USD: Pessim-ISM reins

US equities snapped a five‑day winning streak to start the week, with risk sentiment dented by signals from the Bank of Japan (BoJ) that it may raise rates. The prospect of BoJ tightening rippled through global markets, forcing investors to reassess Japan‑funded carry trades. Bonds underperformed, yields rose, and defensive flows were evident across assets: gold and silver extended rallies, crypto remained volatile, and the USD drifted lower after a lacklustre US PMI print.

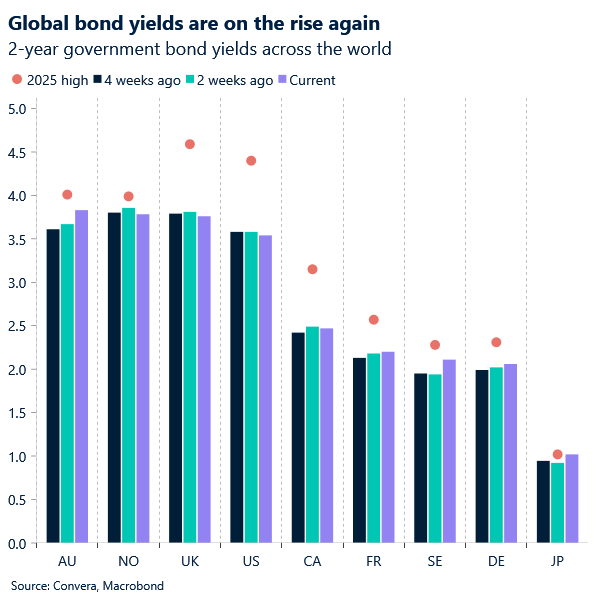

Dollar weakness has been most pronounced against the yen, underscoring how BoJ policy expectations are reshaping FX flows. Political noise around the Fed chair succession added further uncertainty, with odds of Kevin Hassett’s appointment jumping to 73% from 36% last week. Markets see Hassett as more dovish and aligned with Trump’s preference for cuts, raising concerns about Fed independence and credibility. Soaring Japanese yields likely blunted what would otherwise have been a sharper Treasury rally on dovish recalibration.

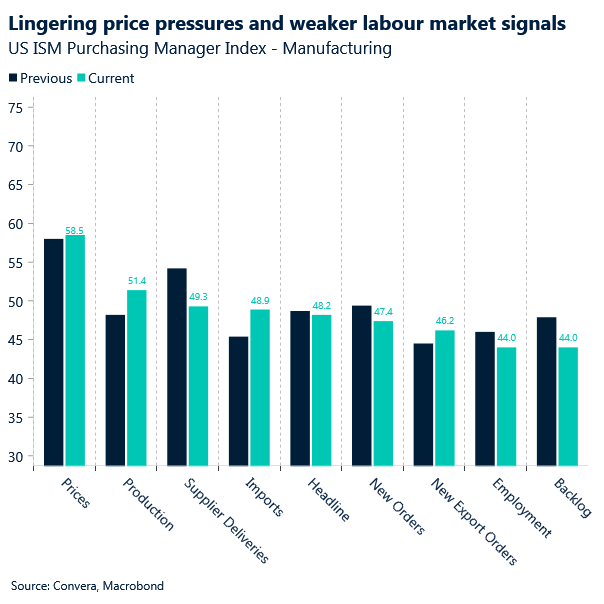

Macro data reinforced the cautious tone. The US ISM Manufacturing PMI fell to a 4-month low in November and the ninth consecutive month of contraction – with employment sliding to 44.0 and input prices rising. The mix of labour softness and sticky inflation complicates the Fed’s policy calculus. Meanwhile, with the next official US jobs report delayed until after the December meeting, private labour surveys and PCE inflation data this week will carry outsized weight in shaping expectations.

Markets continue to price around 60bps of Fed easing by June 2026, but the trajectory could shift if upcoming data leans soft and Hassett is confirmed as chair. A dovish Fed outlook would stand in sharper contrast to peers, especially if the BoJ tightens later this month, adding further pressure on the dollar. For now, investors are hedging against policy uncertainty and bracing for the final stretch of US data before the Fed’s December meeting.

CAD: ‘Drill, Baby, Drill’?

