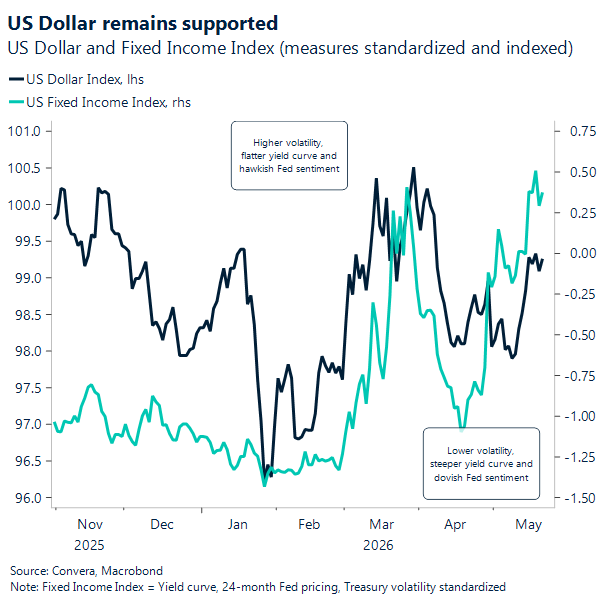

USD: US-Iran headlines keep markets whipsawing

Yesterday, stocks finished slightly higher after a choppy session, oil edged lower, and US Treasury yields extended their decline. The driver was the same familiar mix of optimism, doubt, and rapid-fire headlines around US–Iran talks.

Early enthusiasm cooled after it was reported that no deal has been reached, even if the gaps have narrowed, citing a senior Iranian source. Two issues continue to hang over the conversation: Iran’s uranium enrichment and control over the Strait of Hormuz, which keeps the “risk premium” in energy alive. It also means every incremental update can still move rates and the dollar in a hurry, especially with positioning already leaning into a narrow range.

Against the noise, the Fed message has been the steadier anchor. The April 28–29 FOMC minutes showed officials increasingly worried that inflation could take longer than expected to return to 2%. A majority also pointed to the possibility that additional policy firming could become appropriate if inflation stays persistently high. Just as important, “many” participants would have preferred removing language that markets read as an easing bias. In plain terms, the Fed is trying to stop investors from sprinting toward rate cuts before the data earns them. That is showing up in pricing, where expectations are skewed toward a prolonged hold, and the hurdle for the next cut looks higher than it did a few months ago.

Oil is the part of the equation that keeps making the Fed’s job harder. Pump prices remain sticky, and that keeps the household inflation narrative loud even when core measures cool. Demand also has not cracked cleanly. Recent US retail spending suggests bigger tax refunds helped cushion consumers as gasoline prices rose, which can delay the point where fuel costs force a more visible pullback. If that buffer fades while energy stays elevated, the squeeze can show up quickly in both sentiment and spending.

Earnings are reinforcing that same macro loop. Walmart’s results suggested the consumer is still functioning, with comparable sales at Walmart-only US stores up 4.1% excluding fuel. At the same time, the company highlighted how higher fuel costs can bite, particularly through delivery and fulfillment. When a scale player works to protect low prices, the margin pressure is a real-time reminder that the inflation impulse is not purely theoretical. Investors heard that tension in the guidance, and the stock reaction reflected how quickly “good” demand news gets filtered through the inflation lens.

