USD: Geopolitics back in the driver’s seat

The US dollar found renewed fuel after a series of over‑the‑weekend threats between Iran and the US added pressure to oil prices and kept markets on edge. President Trump issued a 48‑hour ultimatum to “re‑open” the Strait of Hormuz, expiring at 7:44 p.m. Eastern on Monday, after which he has threatened to strike Iran’s power plants. Iran countered by threatening to hit power and water infrastructure across the region.

The headlines pushed geopolitical tensions back to the forefront, overshadowing the dampened hawkish support for the dollar last week. Powell’s mildly hawkish tone on Wednesday was quickly eclipsed by reports that the ECB is actively considering an April hike and by the BoE’s most dovish member openly entertaining tightening. The result was a broad USD pullback that extended well beyond what US rate dynamics alone would justify.

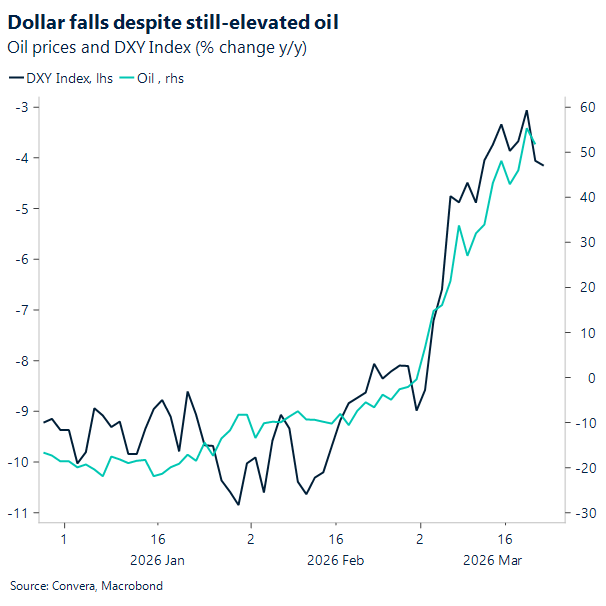

Oil remained the dominant driver too though. The correction lower, triggered by Israeli claims that progress is being made on reopening the Strait of Hormuz and by Washington’s clear discomfort with recent Israeli strikes on Iranian gas assets, dragged the dollar lower and supported energy-sensitive FX. The dollar’s over 1% decline last week reflects a market willing to price a degree of optimism into the geopolitical backdrop — even if the underlying fundamentals remain fragile.

Still, the latest central bank decisions reinforced a familiar message: nothing yet is strong enough to dislodge oil as the primary market anchor. Rate expectations across the G10 remain fluid and highly commodity‑dependent, leaving FX to trade more on shifts in energy sentiment than on policy guidance. That dynamic explains why the dollar weakened despite Powell’s steady hand — the surprise came from abroad, not from the Fed.

The next few days will determine whether this cautious optimism has staying power. Clear evidence of progress on Hormuz would allow the USD to extend its decline, but absent that, the dollar remains prone to sharp rebounds as energy volatility persists.

This week’s global PMIs will offer an early read on how businesses are absorbing the latest shocks. Momentum had improved into late 2025, but renewed trade uncertainty and the Middle East conflict now threaten to soften demand and lift input costs. For the dollar, that mix keeps the near‑term path two‑way — but still tightly tethered to the energy narrative.

