USD: Dollar hits fresh 10-month high

Geopolitical tension remains the dominant macro driver, with recent US actions adding further strain to the Middle East backdrop. Increased military deployments, sharper rhetoric toward Iranian energy assets, and stalled diplomatic overtures have kept the region on edge. Intermittent pauses have done little to alter the trajectory: markets continue to price a higher and more persistent geopolitical risk premium. For the US, the channel is clear—elevated uncertainty feeds directly into oil, risk sentiment, and ultimately the USD.

US equities, meanwhile, remain trapped in a behavioural loop. Every Friday since late February has delivered a sell‑off, followed by a Monday rebound that leaves the S&P higher than Friday’s close. Yesterday’s session followed the script almost perfectly. What’s different this time is the resilience of crude: oil prices have held firm, helping lift the USD to fresh 10‑month highs. Dollar demand largely reflects the structural advantage of US energy independence at a moment when terms of trade have snapped back into focus.

Still, the sustainability of this USD strength hinges on the path of the conflict. A prolonged period of crude above $140 would materially raise US recession risk, making the duration of the crisis the single most important macro variable. The longer uncertainty persists, the greater the likelihood that something breaks—financially, politically, or economically. For now, surging energy prices are supporting the dollar, but that support is conditional. Any de‑escalation would unwind the energy‑premium underpinning the USD and quickly shift attention back to the domestic policy risk premium that weighed on the currency through 2025.

This week’s US data flow adds another layer of potential volatility. The labour market takes centre stage with JOLTS, ADP, and Friday’s March payrolls. Consensus looks for +60k NFP and a rise in unemployment to 4.4%, a combination that would reinforce expectations of Fed tightening later this year as policymakers attempt to counter the inflationary impulse from higher oil. For the USD, the reaction function is straightforward: firmer data supports the dollar; meaningful weakness risks knocking it lower by pulling rate expectations down and raising concerns that the US economy is bending under the energy shock.

EUR: Growth or rates, the euro loses either way

Since the start of the conflict, most of the market action has been concentrated at the short end of the curve, with investors more focused on repricing near‑term policy expectations than long‑term growth. That made sense while consensus still assumed a relatively quick resolution. But yesterday’s yield‑curve behaviour suggests the market may now be shifting focus. Despite no clear end in sight, demand for beaten‑up government bonds, which had tended to fall alongside equities since the conflict began, surged yesterday, with yields dropping across the board. The move was led by the long end, where growth expectations are priced. Put simply, weaker long‑term growth reduces the perceived need for further tightening, easing pressure along the curve, especially further out.

EUR/USD’s reaction to Germany’s above‑consensus March CPI print yesterday (2.7% from 1.9%, est. 2.6%) reinforces this shift. The pair’s daily losses barely retraced, closing 0.4% lower, indicating that as the market pivots toward growth rather than policy, higher inflation and a rates‑for‑longer backdrop become less persuasive drivers for the currency. In this environment, higher oil prices, a direct lever in the repricing of long‑term growth, exert more bearish influence on EUR/USD as relative growth expectations begin to replace rate spreads as the dominant explanatory variable. On that front, the eurozone is the clear loser relative to the US, given its far greater energy dependency versus a US economy supported by domestic production. Yesterday’s sharper drop in UST 10‑year yields relative to Bunds further supports this narrative: lower term premia and stronger safe‑haven demand for US debt continue to favour the USD over the EUR.

This is not to say that euro differentials have lost their sway completely, but the sheer attractiveness of the yield advantage dwindles when inflation becomes top of mind and eats directly into nominal returns. In fact, while nominal rate spreads may be narrowing in favour of the euro, stripping out inflation expectations (2‑year inflation swaps) reveals a much less supportive fundamental backdrop. Real returns on eurozone debt appear less appealing as higher inflation expectations are priced in for the energy‑dependent bloc. Overall, whether you lean toward the growth argument or stick with the rate‑differentials story in this fast‑moving market environment, the euro backdrop appears weak.

EUR/USD continues to trend lower toward the March 13 low at 1.1411, with a downward‑sloping 21‑day MA guiding the move. A second bounce off 1.14 appears less likely given the market dynamics outlined above. Absent a conciliatory shift from Iran, a break through those levels looks increasingly warranted in the coming weeks. For today, all eyes on the March CPI for the eurozone, expected to climb 0.7% from 1.9% to 2.7% as conflict-driven inflation begins to bite.