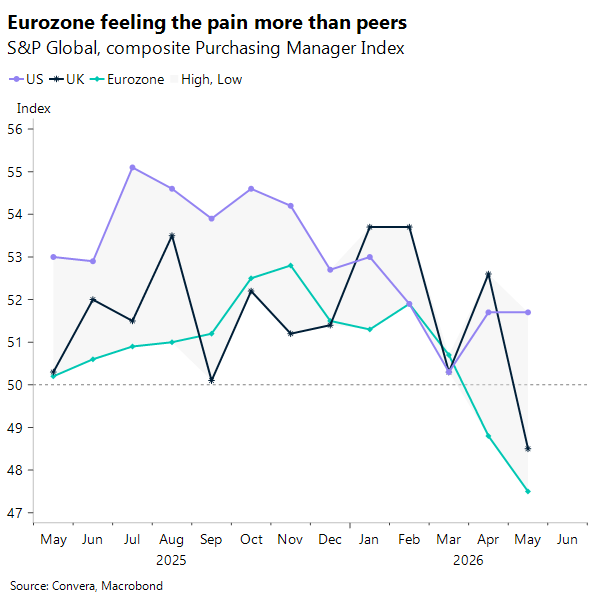

The growth backdrop is also starting to look more split. The latest PMI shows the US holding around the low-50s while much of Europe sits below 50 and has weakened over the past three months. France stands out on the downside, while the Eurozone, Germany, and the UK remain soft. This kind of US–Europe divergence tends to support relative US resilience, but it can also keep global inflation signals messy. Softer Europe can dampen goods demand, yet tighter energy and steadier US activity can keep headline inflation risks alive.

Put it all together and the market’s rhythm stays intact. Oil headlines lift inflation risk, the Fed’s “higher for longer” posture stays sticky, and even solid earnings have to clear the same question: how long can the economy absorb expensive energy without inflation re-accelerating or margins giving way. Into a long weekend, that push-and-pull is still the cleanest way to frame what is moving rates, the dollar, and risk.

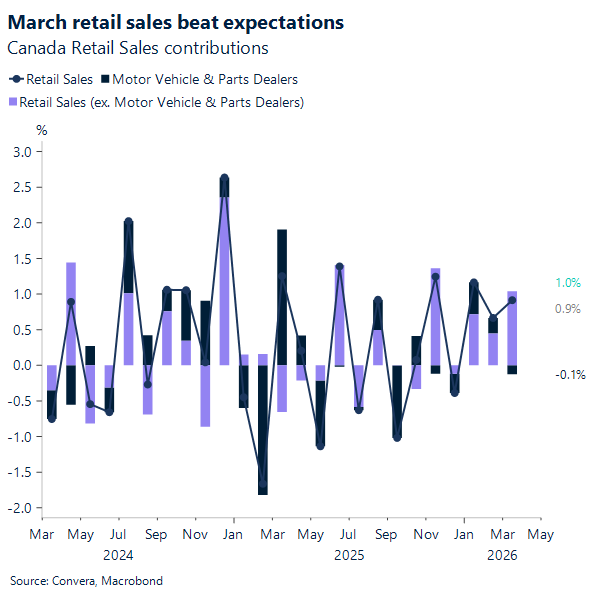

CAD: March retail sales beat estimates

Canadian retail sales easily beat expectations this March by climbing 0.9% to reach a solid $72.7 billion. The data outpaced the consensus survey estimate of just 0.6%. Much of this boost came directly from the pumps. In fact, sales at gasoline stations surged 12.4% because of higher fuel prices linked to overseas supply shocks. When you exclude the auto sector, the monthly jump looks even more impressive at 1.4%. However, overall sales volume actually dipped by 0.7%, meaning higher prices drove most of these top-line revenue gains.

Underneath the strong headline numbers, core retail spending told a slightly different story. Core sales edged down 0.1% due to slower business at building material and garden supply dealers. Car sales also took a small hit, dropping 0.5% primarily from a decline in the used vehicle market. Looking past these minor dips, online shopping remained a bright spot and grew 1.5% for the month. Moving forward, the retail momentum seems ready to continue. Early estimates suggest another 0.6% advance for April, showing that consumer spending is largely holding steady despite paying higher prices at the pump.

