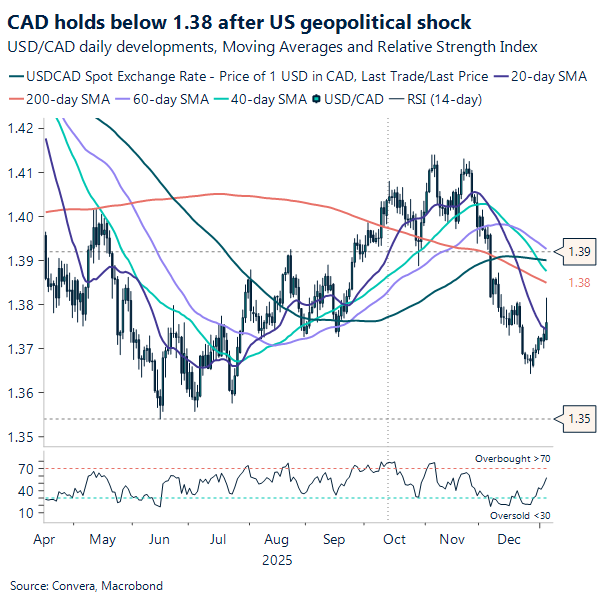

From a technical analysis perspective, the daily chart reveals a significant shift in sentiment over the last two months. After peaking near 1.4147 in November, the USD/CAD has entered a defined corrective phase, recently slicing through both its 50-day SMA (1.3901) and its 200-day SMA (1.3849). The RSI (14) is currently sitting at 44.8, which is neutral-to-bearish; it has recovered slightly from near-oversold levels but remains below the 50-midline, suggesting that bulls lack the conviction to stage a major rally. The current price action is hovering just above the 20-day SMA (1.3743), which is acting as immediate minor support.

Looking ahead, the outlook remains cautious with a slight bearish bias for USD/CAD (CAD strength) unless it can reclaim the 1.3850 level. If the pair fails to hold the current 1.3740–1.3760 zone, the next major technical target is the December low of 1.3642, followed by the psychological and structural support at 1.3550. For a bullish reversal to take hold, the market would need to see a sustained close back above the 200-day SMA, which would indicate that the “Venezuela discount” has been fully priced in and that the U.S. Dollar is regaining its broader macro appeal. In the short term, expect the pair to range-trade as traders weigh the slow-moving reality of Venezuelan production against the immediate rhetoric coming from Washington.

