GBP: High-stakes Budget is here

UK Chancellor Rachel Reeves will unveil her autumn Budget today, with a “smorgasbord” of tax hikes aimed at plugging a £30bn hole in the public finances. But the real drama may only begin once she sits down, as gilt markets and the pound brace for reaction. Raise taxes too aggressively and investment risks stalling; fail to close the fiscal gap and the spectre of 2022’s bond market turmoil and a plunging pound looms large.

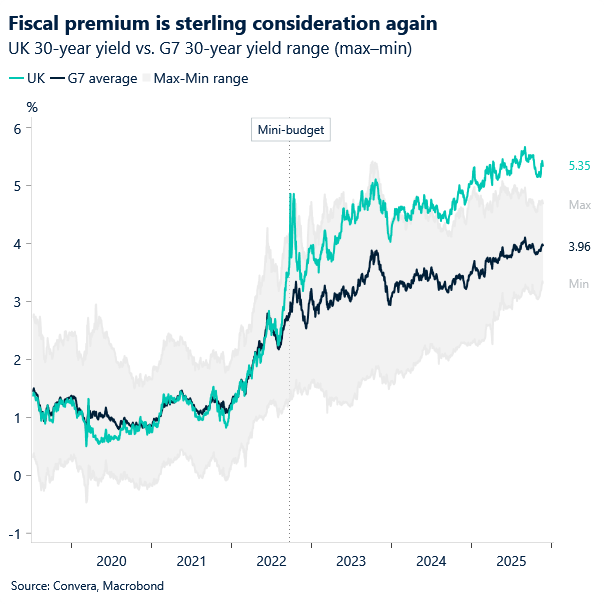

Yields tell the story of unease. The 10‑year gilt yield has eased in recent months but still sits at 4.5% — the highest in the G7 — while the 30‑year still hovers near levels last seen in 1998. Borrowing costs are climbing across advanced economies amid sticky inflation and weaker growth, but the UK’s fiscal position is drawing particular scrutiny, with debt close to 100% of GDP. Earlier this month, investors recoiled after reports Reeves had abandoned plans for a manifesto‑busting income tax rise, underscoring the fragile confidence she must now restore.

Now, it seems, Reeves is opting for a patchwork of smaller, more intricate measures: freezing thresholds, levying high‑end property, and introducing niche charges like the tourist tax. But the risk is that markets view it as piecemeal tinkering. Complex, fragmented hikes can be harder to model, harder to sell politically, and may not deliver the clarity investors crave.

That’s why gilt traders are so focused on the aftermath — if the package looks like a muddle, the fiscal risk premium could persist, keeping yields elevated and sterling fragile. Conversely, if Reeves can frame these smaller measures as part of a coherent, credible path, she might just buy herself breathing space.

Why did the pound strengthen yesterday? Sterling’s resilience was less about conviction and more about positioning. Investors have been running heavy GBP shorts over the last few months, reflecting the sizeable risk premium embedded in the currency. With the Budget looming as a potential inflection point, traders are reluctant to be caught flat‑footed by any upside surprise. Thus, though there are plenty of pitfalls ahead, with so much negativity baked into sterling’s price of late, the risk is not only of a stumble, but also of a relief rally if Reeves can convince markets that fiscal credibility is intact.

Purely from a technical lens, GBP/USD jumped and closed back above its 21-day moving average for the first time in over a month. That break signals a shift in short‑term momentum, but whether it sticks depends on Reeves’ fiscal credibility. Buckle up.

EUR: EUR/USD eyes 1.1650 break

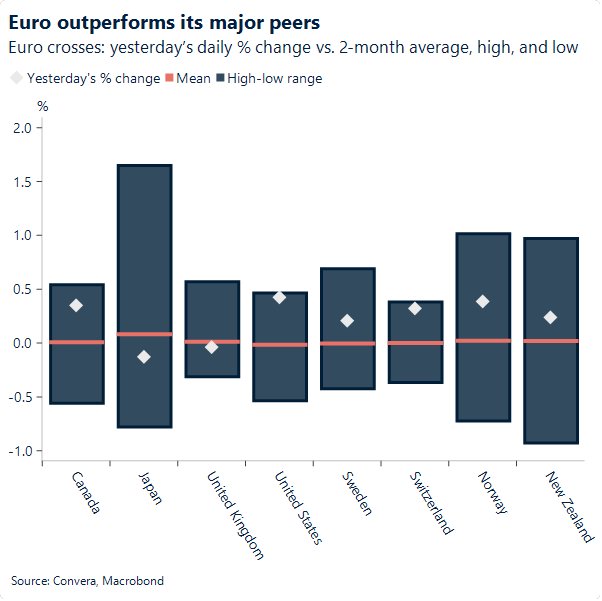

The euro strengthened 0.4% against the dollar yesterday, outperforming across the G10 space. The currency was supported both by weak US macro data and continued developments around a potential Ukraine–Russia ceasefire.

