Fresh threats renew Canada–US friction

Late Thursday, President Donald Trump announced that the U.S. will impose a 35% tariff on Canadian products starting August 1. It remains unclear whether this move is intended to pressure Canada’s trade negotiation team into offering further concessions, but the Canadian government now has less than three weeks to avoid these higher tariffs.

Following the announcement, the CAD initially rose to 1.373. However, U.S. officials later clarified that goods compliant with CUSMA will remain exempt, offering some relief to bilateral trade. Still, the timing isn’t ideal, as Canada prepares for key macro data releases today, and the Bank of Canada’s policy decision later this month.

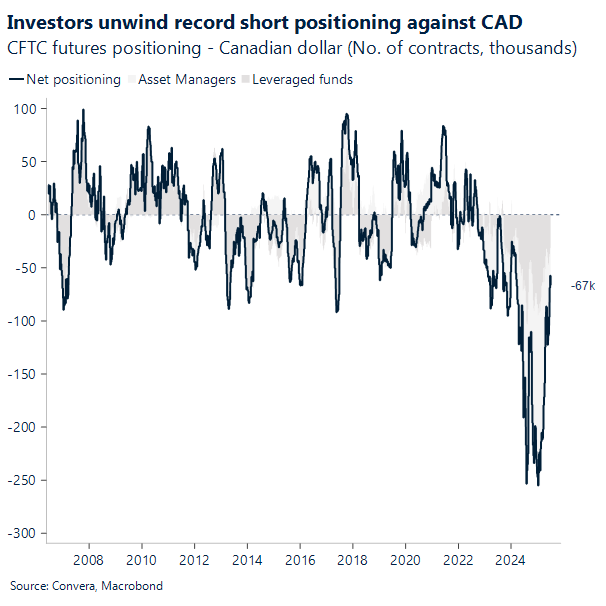

Fresh tariff threats have dampened the rebound in sentiment toward the CAD, which had been benefitting from an unwinding of historical short positions. Investor outlook has shifted from expecting a sharp economic contraction, given Canada’s reliance on U.S. exports, to anticipating a more moderate slowdown. While data indicates that trade-exposed sectors are already feeling the strain, the broader economy continues to show resilience. Still, Canada now faces uncertainty as it braces for the full impact of the trade conflict, and hopes for a near-term deal appear increasingly fragile.

So far this month, the USD/CAD has rebounded from 1.355, near its 40-month moving average of 1.358, rising to 1.373 and ending a five-month downward streak. The pair had fallen from a two-decade high of 1.479 to a 2025 low of 1.354 on June 16. While it attempted to extend the downtrend this month, marking a fresh low at 1.355, it has struggled to hold below 1.36. This price action has formed a potential double-bottom near its three-year average of 1.363. As the U.S. dollar sheds its bearish bias following tariff headlines, the Canadian dollar remains under pressure. It now trades above its 20-day moving average (1.366) and, if employment data disappoints on Friday, could break through the 40-day moving average (1.371). The next resistance level is the 60-day moving average at 1.376. Statistically, July tends to be a quiet month for the Canadian dollar, with largely flat returns over the past decade.

Dollar climbs as Fed remains split and Trump ramps up tariffs

The Fed’s June meeting revealed a resilient economy still battling high inflation—and a divided stance on where policy goes next. Most of the split came down to speculation more than conviction, thanks to an outlook clouded by uncertainty.

Until the policy debate kicked in, the minutes struck a clearly hawkish tone. Fed economists hammered home the same message: inflation remains elevated, while GDP and overall activity are holding steady. Longer-term inflation expectations stayed anchored, which was the main signal they leaned on.

The dot-plot painted a murky picture, with most officials agreeing that policy should ease later this year—assuming tariff-driven inflation fades and growth cools.

In short, it’s still a wait-and-see game. Two members—Bowman and Waller—hinted a rate cut could happen as early as July, but only if the data shifts in line with their forecasts. Bottom line: the Fed’s tough now, but it’s ready to soften if the economy falters.

Meanwhile, the dollar inched up Friday morning in Asia, with the Dollar Index touching 97.80 after President Trump dropped a fresh round of tariffs. He announced blanket duties of 15–20% for remaining trade partners, plus a 35% hike on Canadian imports starting August 1.

The new levies, separate from existing ones, could rise even more if Canada pushes back.

The Dollar index has rebounded sharply, up nearly 2% from its 3-year lows of 96.38.

As we’ve iterated previously in APAC dailies, we are positive on the dollar index. Chart shows the sentiment on the dollar has turned slightly positive.

