USD: Dollar bears grapple with growth expectations

Yesterday’s data dump provides a snapshot of an economy that refuses to cool, even if the figures are technically “stale,” reflecting the activity of late 2025.The standout figures from the November reports, retail sales climbing 0.6% (beating the 0.5% survey) and a massive 28.5% jump in MBA mortgage applications, signal a consumer base that remains undeterred by previous tightening cycles. This resilience is directly feeding into the Atlanta Fed’s GDP Nowcast model, which currently estimates Q4 2025 growth at a robust 5.1%. Despite the reporting lags typical of a post-shutdown environment, the underlying domestic demand suggests the “hard landing” narrative is increasingly a fringe view as we move deeper into January.

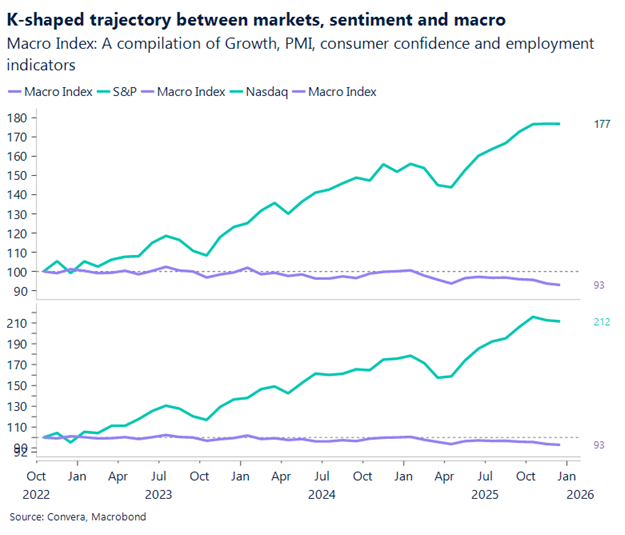

The puzzle of a “hot” GDP alongside a seemingly stalled labor market is reconciled by recent Dallas Fed analysis, which reveals a profound structural shift: the US labor market now needs to add barely 30,000 jobs a month to stay in balance. This “breakeven” collapse, down from 250,000 in 2023, explains how the economy can print supercharged growth while hiring feels stagnant. It also masks a stark K-shaped divergence; while higher-income tiers benefit from surging productivity and asset prices, the “stalled” headline labor numbers reflect a cooling for the lower-income cohort. This environment allows the administration to pursue a “run the economy hot” policy shift, prioritizing growth at the cost of potential long-term stability.

This policy tilt is already rippling through the commodities market, where a renewed bid for industrial metals and energy could be seen as a hedge against a possible inflationary spiral in 2026. With PPI final demand at 3.0% y/y (surpassing expectations), the market is no longer debating if inflation has bottomed, but rather how high the new “floor” will be. (i.e. where’s the neutral rate going to be). Investors are assessing and wondering if this heat will be a sustainable productivity boom or if the mounting fiscal pressures, will eventually trigger a debt-driven crisis. The fear is that the “run hot” strategy is simply borrowing growth from a 2026 that may be defined by persistent price volatility, especially in commodities markets.

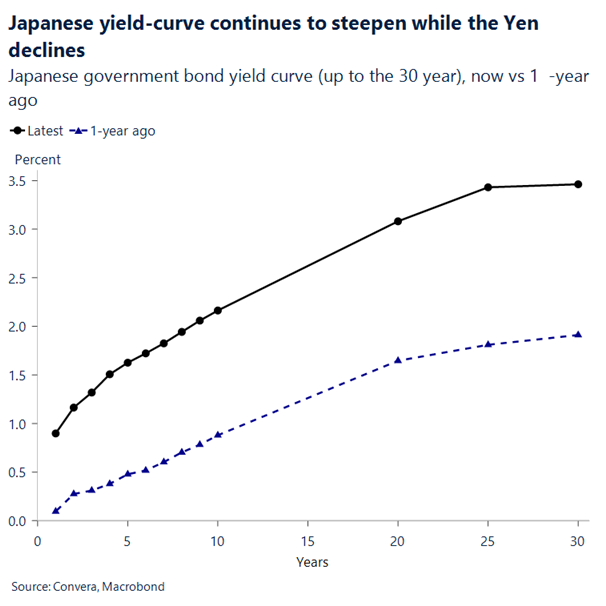

The global backdrop adds a layer of complexity, particularly the “historically unusual” situation in Japan. Prime Minister Sanae Takaichi intensified the pressure yesterday by signaling a snap election for February to secure a mandate for her expansionary fiscal agenda. This political gamble has pushed 10-year JGB yields above 2.1% (levels not seen since 1999), yet the Japanese Yen continues to slide toward the 160 level against the dollar. This rare combination of rising yields and a weakening currency is a worrisome signal for a G-7 economy. It serves as a stark warning of what happens when fiscal credibility is questioned on the world stage.

