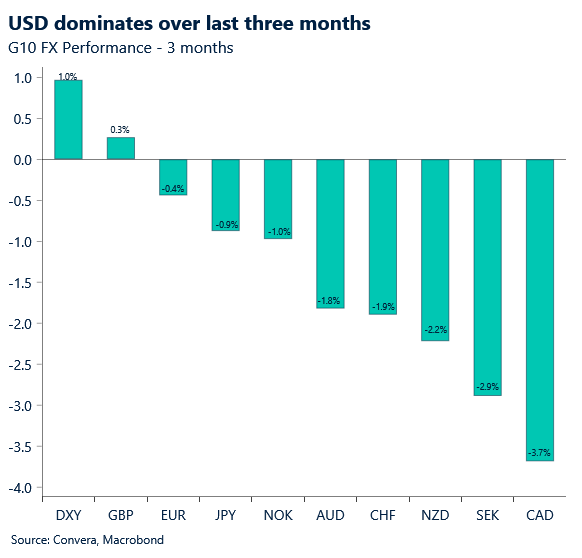

Greenback extends losses

The US dollar weakened last week as expectations for Federal Reserve rate hikes eased, especially after a significant miss in the June jobs report.

Market activity was subdued over the US Independence Day long weekend, allowing the Aussie and other currencies to gain ground.

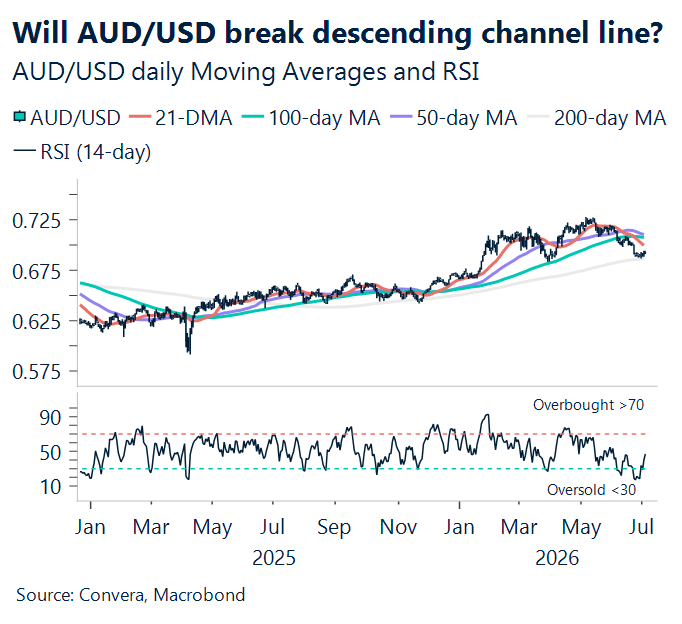

The Australian dollar has reclaimed its position as the best-performing G10 currency, with AUD/USD rising 0.3% on Friday and 4.0% year to date.

NZD/USD gained 0.3% on Friday, extending last week’s rebound from major support at 0.5600.

In Asia, USD/JPY retreated from 40-year highs following a sharp reversal after last week’s US jobs report. USD/CNH and USD/SGD both fell 0.1%.

AUD/USD looks to break higher

Australia’s services sector returned to growth in June, with the S&P Global Services PMI rising to 50.5 from 48.7 in May, driven by stronger consumer-related activity. Increased hiring supported output growth, although demand remained soft, with new orders falling for a fourth consecutive month and export orders declining again amid disruptions linked to the conflict in the Middle East.

While input cost pressures eased, they remained elevated, and businesses slowed the pace of price increases to the weakest level since January. Without an improvement in demand, the recovery may struggle to gain momentum.

A sharp miss in US jobs data and concerns over potential political influence on interest rate policy pushed the US dollar lower, although regional currencies continue to move in different directions.

AUD/USD is testing resistance from its descending channel while trading 5% below its May peak of 0.7278. To reinforce the upward move, AUD/USD needs to break above its 21-day EMA at 0.6979, followed by its 100-day EMA at 0.7016. On the downside, 0.6900 remains the next key support level.