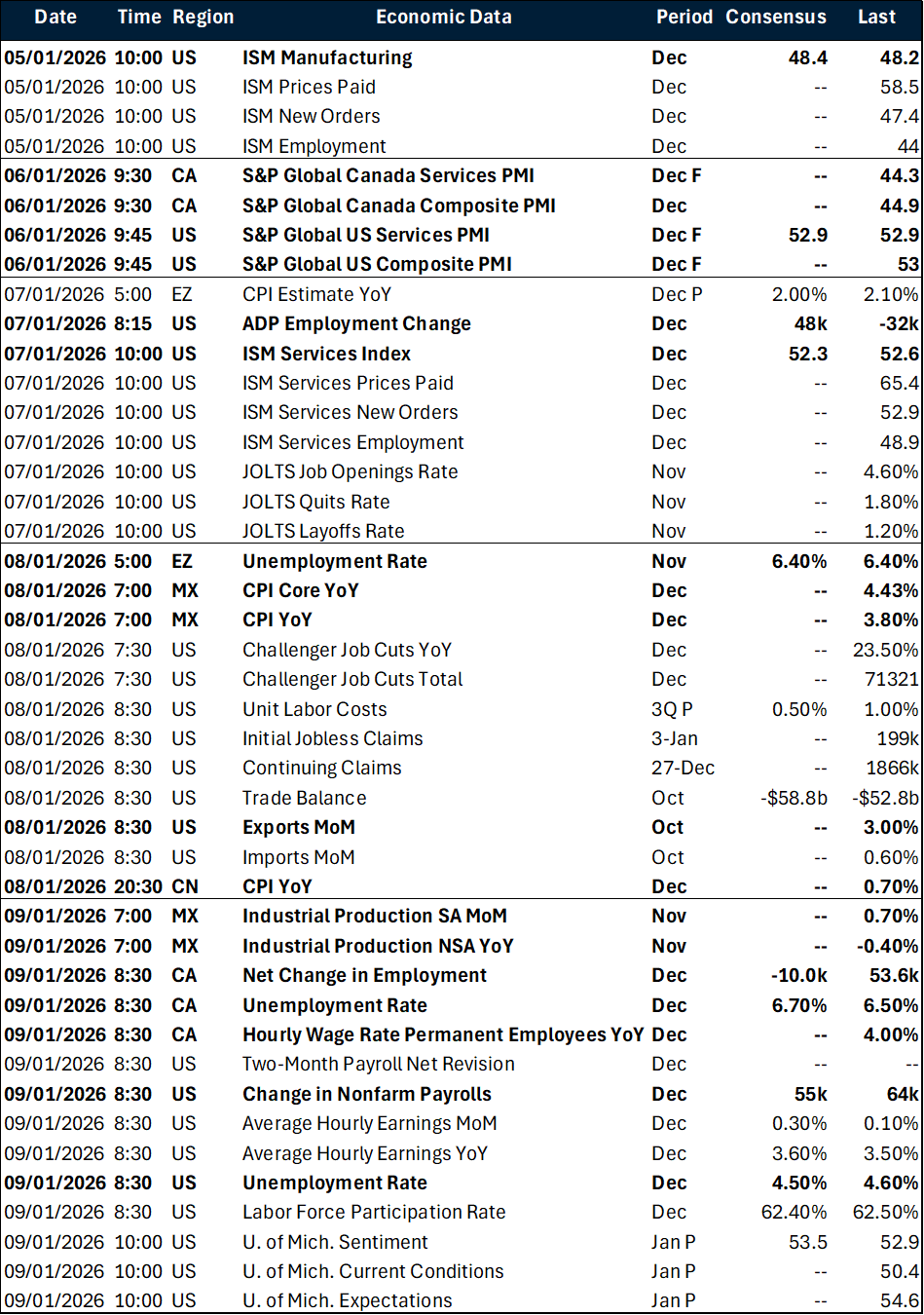

Also, this Friday, markets will closely monitor the December employment report, which is expected to show a decline of approximately 2.5K jobs and an uptick in the unemployment rate from 6.5% to 6.7%. Should the data align with these projections, the 1.37 level is likely to reinforce its role as a key short-term support for USD/CAD.

Geopolitics: Why the U.S. left the Chavista structure intact

The recent U.S. operation in Caracas to unseat Nicolás Maduro represents a shift toward “tactical decapitation” rather than a total dismantling of the state. By leaving much of the Chavista institutional framework intact, evidenced by the naming of Delcy Rodríguez as a compliant interim leader, the Trump administration has effectively engineered a “managed” government. This setup seems designed to be weak enough to remain under Washington’s thumb while performing a very specific surgical task: the aggressive purging of Chinese, Russian, and Iranian influence from South America. By keeping the existing apparatus on a short leash, the U.S. can dismantle adversary networks and reassert the “Trump Corollary” of the Monroe Doctrine without the messiness of a full-scale occupation, even if it means operating through a leadership that lacks true domestic legitimacy.

This strategic choice, however, creates a painful paradox for the Venezuelan people. While the removal of Maduro offers the first real hope for rebuilding in two decades, the decision to sideline María Corina Machado, the movement’s moral and democratic center, suggests that a true transition to democracy is being traded for geopolitical stability. On the other hand, the road to recovery will be grueling; despite sitting on the world’s largest oil reserves, the infrastructure is so decayed that it will take upwards of $100 billion and several years just to see a significant spike in production. Local private investment won’t return overnight, and as long as the U.S. prioritizes “reimbursement” through oil over sovereign democratic health, the average Venezuelan is left wondering if they’ve simply traded one form of external coercion for another.

On the global stage, this 2026 incursion is a massive gamble that could redefine international norms for the rest of the decade. By acting so unilaterally in its “near abroad,” the U.S. may be inadvertently handing a roadmap to its rivals. In Beijing, the Caracas operation is being scrutinized as a potential precedent for future moves toward Taiwan, while Tehran and Moscow are already signaling a tighter strategic pivot to compensate for their lost foothold in the Americas. As Washington moves to lock down its own hemisphere, the world risks fracturing into rigid, hostile spheres of influence where regional powers do as they please, leaving smaller nations and democratic movements caught in the crossfire of a new, high-stakes Cold War.

MXN: Carry + credibility sustains Peso’s gains

A “regime shift” bear case centers on the potential for a rapid dissolution of the Peso’s scarcity premium as the Venezuelan “CAPEX story” pivots to an “infrastructure fast-track.” If the new U.S. administration moves beyond blockades to active “reconstruction” partnerships, the timeline for re-integrating heavy Orinoco barrels could collapse from a decade to 24–36 months. In this scenario, the FX market would stop treating Caracas as a distant CAPEX project and start pricing it as a looming supply glut. For the MXN, this would mean a double-sided squeeze: a narrowing of Mexico’s trade surplus as heavy crude competition intensifies, alongside a “haven rotation” back to the USD as geopolitical uncertainty in the Americas recalibrates toward a U.S.-led hegemony.

This week, emerging‑market equities hit new all‑time highs. And while the long‑term implications of U.S. actions in Latin America remain uncertain, the carry‑plus‑credibility narrative continues to support the ‘Super‑Peso’ as we move into 2026.

On the other hand, the “Carry + Credibility” narrative is highly sensitive to the widening growth-policy divergence between Banxico and the Fed. While the Dec 18 cut to 7.00% was framed as data-dependent, a prolonged slump in Mexican domestic demand, highlighted by eight straight months of negative fixed investment, suggests that Banxico may be forced into a more aggressive easing cycle than currently priced. If the Fed maintains its “higher-for-longer” pause while Banxico chases a cooling economy, the “yield cushion” that currently protects the Peso from headline risk will deflate. In such a environment, the market’s current “prioritization of policy over politics” could flip instantly, leaving the MXN exposed to a “catch-up” depreciation as the 17.80–18.00 support level gives way to a fundamental re-rating toward 19.20.

Market snapshot

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: January 5 – 10

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.