USD: Oil-driven dollar strength fades

Risk appetite has improved after US President Trump signalled the war against Iran might be resolved soon, helping unwind some of the weekend’s extreme moves. But the mood is still cautious, and markets remain highly sensitive to any shift in the geopolitical narrative

European stocks have opened higher today, tracking gains in Asia and on Wall Street, while Brent crude oil have fallen more than 8% this morning. But the improvement is tentative. Several Middle Eastern countries have since reported missile threats and drone interceptions, keeping the Strait of Hormuz effectively closed and limiting how far energy prices can retreat. Oil’s extreme intraday swings — the widest since the pandemic’s negative‑price episode — underline how sensitive markets have become to every headline. Cross‑asset volatility remains elevated, and even after yesterday’s drop, Brent is still up more than 50% this year.

The economic damage extends beyond crude: a sustained energy shock delivers a stagflationary impulse, weakening demand and nudging central banks toward more hawkish stances. For now, sentiment has improved, but only at the margin. The backdrop remains fragile and highly reactive to developments in the Middle East.

The US dollar’s rally fizzled out too as it has effectively become an extension of the oil shock. As crude surged through $100, the US dollar index pushed higher, with the correlation between the two flipping decisively positive recently. This isn’t just cyclical; it’s structural. When oil spikes, global demand for dollars rises mechanically because energy is priced, financed and settled in USD. Higher crude tightens global liquidity, stresses EM and credit markets, and triggers the familiar reflex: balance sheets de‑risk into the deepest collateral pool in the world.

That’s why the current move has been self‑reinforcing — oil up, dollar up, risk down. The haven channel simply amplifies it.

If the conflict genuinely moves toward an end though, this dynamic would start to unwind. A sustained fall in crude would ease the global dollar demand created by the petrodollar system, soften the liquidity squeeze and reduce the need for defensive USD positioning. The dollar wouldn’t collapse but the intensity of the move would fade as energy markets normalise and risk appetite rebuilds.

At that point, focus would swing straight back to the macro data — and the backdrop is hardly flattering for the dollar. Last Friday’s dismal US jobs report has already raised questions about the durability of US exceptionalism, and this week’s CPI print becomes even more important. If inflation cools while growth momentum softens, the market will quickly re‑price the Fed path lower, removing another pillar of USD support.

So the sequencing is clear: as long as oil is elevated and the Strait of Hormuz remains constrained, the dollar stays bid; if the conflict eases and crude retreats, the narrative flips back to weak data and a softer Fed outlook.

EUR: Rebounds from four-month low

EUR/USD keeps setting lower daily lows and remains below its 200‑day moving average at 1.1674, but the reversal from four‑month lows suggests the pair is trying to stabilise amidst tentative signs of a broader risk rebound. The bias is still lower, but the pace of downside is slowing.

EUR/USD’s roughly 2% slide since the Middle East crisis began fits neatly with the dollar’s oil‑linked surge and the euro’s sensitivity to European gas prices. Those energy dynamics have more than offset the earlier boost the euro enjoyed from fading US risk premia after the Greenland episode. For now, these two forces — the dollar’s petrodollar bid and Europe’s energy vulnerability — will continue to dominate the pair’s direction until geopolitical conditions stabilise more meaningfully.

A more hawkish ECB is unlikely to offer much protection. History from the Ukraine shock shows that when Europe’s competitiveness deteriorates sharply due to energy costs, the euro tends to weaken regardless of rate expectations. The longer energy prices stay elevated, the more damage is done to the 2026 narrative of synchronised global growth and Europe narrowing the gap with US exceptionalism. Even as US–eurozone rate differentials move in the euro’s favour, the terms‑of‑trade shock is proving far more influential for EUR/USD.

In short, EUR/USD remains a function of energy markets and geopolitics, not central‑bank rhetoric. Until there is a credible path toward a more stable equilibrium in the Middle East, the euro will struggle to escape the gravitational pull of Europe’s worsening terms of trade.

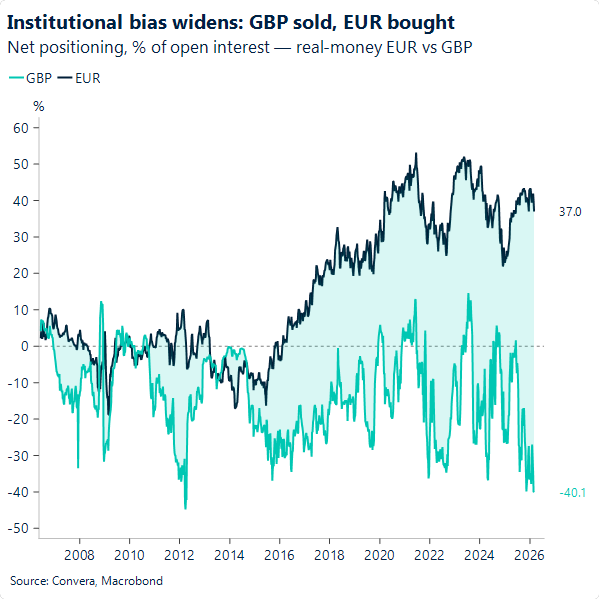

GBP: Positioning buffer

A partial retreat in oil prices yesterday – after smashing through $100 a barrel and briefly flirting with $120 – helped tame markets’ ferocious hawkish repricing that had challenged the BoE’s supposedly easing bias. Earlier in the day, markets had priced as much as 22 bps of tightening by year end, only for those bets to fade almost entirely (~3 bps). The volatility in rates markets, despite a broadly unanimous shift toward a more hawkish stance, underscores investors’ reluctance to commit to a one‑sided scenario given the uncertainty over how durable the conflict will be, even after President Trump signalled the war may end “very soon”.