GBP: Sterling’s fragile backstop exposed

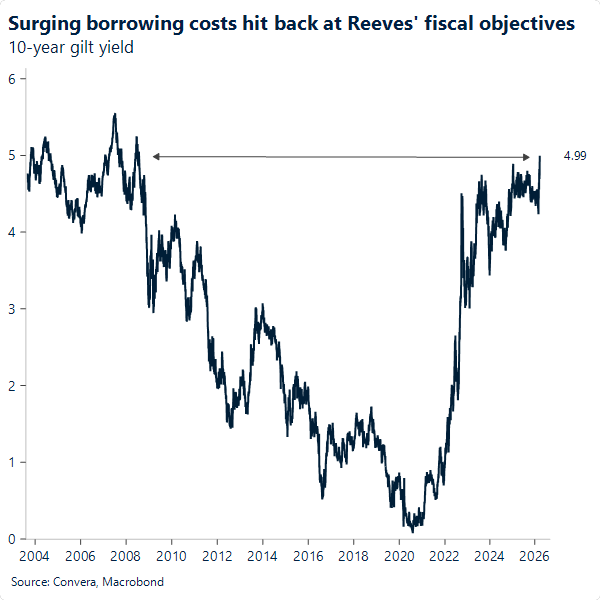

Sterling came under pressure on Friday as UK government borrowing costs rose to their highest level since 2008, with the 10-year yield briefly touching the 5% mark. The selloff unveils the fragile nature of sterling’s only lifeline of support: a more hawkish BoE since the conflict began. There are two considerations to be made here.

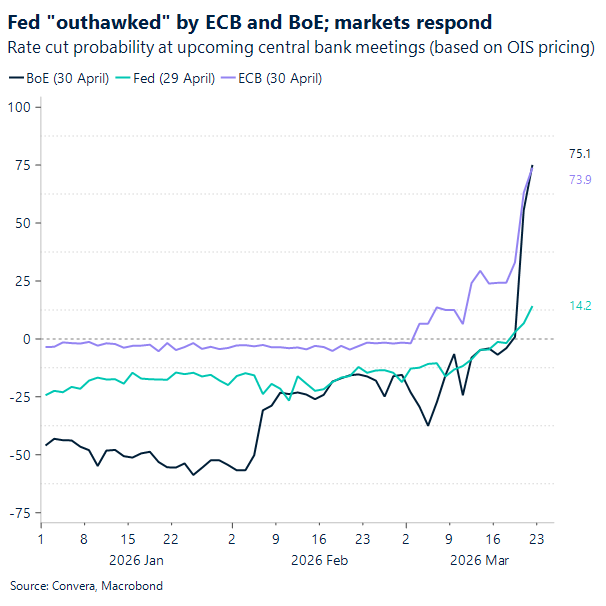

Last week, amid a parade of central bank policy meetings, the BoE stood out as the most hawkish of the bunch, leading a global bond selloff as policymakers delivered firmer signals in response to the conflict‑driven repricing of inflation expectations. Markets now price in more than three quarter‑point hikes by year‑end. The move looks exaggerated. With a softening labour market and sluggish economic momentum – both likely to deteriorate further because of the conflict – the BoE is hardly in a position to abandon its easing bias. That raises doubts about how realistic the current market read actually is.

The conflict also puts the spotlight back on the government’s self‑imposed fiscal rules. Friday’s surge in the 10-year yield highlighted the pressure that the conflict is placing on the government’s interest‑rate repayment burden. This adds strain on Keir Starmer’s administration, which has already faced significant backlash. Weak political leadership, combined with a fiscal risk premium that has been dormant since the 2025 Budget but may now be reawakening, is likely to exert meaningful bearish pressure on sterling in the months ahead as we approach May’s local elections.

On the data front, this week’s UK inflation will be in focus, though markets may treat the print cautiously. The release covers February, while the conflict erupted on 28 February. It will still offer insight into the BoE’s expected disinflation path before the shock hit, but the data already feels outdated given how dramatically the conflict has repriced inflation risks – and, with them, the BoE’s short‑ to medium‑term policy outlook.

EUR: ECB hawks re-claim the narrative

The euro began the week showing more selective bearishness, particularly against oil‑exporters such as the USD and CAD, as markets continued to digest last week’s hawkish signals from the ECB. With the Bank having effectively concluded its easing cycle, any tightening responsiveness is now perceived as more imminent compared with the Fed or the BoE, both of which had been in easing mode and therefore had no hikes on their near‑term radar. The result is more ready‑made support for the euro, best evidenced against currencies that are not materially supported by surging oil prices.

A raft of ECB policymakers has reinforced Lagarde’s hawkish messaging. Germany’s Joachim Nagel and Gabriel Makhlouf suggested the Bank may need to consider hiking as soon as the April 30 meeting if price pressures build further. The latest was ECB Vice President Luis de Guindos, who said the ECB is “ready to respond as necessary,” noting that the conflict poses risks to both the inflation and growth outlook.