Euro & Sterling: At the mercy of U.S. macro

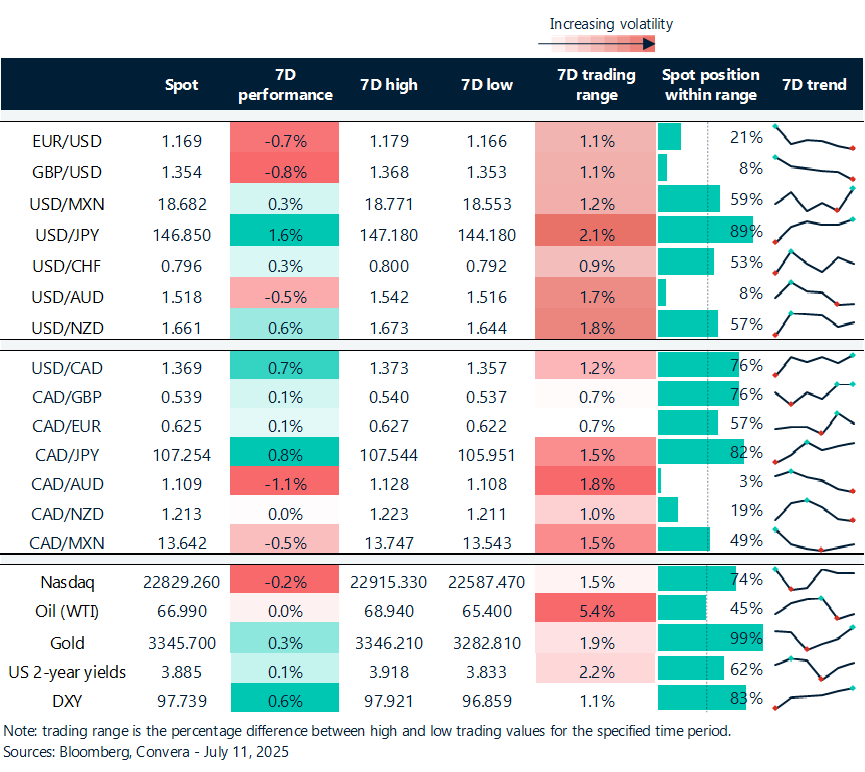

It’s undeniable that both euro and sterling had an impressive H1, up 13% and 8% year-to-date, respectively. However, with minimal data releases driving FX this week, yet heavy in trade headlines, markets had a blank canvas to observe, more clearly, a pivotal shift in the engine behind these strong performances—one that moves beyond sentiment and instead seeks validation of those fears tied to U.S. policy risks as the new driver of momentum.

Trump’s latest threat to impose 50% tariffs on Brazil—based solely on domestic political issues surrounding the treatment of former President Jair Bolsonaro—was perhaps the most striking example yet of just how unpredictable his administration can be. It highlights a tendency to consider non-economic factors when shaping trade policy, despite the surprising fact that the U.S. currently holds a trade surplus with Brazil.

And yet, the dollar edged higher while both the euro and sterling continued their weekly declines. As outlined in yesterday’s report—both from a fundamental and technical perspective—this fading momentum is already well established. Euro and sterling are down circa 1% against the dollar week-to-date.

Looking ahead, for these rallies to regain strength, markets need one thing: macro data-driven evidence that the U.S. economy is truly deteriorating as a result of the tariffs. And this should re-ignite that sentiment-driven dollar sell-off we saw in the months leading up to summer. At present, the mere uncertainty surrounding their implementation no longer provides sufficient fuel to drive further euro and sterling upside.

Should the U.S. economy remain resilient and inflation prove sticky—thus lowering expectations for Fed rate cuts in the near term—a bearish correction for both euro and sterling becomes increasingly likely. Next week’s U.S. inflation data will be critical in validating that outlook.

Domestic drags and global jabs

GBP/EUR saw moderate gains this week before paring back all progress following disappointing UK macro data released Friday’s morning. The pair is up 0.01% week-to-date at the time of writing.

As market sentiment was driven largely by external factors – namely tariffs headlines – sterling managed to gain relative to the common currency thanks to reduced uncertainty, having already secured a deal with the U.S.

This morning, however, the pound came under pressure on its own merits: GDP and industrial production missed expectations, causing GBP/EUR to slip over 0.1% since the Asia market open.

Overall, domestic headwinds—including markedly tighter fiscal policy, the lagged effects of previous interest rate hikes, and a cooling job market—have been compounded by U.S. trade actions, setting the tone for continued weakness in UK growth.

Looking ahead, the UK labour market data due next week will be closely watched. A cooling jobs market has been a key driver behind the BoE’s more dovish stance recently, and confirmation of that trend will likely reinforce expectations for additional rate cuts, pushing sterling lower.

Risk-on mode continues despite fresh tariff threats

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: July 7-11

All times are in ET

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.