Following pressure from Ukraine’s European allies, the US has revisited its original peace plan, reworking it with Ukrainian officials during Geneva talks. Initially rejected by President Zelenskyy, the plan had included concessions that seemed heavily geared towards Moscow’s longstanding demands. Russia has yet to accept the revised changes, however, raising doubts over Moscow’s readiness for a ceasefire, particularly as both sides have continued to exchange fire despite ongoing peace efforts. Trump’s envoy Steve Witkoff is heading to Moscow next week to meet President Putin in hopes of finalising a plan, while President Zelenskyy has signaled readiness to meet Trump to discuss outstanding “sensitive points.”

EUR/USD pulled back from seemingly overstretched lows near 1.15 and is poised to test 1.16, with 1.1650 emerging as a more concrete resistance level. That threshold has capped the pair’s range-bound trading since mid-October, but the euro now appears better positioned to challenge it. The release of US macro data – delayed by the shutdown – could provide the catalyst for a breakout and re-engage the pair in a more pronounced bullish move.

CAD: Cost efficiencies mask tariff pain in Q3 profits

According to Statistics Canada, the strong corporate operating profit of $200.0 billion in the third quarter of 2025, despite the ongoing tariff war with the US, is largely a story of sector divergence rather than broad-based economic invincibility. The headline growth is heavily skewed by the financial sector, which posted a $5.4 billion increase. This sector is naturally more “sheltered” from direct border tariffs on physical goods compared to industrial sectors. Banks and insurers benefited significantly from lower provisions for credit losses and strong investment returns, effectively masking the deeper cracks forming in trade-exposed parts of the economy.

Trade-sensitive sectors are bearing the brunt of the impact, while others are insulated or even benefiting from unique dynamics. The construction and transportation industries, both highly sensitive to supply chains and cross-border flow, saw profits decline by 4.4% and 5.9% respectively, directly citing “tariff pressures” and rising input costs. Conversely, the mining and oil and gas sectors were buoyed by global commodity prices (like record gold and crude oil production), which often operate independently of bilateral trade disputes. Interestingly, the tourism sector actually benefited from the trade tension; record domestic travel suggests Canadians chose to vacation within provinces rather than cross the border, redirecting spending back into the local economy.

Cost-cutting is a significant factor of increased operating profits, particularly in manufacturing. While manufacturing profits rose, Statistics Canada notes this wasn’t necessarily due to booming demand across the board, but partly due to “cost efficiencies.” For example, the auto industry saw a profit jump driven by “lower operating expenses,” which were the result of workforce adjustments and temporary production shutdowns to manage inventory of electric vehicles. This indicates that for some industries, “growth” on the balance sheet is currently coming from tightening belts and managing output rather than purely selling more goods to the US.

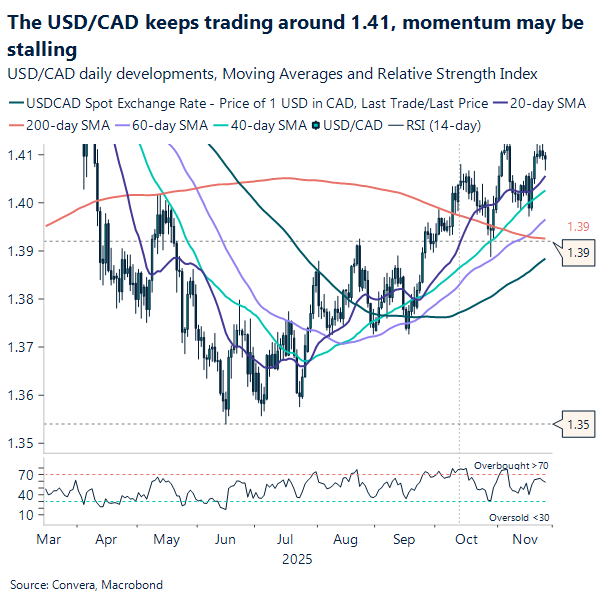

In FX, the USD/CAD keeps lingering around $1.41. Although the equity “fear index” has shown improvement in the US equity market, dropping from 27 to 18.6, underlying uncertainty persists. The US Dollar has given up some of its weekly gains, but the Canadian Dollar is still near the ceiling of its half-year trading range ahead of the key Q3 GDP print this Friday.

