USD: End of conflict optimism sends oil lower

Starting the week, crude oil futures slipped back below $100 a barrel after US officials signaled optimism about a possible agreement with Iran. The move reflects hopes for a 60-day ceasefire extension and, ultimately, the reopening of the Strait of Hormuz. But the outlook remains far from clear. Tehran has yet to embrace the framework, and several key provisions remain unresolved. Absent tangible progress, the latest pullback in oil looks fragile. If diplomacy falters, Brent could quickly reclaim the $100 mark.

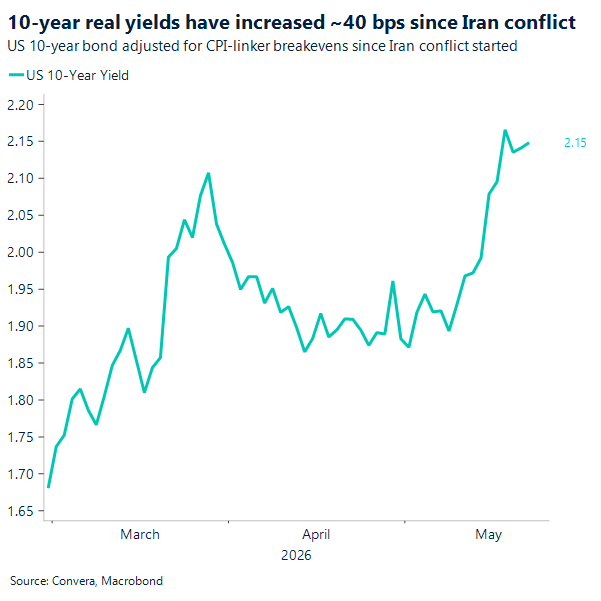

The broader macro consequences have been persistent and loud over the last couple of weeks. Elevated energy uncertainty is colliding with still-sticky inflation, complicating the task for central banks. Since the conflict began, US 10-year real yields have risen roughly 40 basis points to 2.15%. Starting the year, for the most part, markets anticipated rate cuts and are now entertaining the possibility of a year-end Fed hike. The message is familiar but increasingly entrenched: higher-for-longer is no longer a cautionary phrase, but a market reality. That has widened the gap between uneasy households and remarkably composed financial markets.

For now, equities continue to look through the tension. Global stock benchmarks have pushed to fresh highs, buoyed by enthusiasm for structural technological change rather than concern over near-term geopolitical risk. Last week, strong corporate earnings, led by Nvidia’s striking $81.6 billion in quarterly revenue, have reinforced that conviction. So even as disrupted shipping lanes and potential energy shortages threaten the real economy, Wall Street remains focused on the AI story.

What’s happening in markets this week?

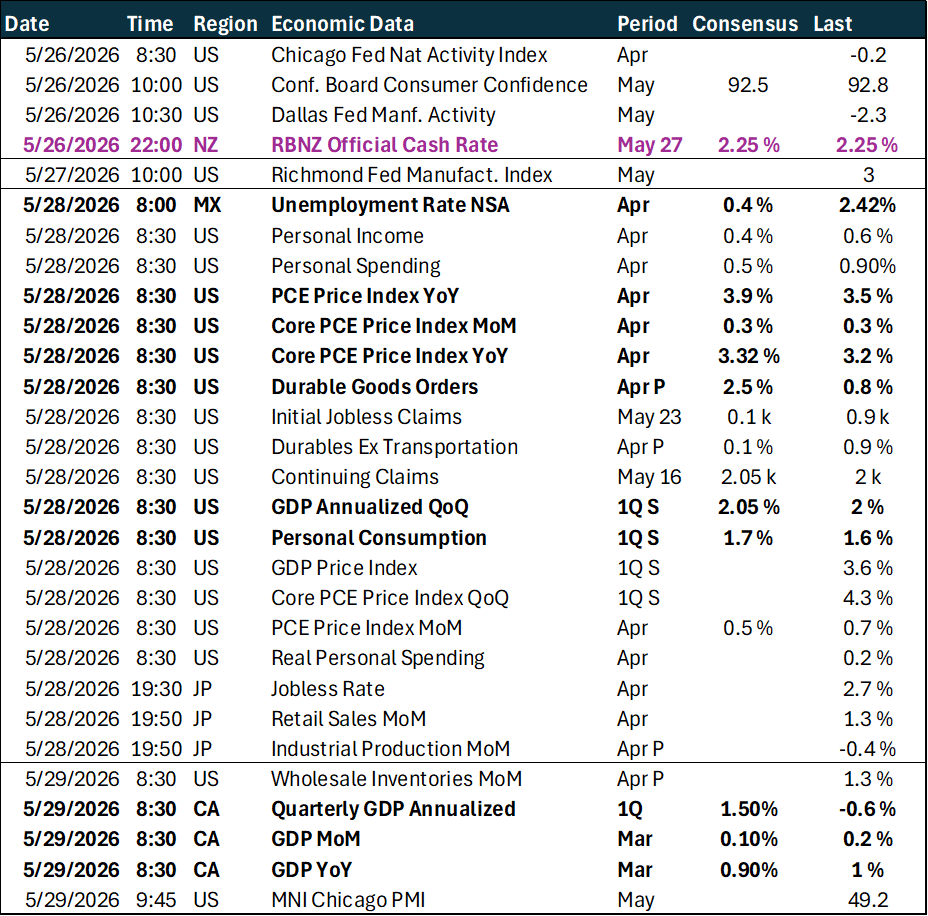

The week opens quietly, with US and UK public holidays (Mon) limiting early activity. Focus then turns to US consumer confidence (Tue) for signals on whether softer sentiment is beginning to affect spending. Australia’s CPI (Wed) is expected to remain elevated near 5%, reinforcing ongoing inflation pressures, while the Reserve Bank of New Zealand (Wed) is widely expected to leave rates unchanged. Japan’s 40-year bond auction (Wed) will test demand for long-dated issuance against a backdrop of still-elevated global yields.