Is this Canada’s “Drill, Baby, Drill” moment? The recent announcement outlines a historic energy agreement between the Alberta and Canadian governments, aiming to transform Canada into a “world energy superpower” by leveraging not just oil and gas, but also renewables and critical minerals. The deal promises to expand export capacity via a new Indigenous co-owned bitumen pipeline, with the potential to add 1.4 million barrels-per-day to the west coast. Yet, this ambitious vision is immediately met with skepticism; critics label the framework “smoke and mirrors,” warning that the requirement for private finance is unfeasible given that the Trans Mountain expansion alone cost $34 billion. This lack of a private proponent has led BC Energy Minister Adrian Dix to state there is currently “no conversation about the feasibility” of the project, while Alberta’s Premier Smith simultaneously faces growing political pressure from opposition leader Naheed Nenshi ahead of the MOU’s aggressive April 1, 2026 deadline for key deliverables.

Crucially, the federal government has agreed to not implement the oil and gas production cap and to immediately suspend the federal Clean Electricity Regulations (CER) in Alberta. Instead, the focus is on reducing emissions intensity through the TIER system and the world’s largest Carbon Capture, Utilization, and Storage (CCUS) project. This regulatory carve-out is set to enable massive investment in AI data centres and strengthened inter-provincial electricity transmission, a package meant to balance economic prosperity with net-zero goals. Furthermore, the MOU attempts to win over key opponents by committing to “appropriate adjustments” to the Oil Tanker Moratorium Act and promising British Columbia “substantial economic and financial benefits” in an explicit effort to secure the necessary trilateral sign-off from B.C. and affected First Nations.

The most damning critique, however, lies in the political and financial cost borne by the federal government. Prime Minister Carney’s move has been met with extraordinary internal dissent, including the resignations of high-profile Liberal loyalists and former ministers, such as Steven Guilbeault. This internal turmoil, coupled with former environment ministers Catherine McKenna and Seamus O’Regan publicly speaking out against the MOU, underscores the political risk.

The most contentious aspect, however, lies in the financial reality hidden within the Memorandum of Understanding. As Mark Carney noted, tightening the TIER system to at least $130 per tonne represents a 600% increase in the effective industrial carbon price for Alberta, a cost critics argue is a staggering self-inflicted wound. This raises a fundamental question of competitiveness: among the top five global oil producers, including the U.S., Saudi Arabia, Russia, and China, Canada is the only one tying incremental pipeline capacity to such expensive and anti-competitive carbon capture mandates. With the “Pathways project” and the use of Canadian steel listed as strict prerequisites, many are left asking why Alberta would agree to a deal that arguably handicaps its own industry while competitors operate without such constraints.

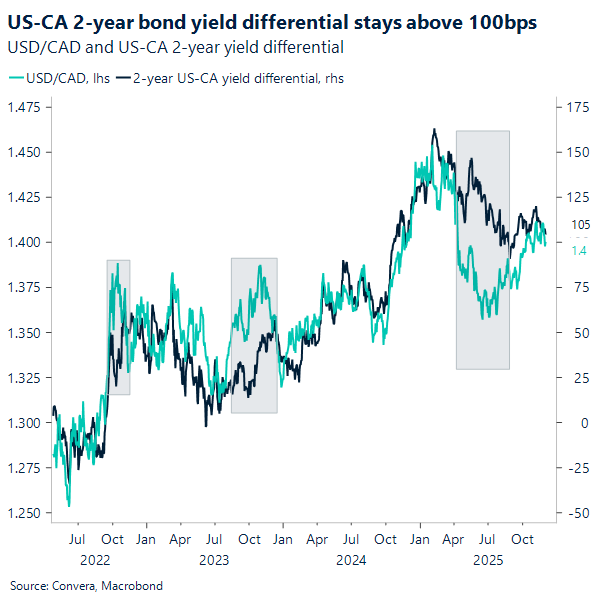

In FX markets, the massive upside surprise in Q3 GDP last Friday pushed the Canadian dollar beyond the key $1.40 resistance level against the USD, signaling reduced near-term economic anxiety. However, the CAD has struggled to remain below 1.377 for long, with the $1.40 level acting as a short-term magnet. Yield differentials continue to point toward $1.40 as the fundamental anchor in the near term.

