USD: Risk on, dollar off

Risk sentiment improved on Monday as markets responded to signs of tentative de-escalation in the Middle East alongside a stabilisation in semiconductor stocks. Iran said its military operation against Israel had concluded following weekend strikes, while President Trump struck a more constructive tone on negotiations with Tehran, easing fears that recent escalation would derail attempts to secure a broader agreement.

The retreat in oil prices and Treasury yields helped support equities, with the Nasdaq 100 rising 1.6% as semiconductor stocks rebounded sharply. The more constructive tone carried into Asia overnight, where South Korea’s Kospi recovered most of its early‑week losses as chipmakers led gains across the region following a 5.6% rally in the US semiconductor sector.

In FX, the dollar started the week softer as improved risk appetite and lower oil prices reduced demand for defensive positioning. Even so, downside pressure on the USD is likely to remain contained given continued support from rates markets and a resilient US macro backdrop. Markets are now pricing close to 30bp of additional Fed tightening this year and around 50bp by Q2 2027.

Geopolitical headlines continue to drive day‑to‑day sentiment swings, though beneath the volatility the dollar continues to draw support from the US rate advantage and relative economic outperformance. Those dynamics should help underpin the broader USD trend beyond the near-term headline noise.

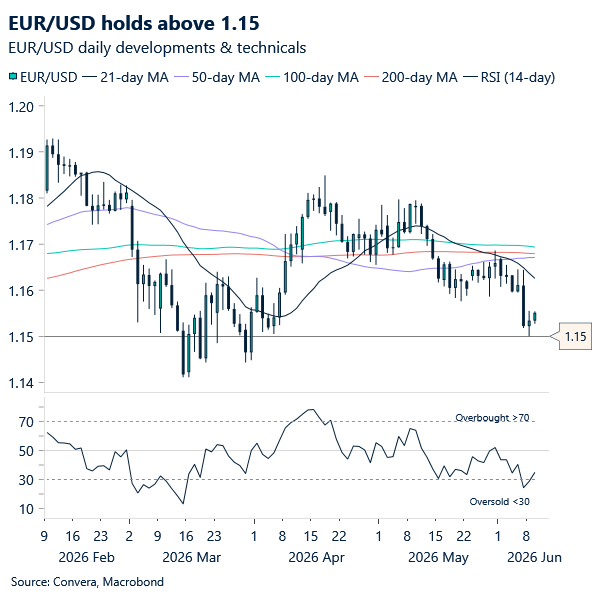

EUR: Tentative rebound

EUR/USD pared part of Friday’s move, rebounding from support at 1.15 after breaking south of 1.16. It has, however, struggled to more convincingly re‑claim 1.1550 despite improved risk appetite following the de‑escalation of Israel–Iran tensions. The price action therefore reinforces the view that Friday’s break below 1.16 was less about geopolitics and more a confirmation of a hawkish re‑pricing of the Fed relative to the ECB, with a blowout US jobs report as the catalyst.

We expect EUR/USD to hold above 1.15 while struggling to break significantly higher from 1.1550 ahead of Thursday’s ECB policy meeting, barring a meaningful re‑acceleration in de‑escalation momentum around Hormuz. On rate-setting day, the focus will be on the ECB’s revised projections. That said, a likely data‑dependent forward guidance, coupled with a growing divergence between upwardly revised inflation and downwardly revised growth expectations, should limit the extent of any directional FX follow‑through in support of the euro.

A test of 1.1450 this week remains on the table should growth forecast revisions prove particularly negative, especially in light of recent underwhelming euro area macro – including Germany’s factory orders on Monday.