Attention shifts to a heavier data slate later in the week. The Bank of Korea’s decision (Thu) underscores increasingly divergent policy paths across central banks. In the US, a dense run of releases (Thu), including GDP, personal income and spending, durable goods, jobless claims, and core PCE, will be closely watched, with core inflation expected near 3.3% year-over-year. Friday brings Japan’s labor, activity, and inflation data (Fri), along with preliminary CPI prints from Germany, France, Italy, and Spain (Fri) and Germany’s unemployment rate (Fri). Canada’s GDP (Fri) concludes the week, offering a final read on growth momentum.

CAD: Yield differential pushes USD/CAD higher

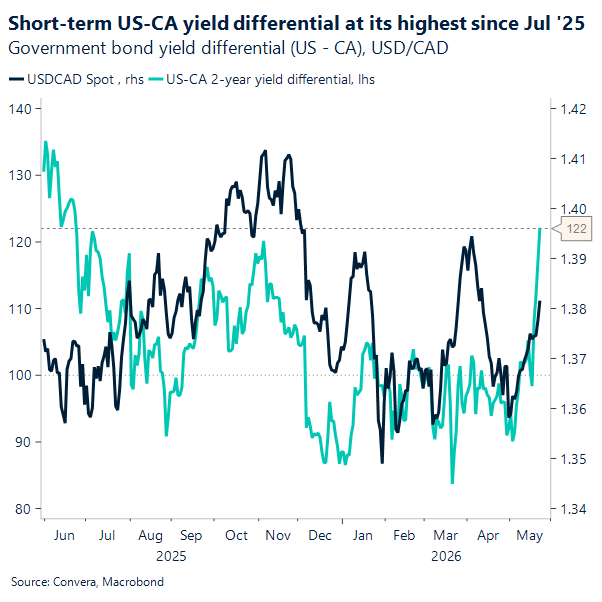

USD/CAD’s move higher since mid-May has been a clean expression of widening relative-rate support for the dollar. Hotter US inflation data helped push markets back toward a higher-for-longer Fed view, while Canada entered the move with little fresh macro momentum strong enough to offset the softer labour backdrop. That left the pair trading less on idiosyncratic noise and more on the simple fact that US yields were moving higher, faster, and with more conviction.

What has made the move more durable is the broader shift in market leadership. The macro backdrop has reasserted itself as the dominant driver as yields rise, inflation expectations edge higher, and financial conditions tighten through rates rather than policy. Equities have absorbed that adjustment better than expected so far, but the underlying FX message has been clearer: where yield support is backed by a firmer inflation and policy backdrop, the dollar is regaining traction. In that environment, USD/CAD remains one of the cleaner ways to track when macro reasserts itself as the dominant driver.

The US–Canada 2-year yield differential has widened to roughly 122bp, its widest level since July 2025, and USD/CAD has climbed alongside it toward the upper end of its recent range. That is exactly what a relative-momentum market should look like: the US retains the yield advantage, Canada lacks a sufficiently strong domestic impulse to push back, and the Loonie remains vulnerable while that imbalance holds. Unless US yields roll over decisively or Canada delivers a materially stronger domestic surprise, the bias in USD/CAD still looks skewed toward further upside.

MXN: Peso strength defies weak domestic backdrop

The Mexican peso has remained notably firm despite a weaker domestic outlook and a recent sovereign downgrade. Moody’s move to Baa3 was largely absorbed by markets, with concerns around subdued growth, fiscal slippage, and Pemex already reflected in positioning. Banxico’s May minutes reinforced the softer backdrop, highlighting a 0.77% contraction in first-quarter GDP. With inflation easing to 4.45% in April, policymakers delivered a 25-basis-point cut, taking the policy rate to 6.50% and signaling an end to the easing cycle that began in early 2024.

Rather than undermining the currency, the shift in policy has been offset by supportive external conditions. A softer dollar and steadier global risk sentiment have sustained demand for higher-yielding emerging market assets. Banxico continues to point to the peso’s favorable carry, supported by a still-wide real rate differential and a manageable external balance, allowing investors to look through weaker domestic fundamentals.

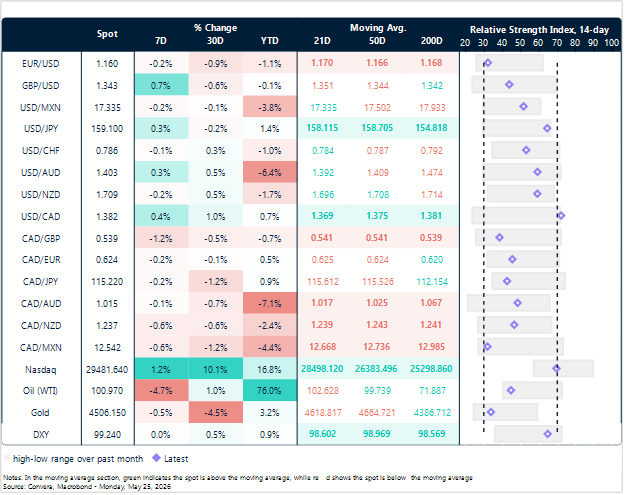

In technical terms, the USD/MXN remains range-bound within a broader downtrend. Spot is trading near 17.3, close to its 20-day moving average. Resistance is clustered around 17.50–17.52, while support holds near 17.10. A break below that level would suggest a move toward 17.00, while a sustained push above resistance could shift focus back toward the upper end of the recent range.

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

Calendar: May 25 – 29

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.