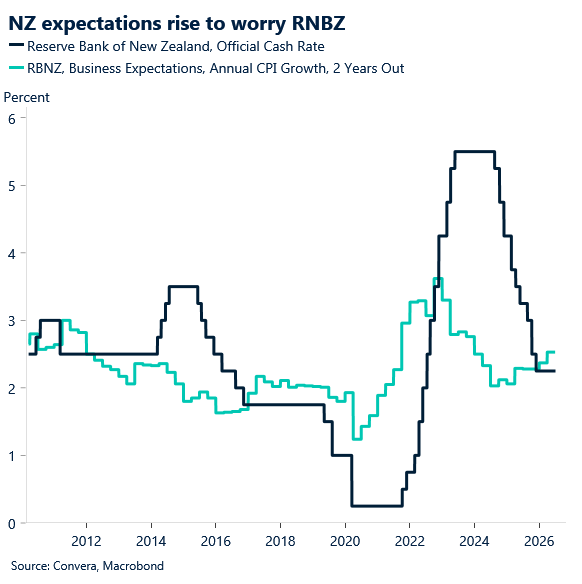

RBNZ in focus this week

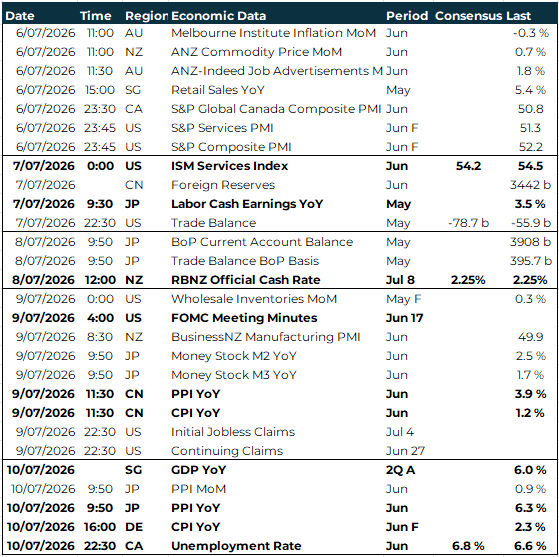

The Reserve Bank of New Zealand’s rate decision on Wednesday is the week’s only major central bank meeting, with consensus expecting the official cash rate to rise to 2.50% from 2.25%. Any surprise could trigger outsized moves in the New Zealand dollar. The FOMC minutes from the June meeting follow early Thursday morning, offering further insight into the Fed’s policy debate.

Thursday brings China’s June CPI and PPI data, last reported at 1.2% and 3.9% respectively, providing an important read on inflation momentum. Japan’s PPI on Friday, currently running at 6.3%, and Germany’s final June CPI will round out the week’s inflation releases, while the Melbourne Institute inflation gauge opens the week on Monday.

The US ISM Services PMI on Tuesday is expected to ease to 54.2 from 54.5. Singapore’s advance Q2 GDP estimate on Friday follows a strong 6.0% reading in the previous quarter.

Japan’s labour cash earnings data are due on Tuesday, US jobless claims are released on Thursday, and Canada’s unemployment rate on Friday is forecast to edge up to 6.8% from 6.6%.

Aussie back to two-week highs

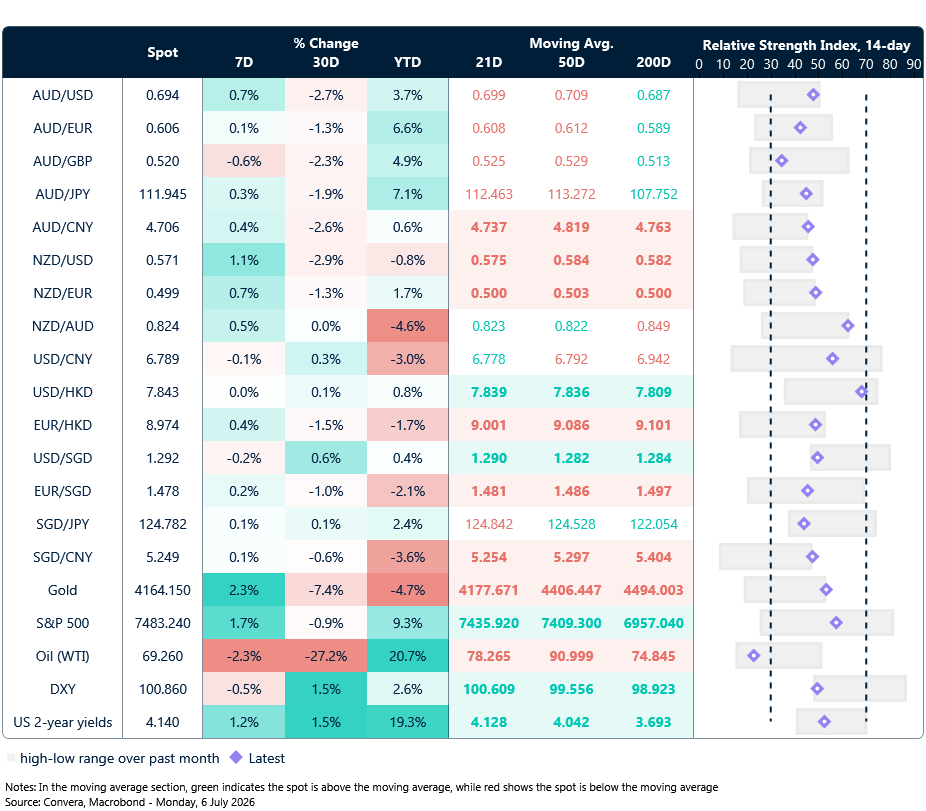

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 6 – 10 July

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.