GBP: Five-day slide puts 1.30 back in view

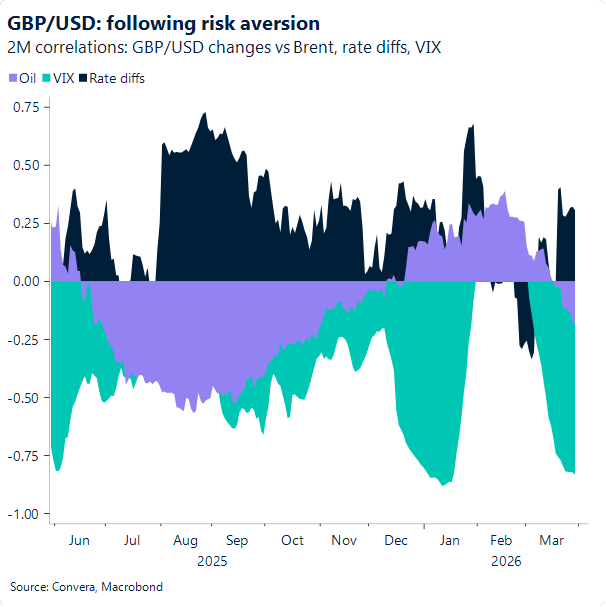

GBP/USD has now fallen for five consecutive sessions, shedding roughly 2% and trading almost 5% below its YTD high. Yesterday’s move was particularly significant: the pair finally broke below the 1.32 support we had flagged, raising the risk of a test of the psychologically important 1.30 handle — a level sterling hasn’t breached in almost a year. With risk appetite deteriorating and energy prices still elevated, the near‑term bias remains skewed lower.

The geopolitical backdrop is doing sterling no favours. Markets are grappling with contradictory signals from Washington. On one side, reports suggest President Trump is prepared to escalate militarily, including a potential operation to extract uranium from Iran and even a strike on Kharg Island, the country’s critical oil‑loading hub. On the other, he claims Tehran is allowing more tankers through the Strait of Hormuz, hinting at progress in negotiations. The result is a volatile, two‑way uncertainty that keeps the dollar supported ultimately for now, leaving GBP/USD stuck in a grinding downtrend.

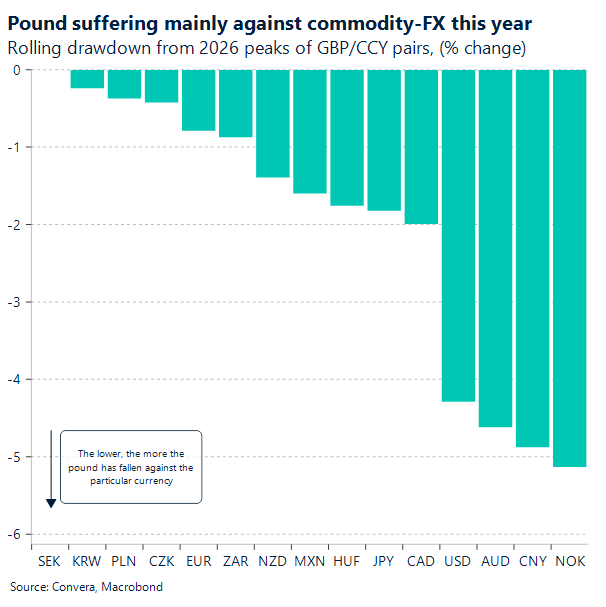

Indeed, sterling’s weakness this year has been most pronounced against commodity‑linked currencies, where the terms‑of‑trade shock is biting hardest. From their 2026 peaks, GBP’s largest drawdowns have come against NOK, AUD, CAD and USD — all currencies with either direct energy exposure or strong commodity‑beta. In contrast, GBP has held up better against low‑yielding or Europe‑centric peers, underscoring how the current environment is punishing energy importers while rewarding economies with commodity buffers.

Domestically, the data offers little offset. The Lloyds Business Barometer showed headline confidence holding steady in March, but the underlying picture is more uneven, with sentiment diverging sharply by firm size. This comes at a time when the UK is estimated to face the largest growth hit among major economies from the US–Iran conflict, reflecting its acute exposure to energy imports and already‑soft underlying momentum.