EUR: Euro buoyed by stability premium

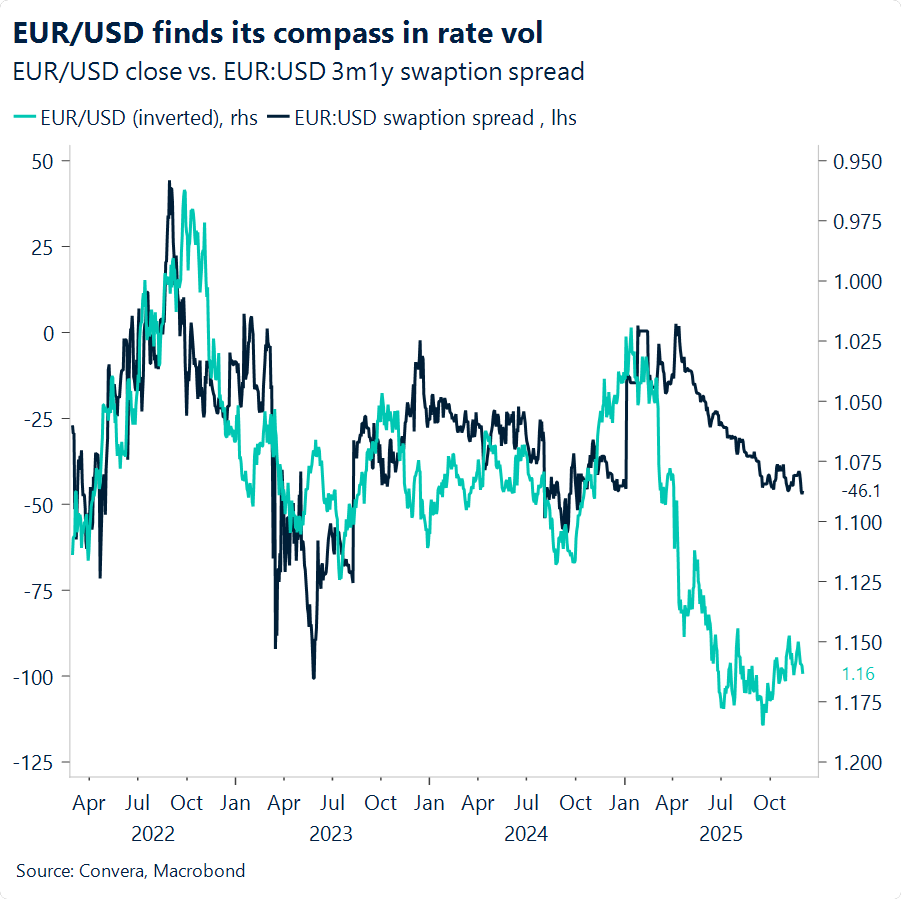

EUR/USD climbed to a two‑week high yesterday at 1.1652, challenging its post-summer downtrend. It met resistance at 1.1650 before closing below the 50‑day moving average near 1.1620, dampening hopes of a more sustained advance and leaving the pair confined within its bearish structure, with the 50‑day MA acting as key resistance since mid‑October.

The euro was broadly bid, with ECB policy stability appearing attractive at a time when the policy outlook for majors such as USD and GBP remains in flux. The single currency weakened only against the yen, after BoJ Governor Ueda signaled that the bank will hike rates later this month. As global bonds sold off, euro‑area debt may have benefited from spillover demand, given the relative stability of the ECB’s policy path.

Additional momentum in EUR/USD came from weaker‑than‑expected US factory activity (ISM manufacturing headline PMI). Markets also absorbed the nomination of a likely dove as the next Fed chair. Given that recent dovish repricing had not moved the dollar significantly, the softer ISM print, combined with confirmation of a dovish‑leaning Fed president, helped solidify expectations for next week’s easing and beyond, pushing the dollar lower.

Eurozone CPI is due today. While it is expected to print in an orderly fashion, slightly above target at 2.1%, any undershoot would lend more directional weight to last week’s mixed single‑country releases. That said, unless there is a major sub‑2% miss, euro price action is unlikely to react meaningfully. Oh, and keep an eye on the bloc’s unemployment rate too!