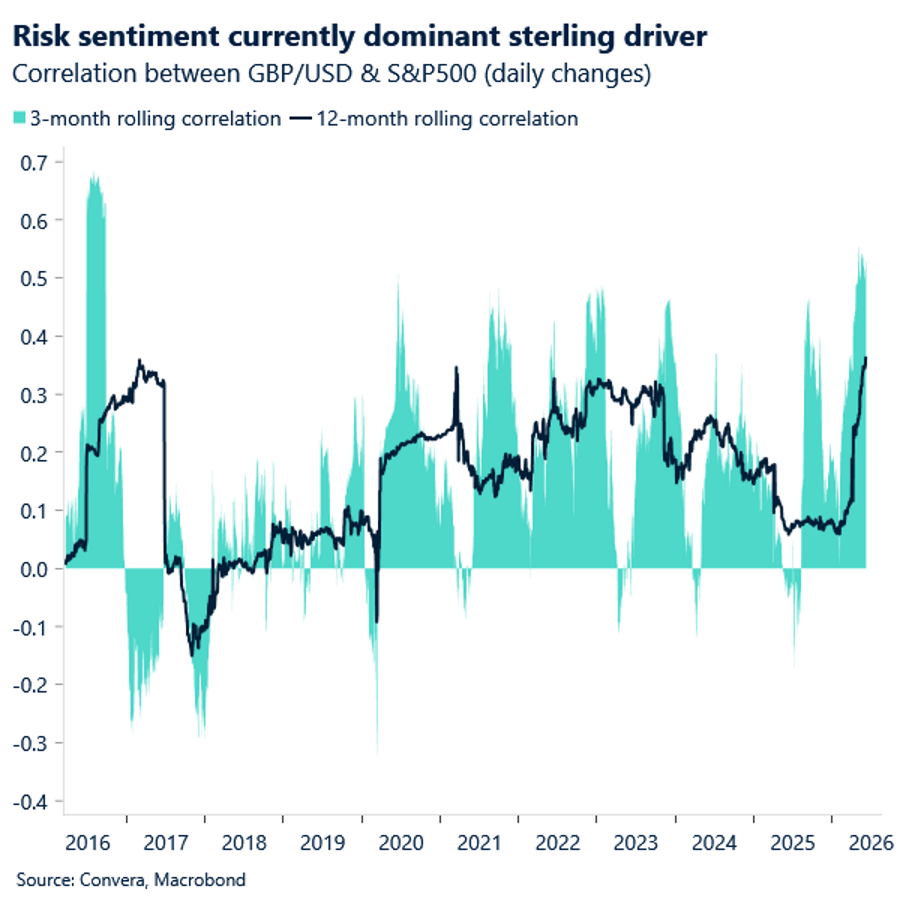

GBP: Pound rebounds with risk appetite

Sterling rebounded from the 1.33 area against the dollar on Monday, with that level again acting as an important pivot that previously defined much of the March-April range. Attention had centred on the risk of a deeper breakdown toward 1.3250 and potentially 1.3160, but Tuesday’s follow‑through move has lifted GBP/USD back toward 1.3370.

Even so, sterling would still need to reclaim the 1.3440-1.3480 resistance zone to meaningfully ease the current bearish bias. For now, the technical backdrop continues to favour the dollar moderately, supported by a relatively stronger US growth outlook and higher US real yields.

The UK story has become less supportive over the past month. Economic data has softened, while domestic political uncertainty is beginning to re-enter the equation. Prediction markets currently assign Andy Burnham an overwhelming probability of winning next week’s Makerfield by-election, while also implying a strong chance of him becoming prime minister before year-end.

Gilt markets have already shown signs of unease around a potential shift toward the softer left of the Labour Party. Given the UK’s elevated debt burden, investors appear wary of any policy direction that could imply materially higher gilt issuance or weaker fiscal discipline.

Still, external forces remain the dominant near‑term driver of the risk‑sensitive pound, with the rebound in global equities helping support sterling broadly at the start of the week.

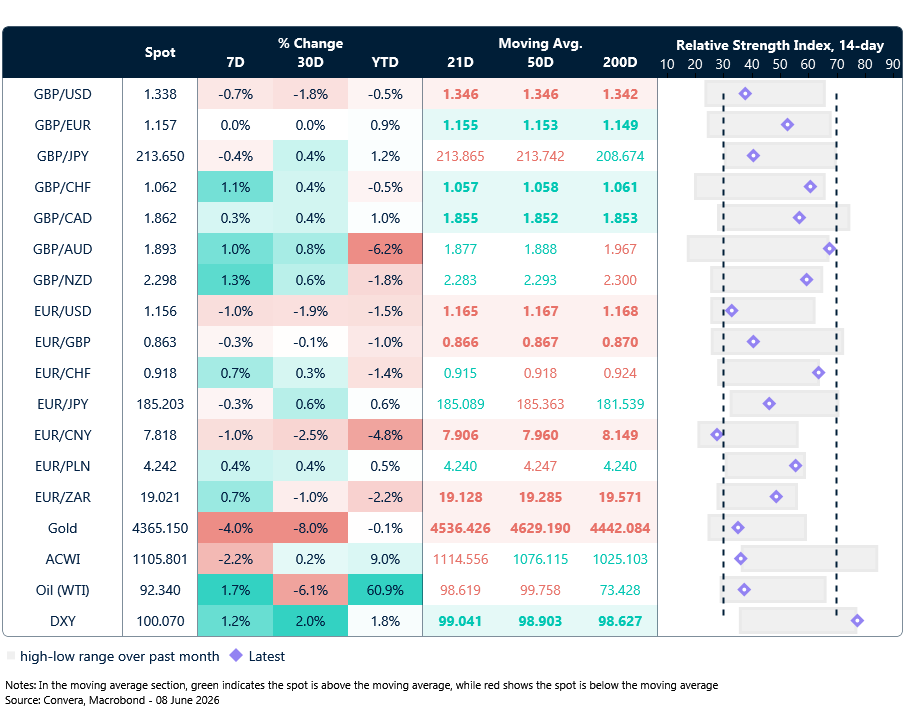

Market snapshot

Table: Currency trends, trading ranges & technical indicators

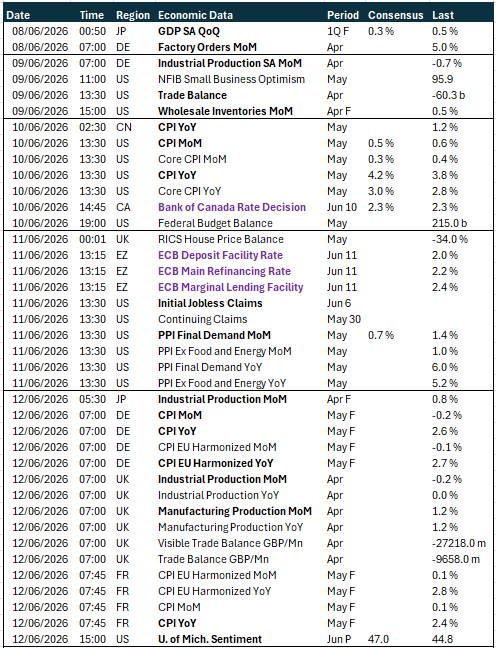

Key global risk events

Calendar: June 8-12

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.