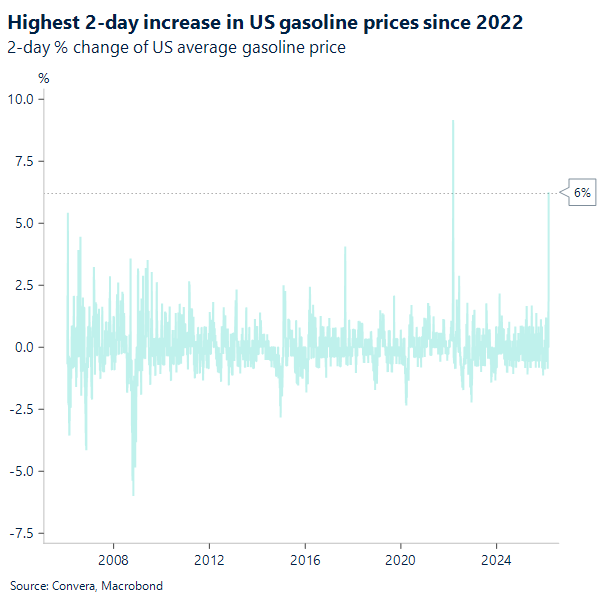

ME Conflict: Markets reprice risk as endgame stretches out

Markets remain hypersensitive to headline risk as crude hovers near $84 after a fresh bout of risk premia, and the policy calculus still revolves around containing energy‑driven inflation while sustaining operational tempo. On the ground, Iran’s response has deteriorated sharply. After the Iranian leader Ali Khamenei was killed in the opening phase, the country has further fractured command and control, turning what began as an offensive push into a grind of attrition and interdiction rather than coordinated escalation.

It’s becoming increasingly clear that a speedy resolution was likely wishful thinking; prediction market platforms now see only a 25% shot at a truce before the month wraps up. Meanwhile, crude prices are creeping upward as doubts linger over whether naval protection can truly keep trade flowing through the Strait of Hormuz, ensuring a layer of tension remains baked into the price. The broader market response has been a bit of a mixed bag: while the S&P 500 brushed off the volatility in record time, South Korean equities plummeted into a deep slump and are still struggling to find their footing despite a brief attempt at a comeback.

The central uncertainty is whether investors have fully baked in the potential for a stalled peace process and continued maritime bottlenecks. While the initial shock usually carries the most weight, the trajectory from here relies on three pivotal factors: the steady decline of Tehran’s offensive reach, the resolve of neighboring states to keep Iran sidelined, and the effectiveness of US efforts to shield cargo and prevent a spike in pump prices.

It seems now that the strategic aim is to leave Iran sufficiently weakened to accept terms without triggering a total collapse, and there are hints that Tehran is weighing its options for a way out. If these discussions gain momentum and sea lanes stabilize, the current “fear tax” should dissipate; if not, another round of market adjustments is likely on the horizon.

CAD: Energy trade persists, credit fears mount

Bank of Canada Governor Tiff Macklem announced a major update to the nation’s financial “plumbing” yesterday in Toronto, signaling a shift toward central clearing for its repo operations. By planning to join the Canadian Collateral Management Service (CCMS) by early 2027, the central bank aims to automate transactions and remove the friction that often leads to interest rate spikes during quarter-end reporting cycles. This move is designed to ensure that monetary policy flows smoothly through the economy, preventing technical bottlenecks from distorting the effective interest rates that businesses and consumers actually face.

This modernization effort is particularly timely given the growing anxiety surrounding “shadow banking” and the rapid expansion of private credit. Macklem highlighted the risks posed by high-leverage bets from hedge funds, noting that the financial system needs stronger infrastructure to absorb shocks rather than amplify them. By centralizing these operations and eventually integrating with the Canadian Derivatives Clearing Corporation, the Bank is creating a buffer against potential liquidity freezes. If private credit defaults were to rise, this reinforced system ensures that the broader market remains functional even under significant stress.

The push for domestic stability comes at a time when the Canadian economy is navigating a complex “soft landing” scenario. While the central bank’s recent interest rate cuts are beginning to offer some relief to households, structural challenges like stagnant productivity and trade uncertainties continue to weigh on long-term growth. These internal upgrades to the repo market are essential for building a resilient foundation, ensuring that the financial system can support the economy even if external volatility or credit market jitters begin to test the limits of Canada’s investment landscape.