Looking ahead, the USD outlook for 2026 appears increasingly complex, leaving dollar bears facing a choppy year. While the greenback might find significant relief in Q1 if the post-shutdown US economic revival is confirmed, the sustainability of this strength requires more than just “hot” numbers, it needs data validation that growth can coexist with manageable yields. Without it, the dollar remains at the mercy of evolving Fed expectations and the market’s tolerance for fiscal expansion. Ultimately, 2026 will be a test of whether the USD retains its “safe haven” status or begins to trade like a high-beta growth currency sensitive to the very heat the administration is trying to generate.

EUR: Volatility too quiet for comfort

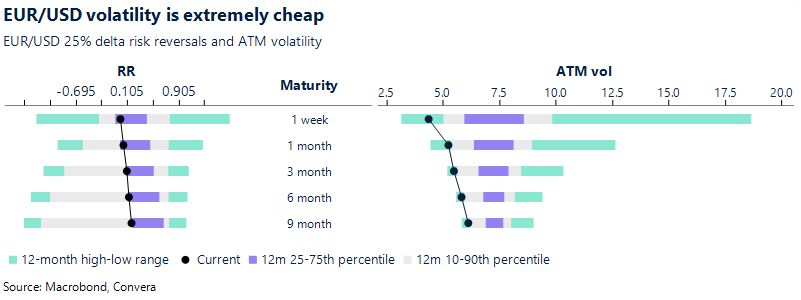

Expected volatility in EUR/USD has slipped to unusually subdued levels, with one‑month volatility below 5.3% and six‑month vol under 6%, offering very little compensation for either time or uncertainty.

What makes this so striking is the backdrop: major geopolitical flashpoints — from US political escalation and rising Iran–Israel tensions to the unresolved war in Ukraine — are barely reflected in FX pricing. We’ve seen some modest haven demand for the Swiss franc, but it’s not significant. True, spot prices rarely embed these types of geopolitical risks directly, but the options market normally does; right now, it isn’t. The result is a potential mispricing: volatility looks cheap not because the world is calm, but because positioning and flows have dampened demand for protection. That’s rarely sustainable, and any unwind could trigger abrupt volatility spikes.

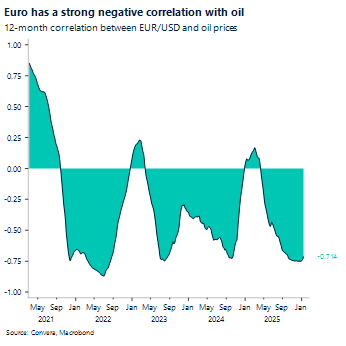

In the near term, stretched long EUR positioning and the disappearance of ECB‑hike expectations leave the common currency with a slightly bearish bias. Moreover, rising oil prices don’t bode well for it either. Unless Fed‑independence risks intensify and the “Sell America” narrative gains real traction, a dip below $1.16 cannot be ruled out.

Looking further ahead, Europe is hardly insulated from risk. Germany and France are both navigating political fragility, and China’s record $1.2 trillion trade surplus is a headwind for Eurozone inflation and growth. The combined drag on activity and prices tilts risks toward a more dovish ECB and, by extension, downside for the euro.

Even so, we expect the dollar to face greater downside pressure from Q2 onward as US‑specific risks build and Eurozone growth improves on the back of fiscal support. That opens the door for EUR/USD to retest — and potentially break — above $1.20 later in the year.

In the meantime, we expect EUR/USD to remain trapped in its familiar $1.15–$1.18 range — unless, of course, we see the volatility pickup flagged at the outset, which could break the pair out of its holding pattern.