GBP takes a breather ahead of Budget

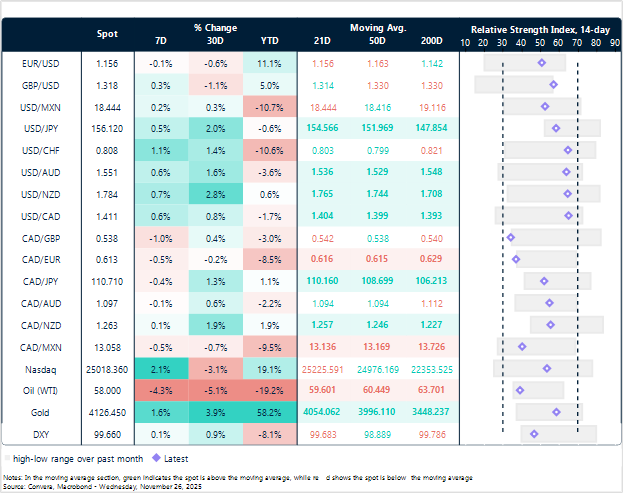

Table: Currency trends, trading ranges and technical indicators

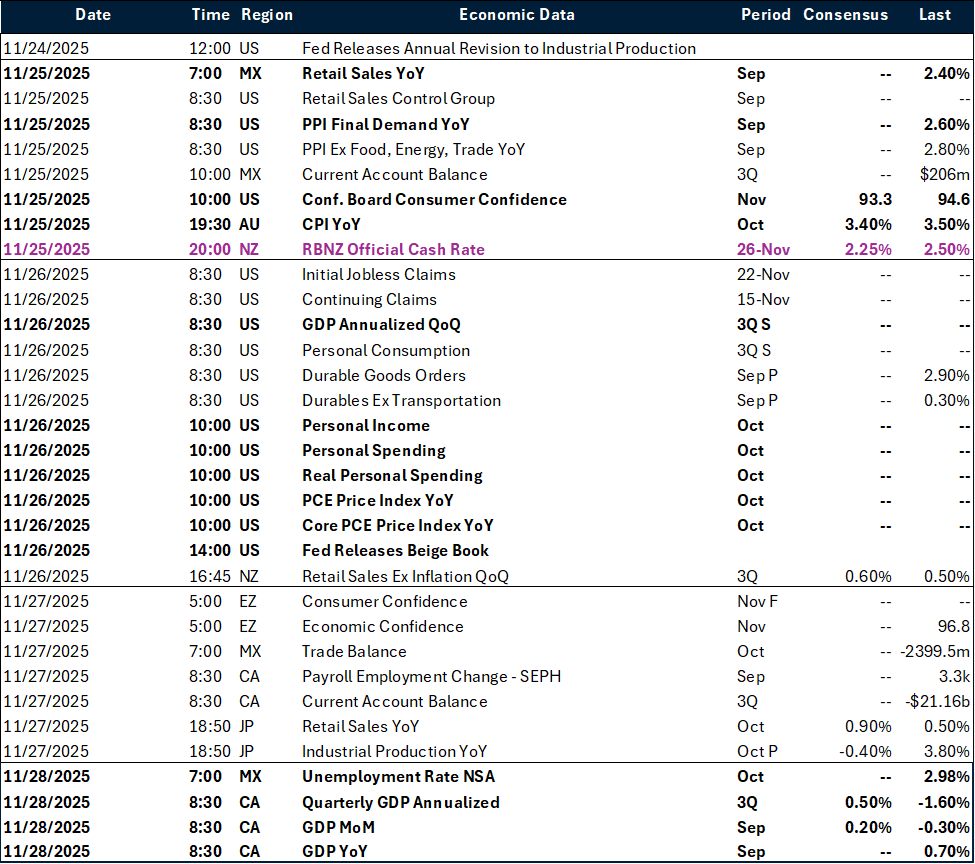

Key global risk events

Calendar: November 24-28

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.