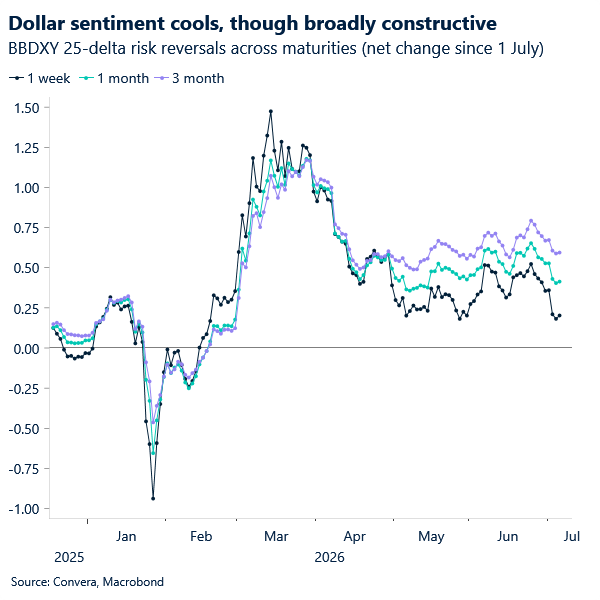

USD: DXY consolidates near 15-month highs

The US dollar’s rally has lost some steam after the DXY reached a 15-month high of 101.800 on 24 June. A softer-than-expected US jobs report last Thursday added to the pullback. Markets are becoming increasingly demanding of data that can justify a hawkish Fed stance, particularly as lower oil prices continue to ease inflation concerns.

Last week’s sharp move in the dollar and short-end yields following the NFP release highlighted just how confident investors had become in the Fed delivering a more hawkish policy path. Fed Chair Warsh adds another wrinkle. Markets initially embraced his hawkish tone, but that was largely relief-driven after months of fears he would lean dovish. Investors are now beginning to recognise that Warsh’s scepticism towards forward guidance does not necessarily make him a committed hawk, unwinding tightening bets more readily on dovish data misses.

Meanwhile, reports have emerged that President Trump and close allies are exploring ways to remove members of the Fed’s Board of Governors after the Supreme Court blocked an effort to dismiss Governor Lisa Cook last week. The move is widely viewed as another attempt to reshape the FOMC with policymakers more aligned with Trump’s dovish policy preferences.

While this is not a theme to which the dollar is likely to respond immediately, it was only earlier this year, in January and February, that the greenback came under pressure following reports that the US Department of Justice had launched a criminal investigation into the Fed. Questions surrounding the Fed’s independence remain important and could attract greater market attention as geopolitical risks fade out later in the year.

With nothing major on the data calendar until next week’s US CPI report, consolidation within the 100–101 range appears the most likely near-term outcome. Initial support is seen in the 100.60/80 area, where the 21-day moving average sits. Below that, stronger support comes in at 100.20/00.

EUR: Euro steadies

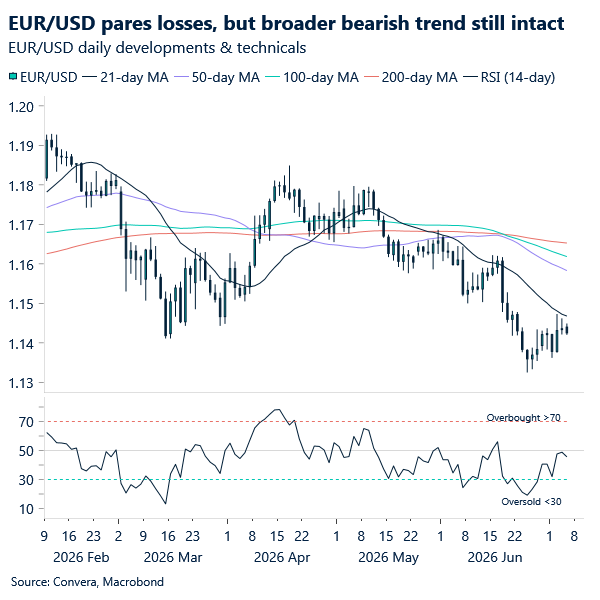

EUR/USD closed last week 0.5% higher. However, it continues to trade just below its 21-day moving average near 1.1470, keeping the broader bearish bias intact. The pair has declined steadily from April’s high at 1.1849, as receding geopolitical risks have led to a sharper unwind of ECB rate hike expectations relative to those for the Fed.

Last week’s eurozone CPI report provided further evidence that disinflation is not solely being driven by lower oil prices. Softer readings in both services and core inflation added weight to the argument that second-round effects from the energy shock may prove more limited than initially feared. As a result, the case for a prolonged ECB pause has become increasingly compelling.