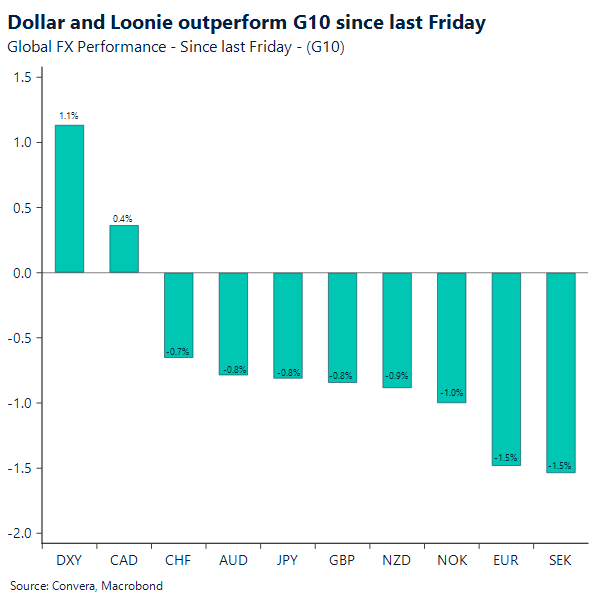

While the Bank of Canada focuses on these structural reinforcements, the Canadian dollar’s movement remains heavily influenced by external factors. As noted in yesterday’s daily blog report, the Loonie’s recent performance has been closely tied to the “energy dependence trade” in FX markets. Because Canada remains a major energy exporter, its currency is uniquely sensitive to shifts in global oil prices and energy demand. This reliance has created a performance gap compared to other major currencies. This has opened a window of opportunity for the EUR/CAD and EUR/GBP crosses which are trading at their lowest levels in almost a year.

LatAm FX: Geoeconomics stall emerging markets

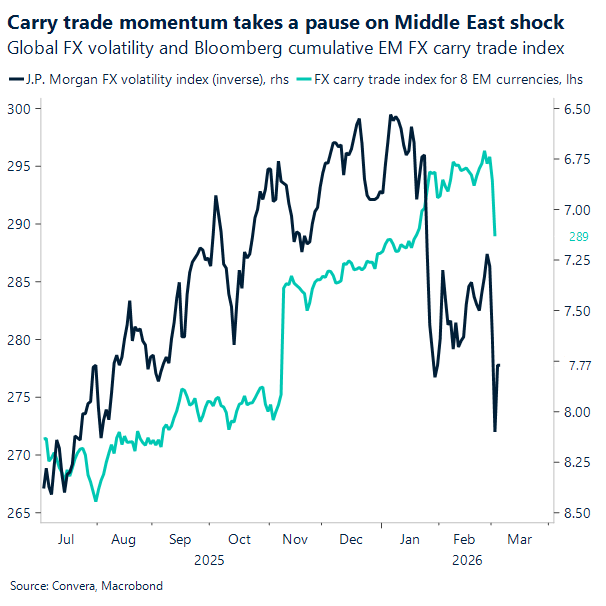

Emerging market currencies initially kicked off the year with significant strength, driven by aggressive portfolio diversification and improved terms of trade for commodity exporters. Latin America, in particular, attracted a massive surge of inflows in January that sparked outsized moves in the Brazilian and Mexican equity markets. While these high-yield destinations were once solidified as compelling targets for global capital due to their commodity exposure and proximity to the U.S. market, the narrative has shifted as geopolitical volatility triggers a move away from risk. The escalation of the U.S.-Iran conflict and the effective closure of the Strait of Hormuz have fueled a risk-off surge into the U.S. dollar, abruptly capping the advancement of emerging assets.

The Mexican peso has hit a six-week low, weakening toward 17.7 per dollar as global investors shift toward safer assets. This dip follows a record $6.48 billion trade deficit in January, largely driven by a sharp 33.5% drop in oil exports and a 9% decline in auto shipments to the US market. Essentially, the energy and industrial sectors, traditionally Mexico’s biggest economic engines, are currently facing a bit of a perfect storm, turning previous strengths into temporary hurdles.

This rising dollar creates one of the most challenging backdrops for emerging market assets seen in the past year, as the greenback’s safe-haven status is now compounded by its tendency to amplify energy shocks. A stronger dollar inherently tightens global financial conditions, pressuring balance sheets burdened with dollar-denominated debt and weighing on cross-border lending and trade. While investors previously expect high-yield markets to resume their upward trend once risk appetite returns, the current environment of higher yields and tightened liquidity suggests a much more arduous path forward. The systemic pressure of a dominant US currency continues to weigh on risk assets, making the resilience of Latin American markets increasingly dependent on a de-escalation of global tensions.