GBP: Gilts lean into the soft patch

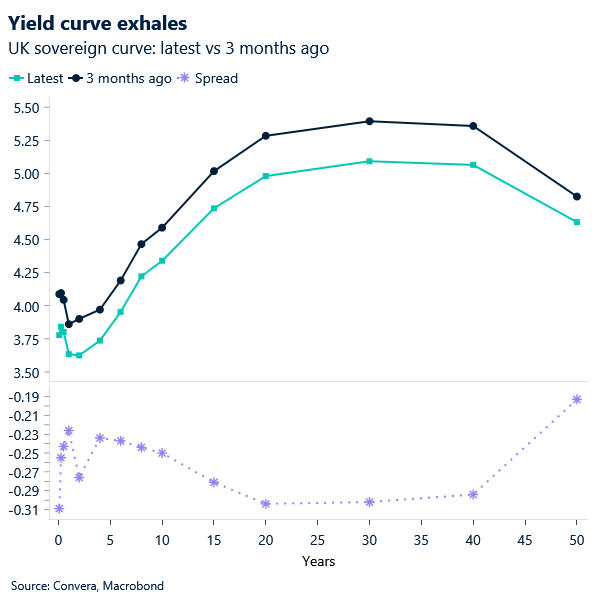

Yesterday the UK’s benchmark bonds rallied, sending borrowing costs to their lowest level since December 2024. The yield on 10‑year gilts fell six basis points to 4.34%. The slide marks a sharp turnaround from this time last year, when fiscal worries put pressure on the long end of the curve.

While the fiscal backdrop remains fragile, the UK budget has eased, or at least postponed, further market jitters. The result is a clearer read of growing BoE easing through the yield curve, reinforcing the scope for additional cuts.

This morning, monthly GDP figures for November rose 0.3%, rebounding from a 0.1% fall the previous month and beating the 0.1% growth predicted by economists. The ONS said the increase reflected a rebound in production at Jaguar Land Rover, the car manufacturer hit earlier in the autumn by a cyberattack. In fact, half of the rise in GDP was driven by industrial production.

While the print may help allay worries that the economy has deteriorated in recent months after persistent signs of mounting job losses, it is unlikely to materially shape the BoE outlook. The series is notoriously volatile and sits well outside the Bank’s core focus on inflation and labour market dynamics. GBP’s reaction saw the pound pare losses against USD in early trading today, yet we do not expect meaningful upside from here, as the data backdrop’s influence on GBP price action remains dependent on MPC commentary amid broad divisions.

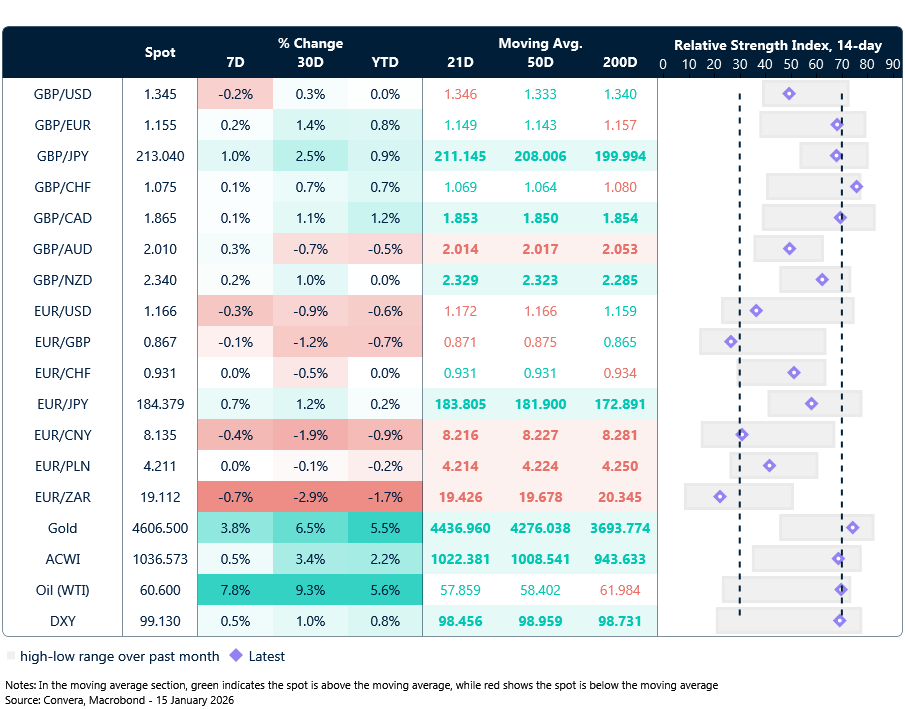

We see GBP/USD trading sideways for the remainder of the week, bounded by tops at 1.3460 and support at 1.3420.