That said, we are not convinced EUR/USD has substantial downside from current levels. The Fed is also subject to the disinflationary effects of lower oil prices and, while the stronger US macro backdrop supports a relatively sticky tightening bias, a full pricing-out of further Fed hikes later this year is becoming increasingly likely. That should help provide some underlying support for the euro.

For this week, we expect EUR/USD to consolidate in the 1.14 handle, as the light data calendar is unlikely to generate meaningful directional momentum. Resistance is seen near 1.1450/70, followed by the 1.15–1.1520 area, while support around 1.1350 should remain firm.

GBP: Strong GBP week, fragile story

Sterling posted its strongest weekly gain against the dollar since early April, erasing most of the losses incurred following the Fed’s hawkish June policy meeting. GBP/USD closed the week 1.1% higher.

The pair has moved back above its 21-day moving average near 1.33. The 1.34–1.3440 area now stands out as key resistance, with a break higher needed to challenge the broader downtrend that has been in place since early May.

This week, Starmer could outline a timetable for his departure. Confirmation of a swift and orderly transition should be modestly supportive for sterling. Nevertheless, dollar strength remains the cleaner narrative. Arguing for a sustained break above 1.34 solely because the UK political backdrop appears somewhat less negative than before still feels like a stretch to us.

Meanwhile, inflation expectations eased further in June, according to the closely watched Decision Maker Panel survey. One-year-ahead inflation expectations fell to 3.3%, below the 3.6% consensus estimate and down from 3.7% in May. The backdrop reinforces the view that inflation risks are receding as oil prices continue to unwind their conflict-driven gains, strengthening the case for a prolonged BoE pause rather than further rate hikes.

We expect these views to come through more clearly at the policy meeting later this month, particularly with June’s inflation report due the week before. This dovish recalibration should weigh on sterling.

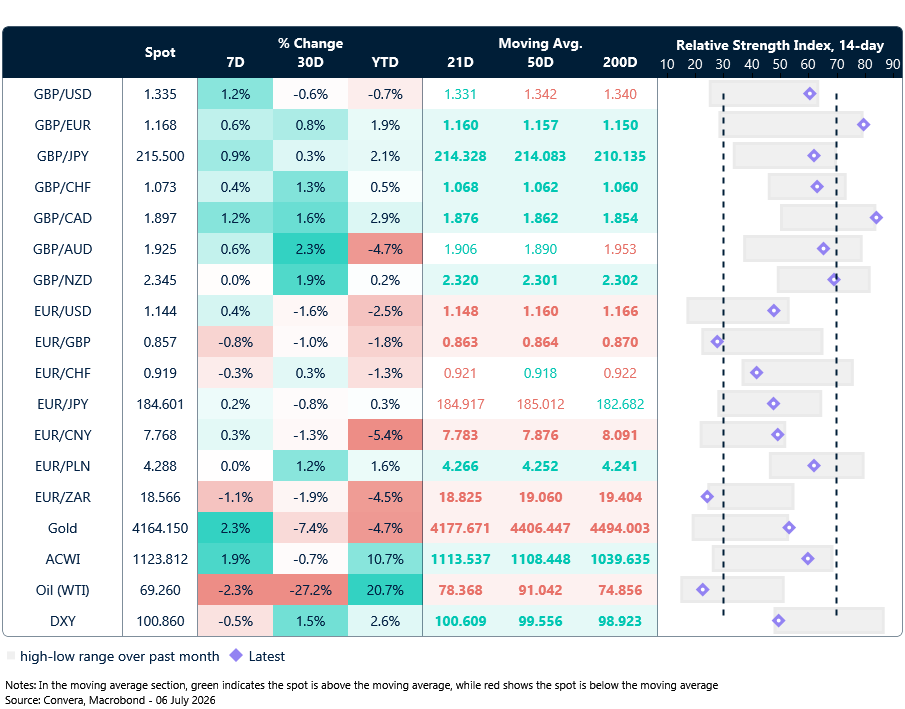

Market snapshot

Table: Currency trends, trading ranges & technical indicators

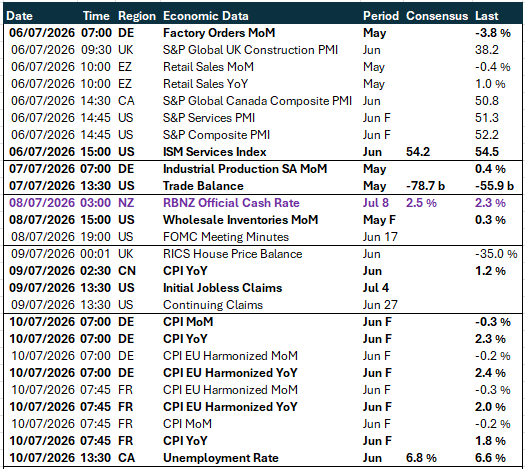

Key global risk events

Calendar: 6 July – 10 July

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.