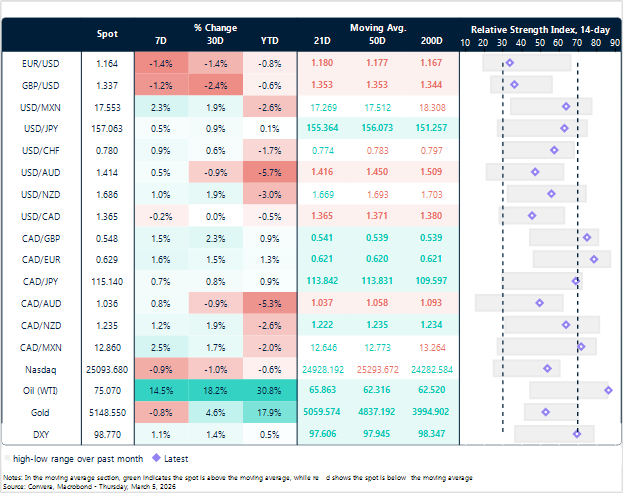

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

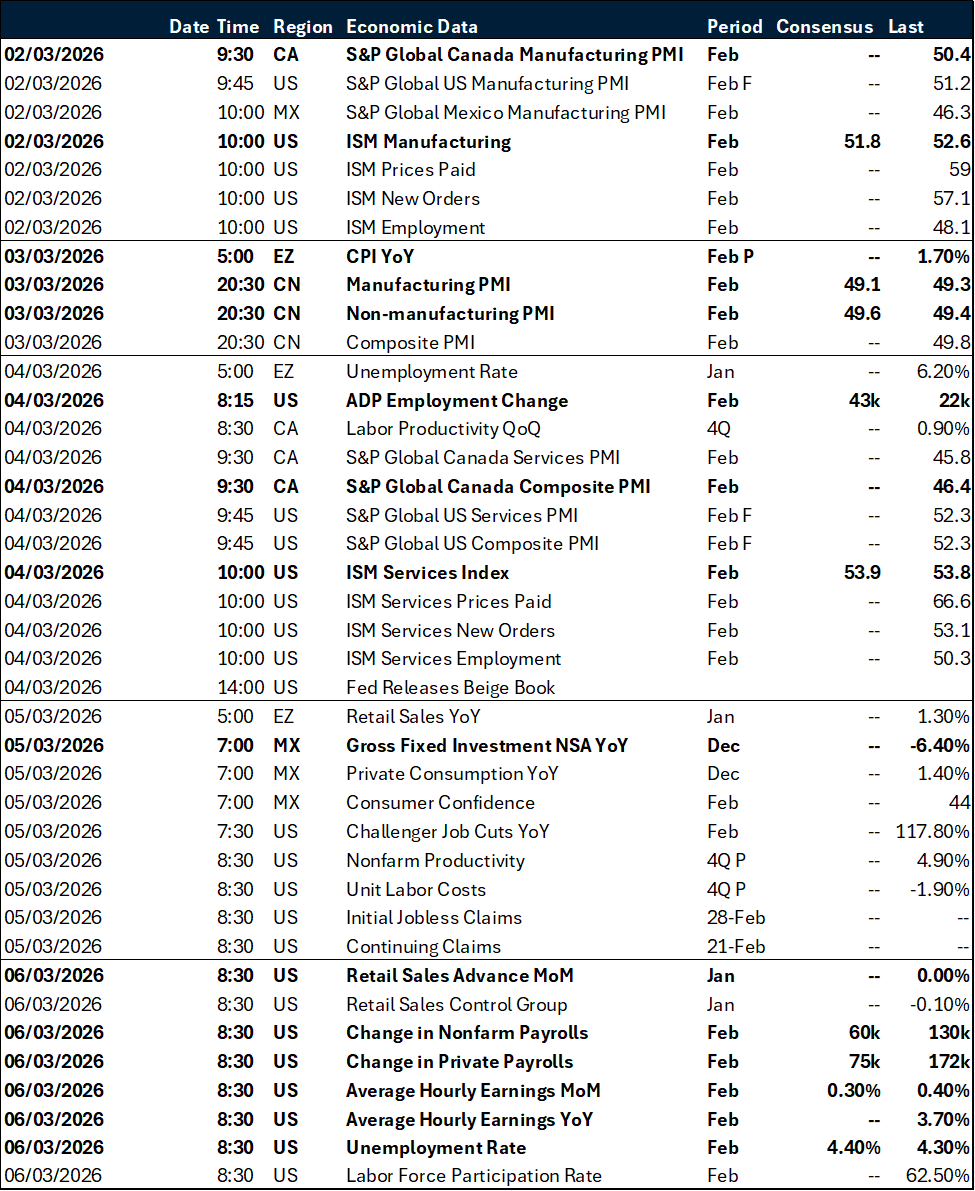

Calendar: March 2 – 6

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.