Consumer‑side indicators reinforce the fragility. Confidence has deteriorated, retail sales have slipped back into contraction and households appear to be tightening spending even before the latest geopolitical shock fully feeds through. The UK enters this phase on weaker footing than in 2022 — with higher rates, thinner savings buffers and less fiscal insulation — making it more vulnerable to an externally driven inflation shock.

Against this backdrop, sterling’s earlier resilience looks increasingly difficult to sustain. With the break below 1.32 now confirmed, 1.30 becomes the next key downside target. Unless geopolitical tensions ease meaningfully, energy prices follow, and risk sentiment improves, rallies are likely to be shallow, and GBP/USD remains at risk of extending its decline in the days ahead.

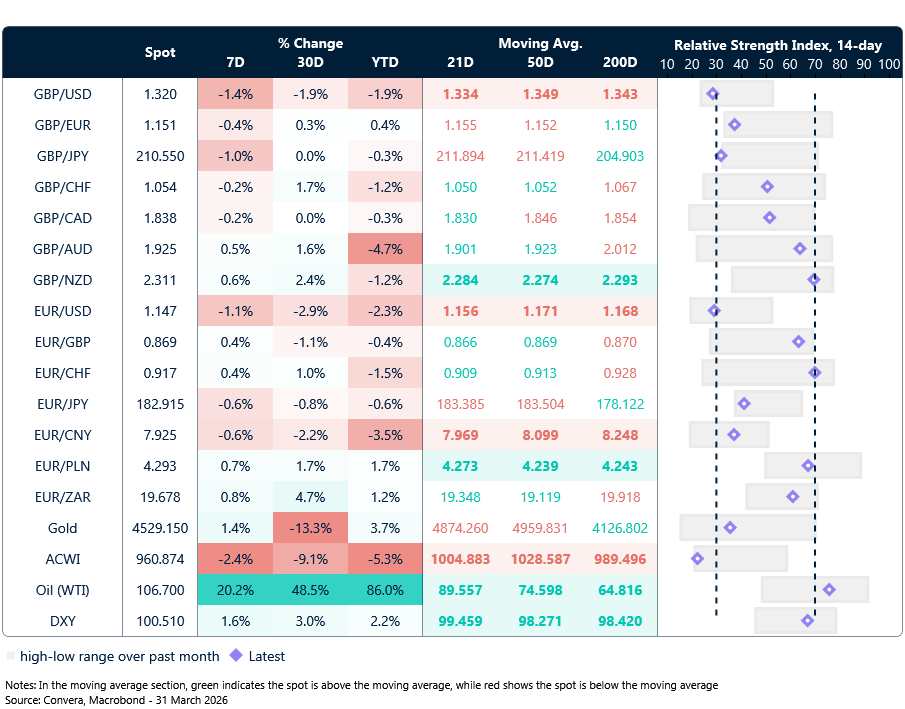

Market snapshot

Table: Currency trends, trading ranges & technical indicators

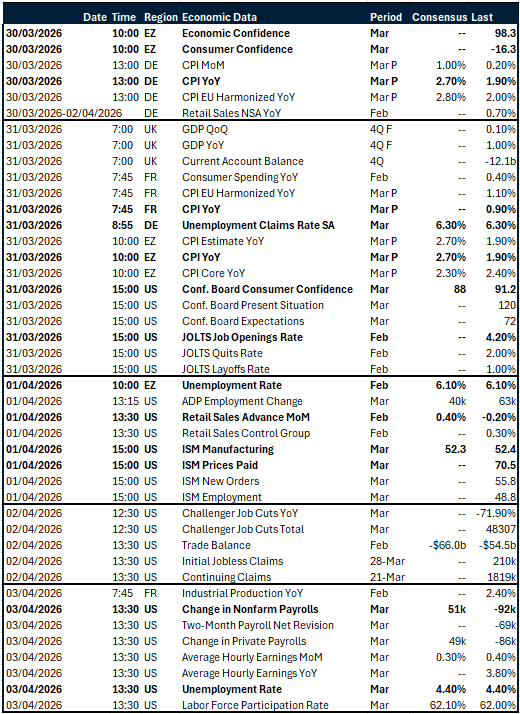

Key global risk events

Calendar: March 30 – April 3

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.