Despite the beat, the data has done little to support the Loonie, as the broader force keeping the Canadian Dollar under short-term pressure is the diverging macro gap between the US and Canada. Resilient economic readings and firmer inflation data south of the border stand in sharp contrast to Canada’s cooler economic performance, naturally favoring a US Dollar buoyed by higher yields and oil prices. Even after a sharp, temporary mid-week dip down to a low of 1.373, buyers quickly stepped in to buy the layout, pushing the CAD above 1.38. However, the trading range has narrowed and volatility has dropped. For now, as long as this relative macro differential persists, the path of least resistance for the USDCAD remains skewed to the upside.

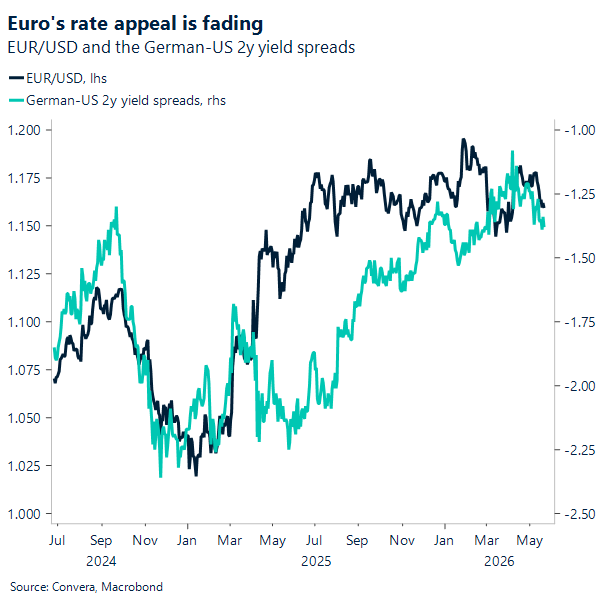

EUR: From stability to building downside pressure

EUR/USD has traded broadly flat on the week, holding around the 1.16 area, but this masks a meaningful shift in underlying dynamics. Beneath the surface, a combination of bond market turbulence, widening US–euro area data divergence, and a reversal in rate differentials has tilted the balance more clearly to the downside.

Earlier in the conflict, narrowing German–US yield spreads provided a degree of support for the euro, as markets priced a more hawkish ECB relative to a Fed seen as insulated from the inflation shock. That dynamic has now faded. In the wake of stronger US inflation prints and resilient activity data, rate differentials have moved back in the dollar’s favour, returning to pre‑conflict levels.

At the same time, Eurozone data has continued to weaken, reinforcing the divergence. This week’s PMI releases pointed to a fragile growth backdrop, with survey data consistent with a potential contraction in Q2, while US indicators remain firmly in expansionary territory. The result is a growing mismatch: a eurozone economy losing momentum versus a US economy still showing resilience.

Positioning adds to the risk. With asset managers and leveraged funds still long euros, the market appears vulnerable to a deeper unwind. In the absence of tangible progress on US‑Iran negotiations, the combination of resilient US growth, a less credible ECB tightening path, and elevated geopolitical uncertainty points to further downside.

Bottom line: The euro has shifted from being supported but capped to increasingly exposed, and without a clear de‑escalation catalyst or reversal in rate dynamics, EUR/USD risks extending lower toward the 1.15 area in the near term.