More ECB speakers are lined up this week, starting with Philip Lane and Piero Cipollone later today, likely to reinforce the hawkish contour that should support the euro in the short term. On the data front, eurozone preliminary PMIs for March are released tomorrow. The indicators had begun to show more upbeat momentum toward the end of 2025 and into early 2026, but the new year brought a series of sentiment‑dampening shocks that now cast doubt on the durability of that improvement. From renewed trade uncertainty following the Supreme Court’s ruling that Trump’s tariffs were illegal, to the outbreak of conflict in the Middle East, businesses may be heading into months of softer demand and higher energy costs.

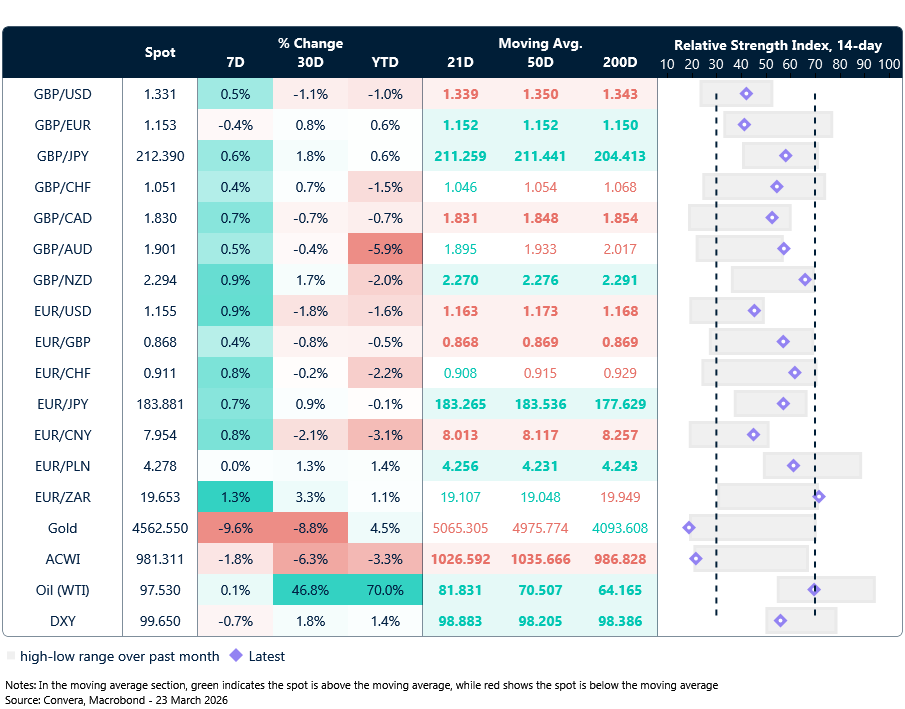

Market snapshot

Table: Currency trends, trading ranges & technical indicators

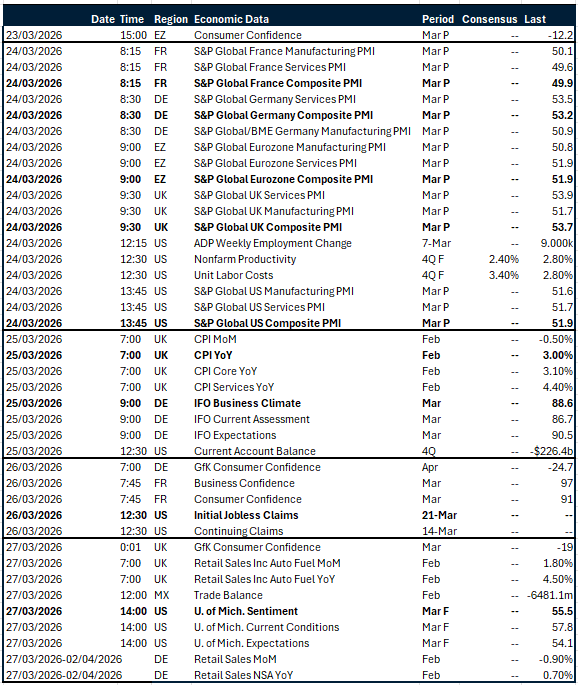

Key global risk events

Calendar: March 23-27

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.