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

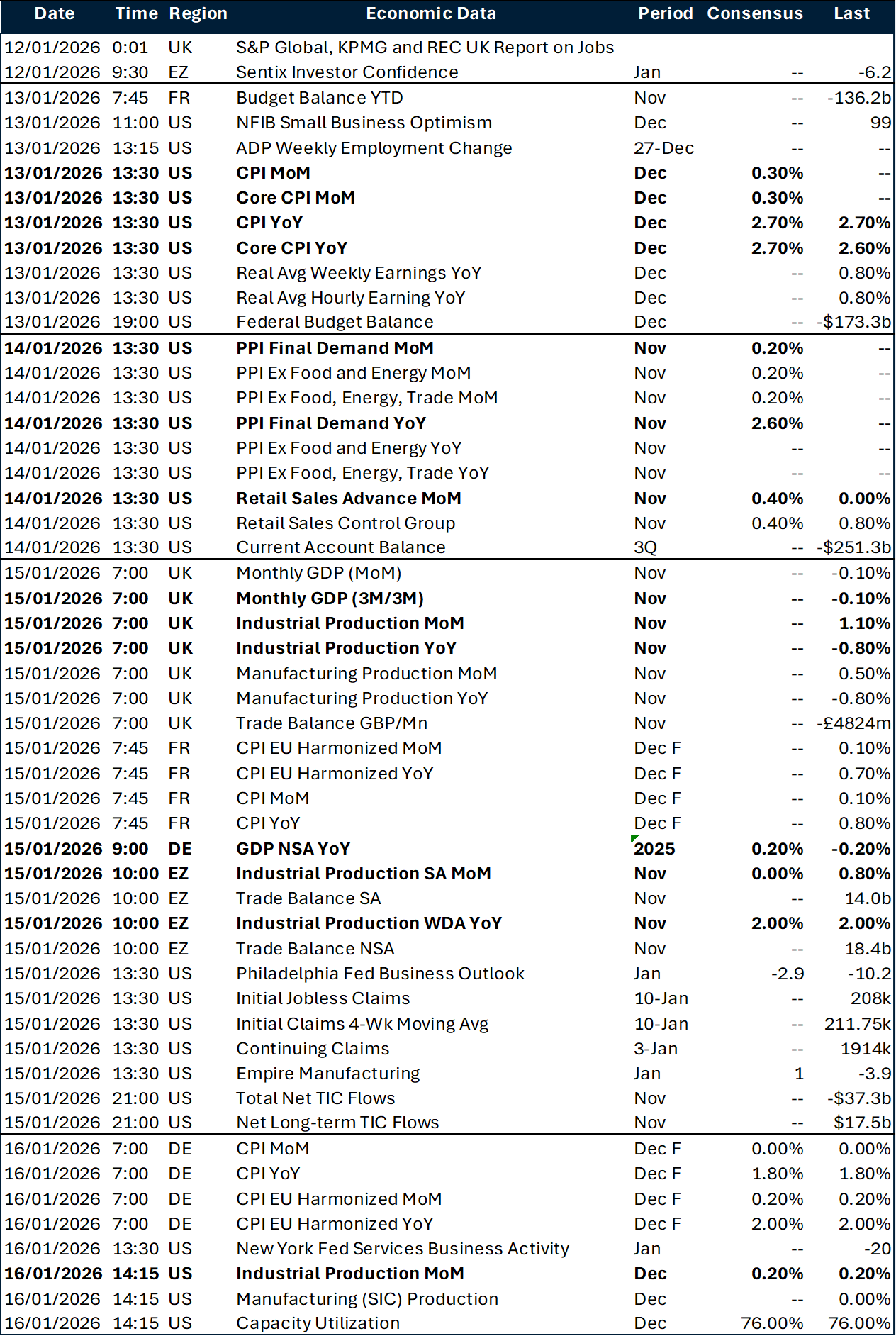

Calendar: January 12-16

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.