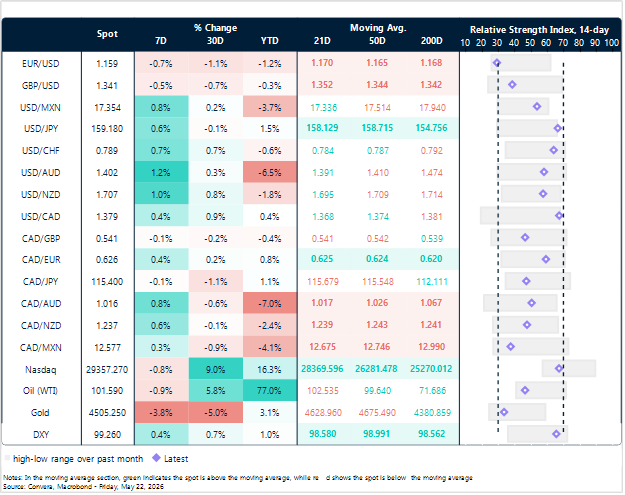

Market snapshot

Table: Currency trends, trading ranges & technical indicators

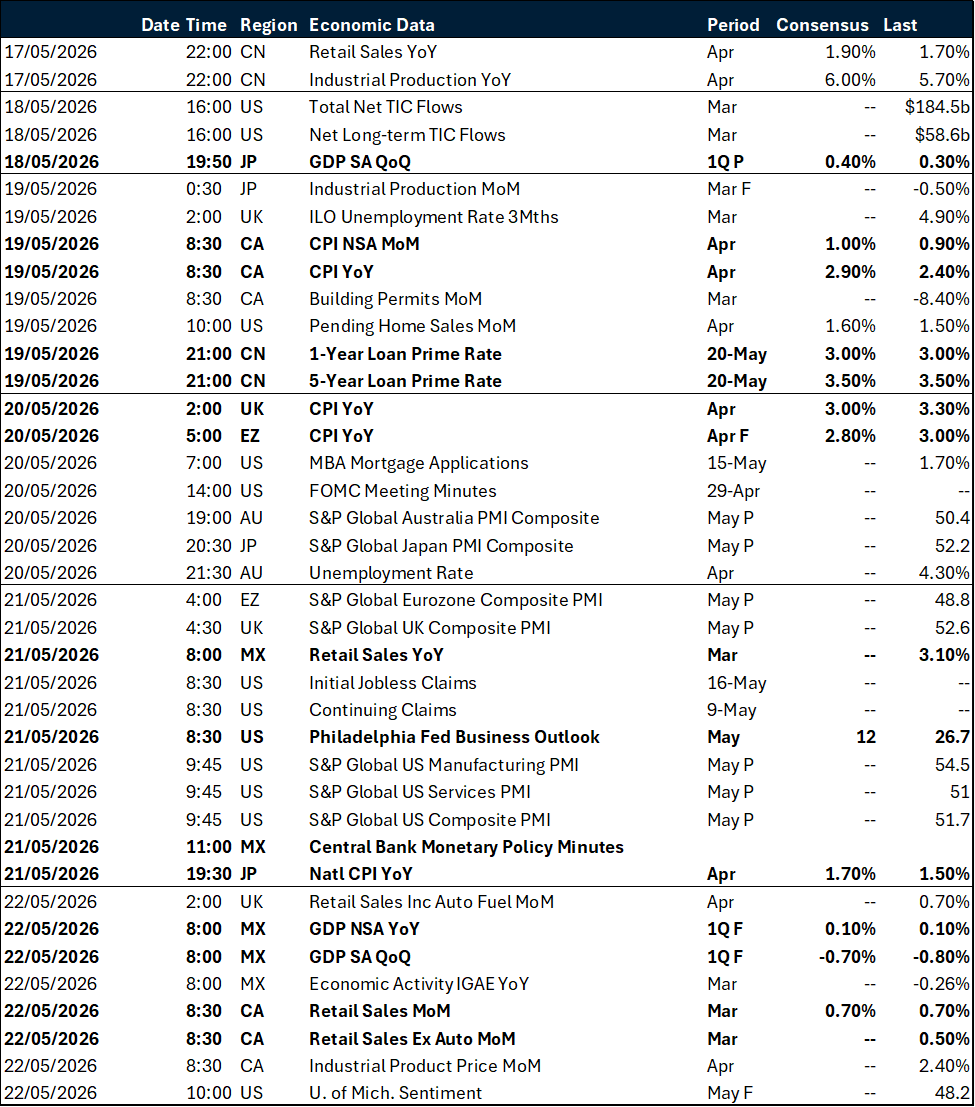

Key global risk events

Calendar: May 18 – 22

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.