Short‑end gilt yields have reacted the most forcefully to the conflict‑driven inflation risk compared with other G10 markets. This reflects not only the UK’s reliance on crude but also the current monetary policy path and the balance of risks around it. The Bank’s easing bias remains anchored to the expected deflationary outlook, as the dovish tilt at the February meeting made clear. That said, inflation is still at 3%, with a long way to go before returning to target by April, and given how reticent the Bank has been to accelerate easing, the front end’s sensitivity to oil moves is naturally higher than in peer markets.

Sterling’s bearish posture therefore appears more contained relative to the euro, despite sterling’s higher-beta tendencies, which typically see the currency sell off when sentiment sours. GBP/EUR is roughly 1% higher since the conflict erupted (27 Feb), and options markets signal a clear improvement, though still bearish, in the short‑to‑medium‑term outlook for the pair. Positioning also helps explain sterling’s more muted downside. Net GBP/USD positioning was already heavily short, creating a crowded environment that limits further losses. The euro, by contrast, sits in a much more crowded bullish backdrop against the dollar, which makes any unwind more forceful for the common currency.

With an empty calendar today and no BoE speakers on the agenda, we expect sterling to continue trading war headlines, likely drifting cautiously higher on Trump’s newly conciliatory tone, while also supported by expectations of a relatively more hawkish post‑conflict revamp in the BoE policy path.

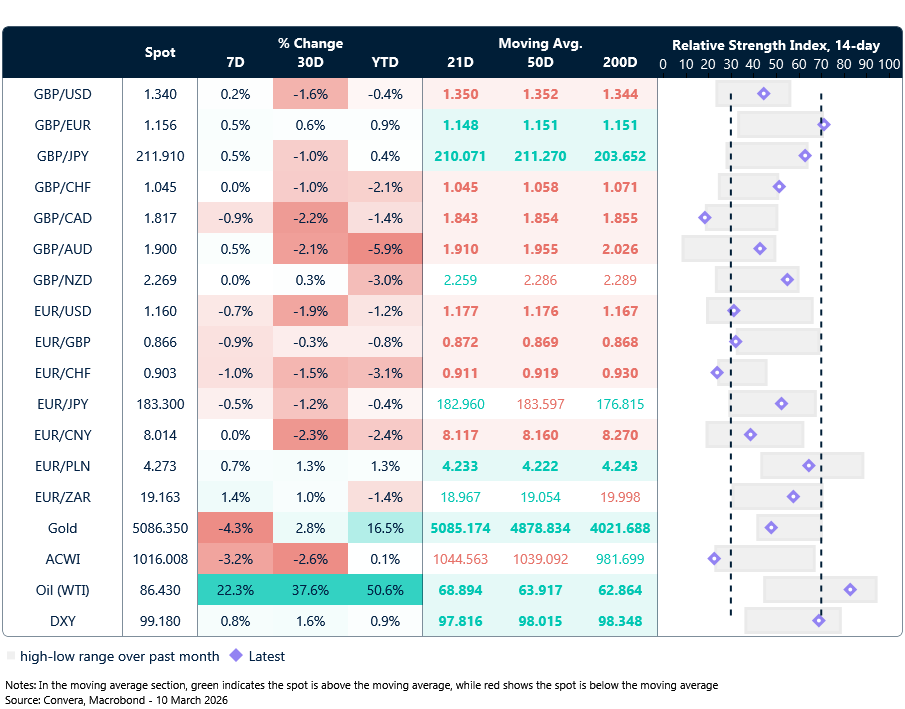

Market snapshot

Table: Currency trends, trading ranges & technical indicators

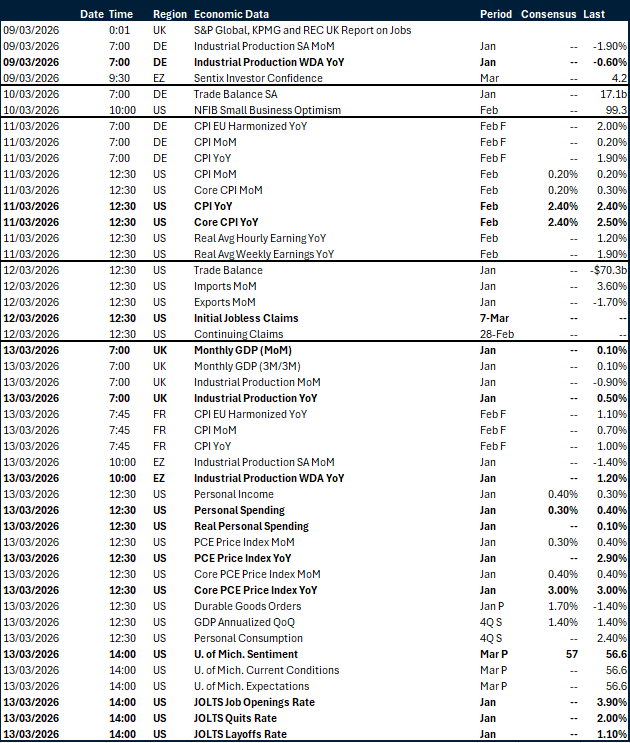

Key global risk events

Calendar: March 09-13

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.