Gold is up 4% the last week

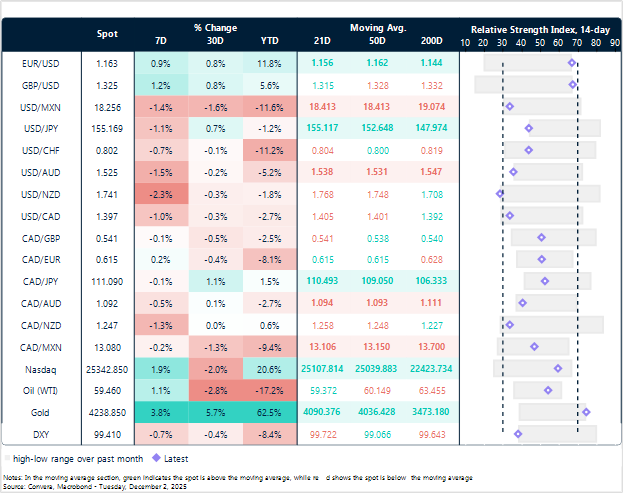

Table: Currency trends, trading ranges and technical indicators

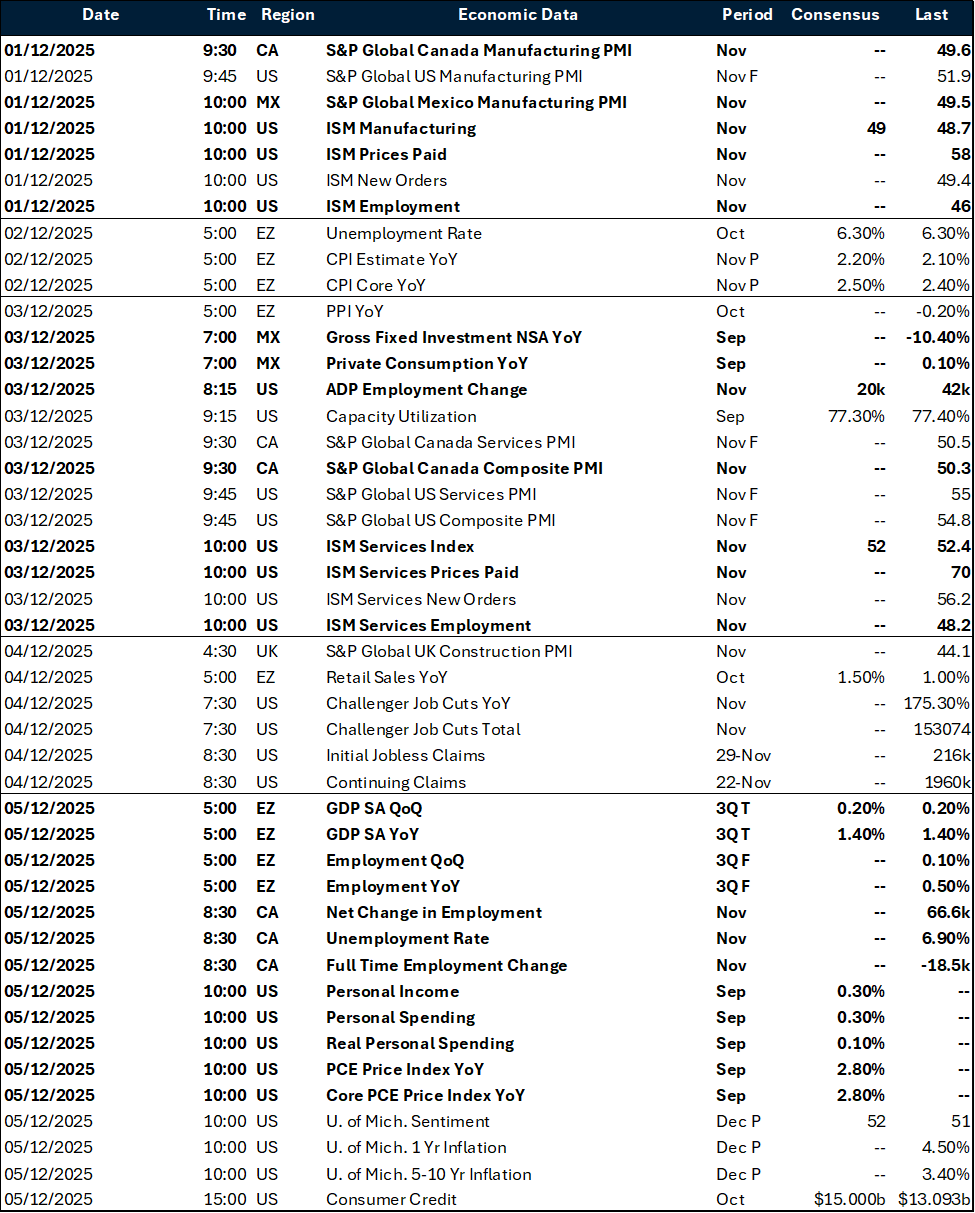

Key global risk events

Calendar: December 01 – 05

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.