US September NFP payrolls: Even though these job figures come with a six-week delay, they are certainly grabbing the market’s attention and pushing stock futures to near session highs. The headline number was a massive upside surprise, with September payrolls jumping by 119,000, crushing the 51,000 estimate, driven largely by hiring in health care and food services. While there was a slight downward revision of 33,000 to the previous two months, it doesn’t take much shine off this beat. Interestingly, the unemployment rate ticked up unexpectedly to 4.4%, but because labor force participation also climbed, this isn’t necessarily bad news. For the FOMC, this creates a nuanced backdrop; since payrolls alone don’t fully signal if the labor market is easing, a December rate cut remains possible only if other indicators show sufficient weakness.

Dollar up, Fed blind, Nvidia the only game in town

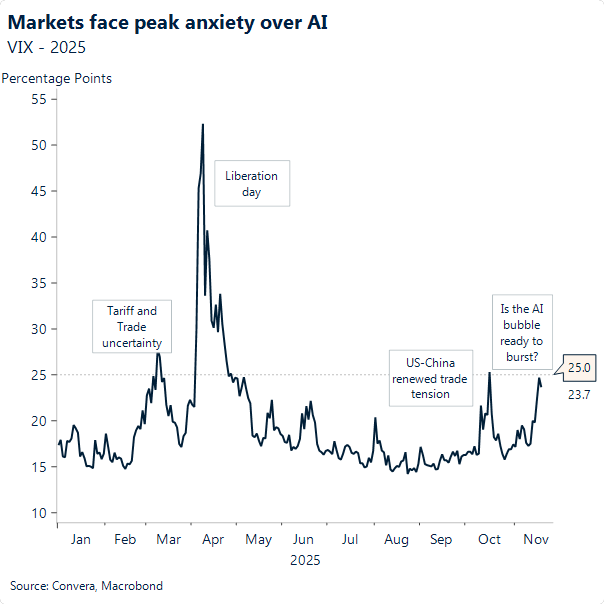

As mentioned this past Monday, if doubt was to persist around Fed’s next step, the dollar’s path of least resistance was upward. That played out this week: while equity markets treaded downward searching for a catalyst, the dollar held strong. It felt as if a “lot of nothing” was happening until yesterday, when a confluence of news, headlined by Nvidia’s mega results, calmed the markets, for now. Before this relief, investors were trading in a vacuum, clinging to alternative data because the official numbers just aren’t there. This lack of clarity hits at a crucial moment with the VIX near 25, levels unseen since tariff threats re-escalated, igniting a debate on whether recent tech and crypto selloffs are merely a modest correction or the popping of a bubble.

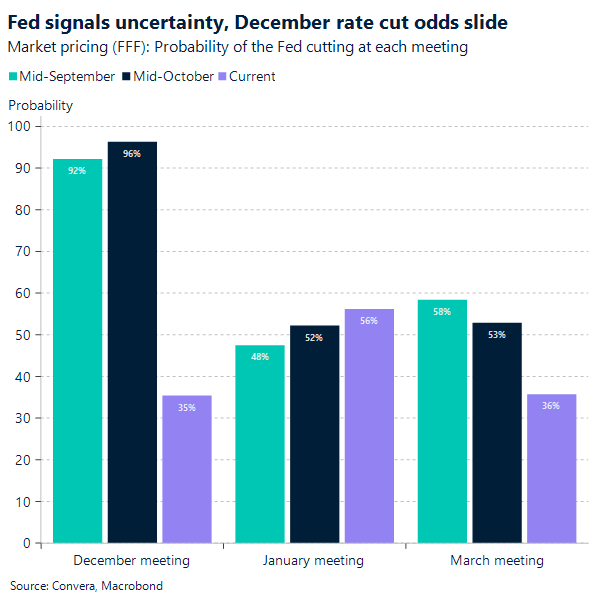

The confusion is being compounded by the Federal Reserve itself. Minutes released this afternoon reveal a central bank that is deeply divided, with “many” officials, a significant minority, believing it likely appropriate to keep rates steady for the rest of 2025. This hawkish tone, reinforced by voting dissenters pushing for everything from a pause to a deeper cut, has dampened hopes for a December easing. Odds of a third rate cut this year have dropped to 30%. Policymakers are explicitly worried about “stretched asset valuations” and sticky inflation, shifting the narrative from a guaranteed cut to a nervous “wait-and-see” stance.

To make matters worse, the Fed is essentially flying blind into its final meeting of the year. In a historic first since 1994, the Bureau of Labor Statistics cancelled the October employment report due to the government shutdown and won’t release the November data until December 16. That is a week after the Fed meets on December 9–10. With the only reliable comprehensive look at the labor market coming from September’s data, set to be released today, rather than the usual Friday, the central bank lacks the critical feedback loop needed to navigate these divided opinions, further lowering the odds of a December cut.

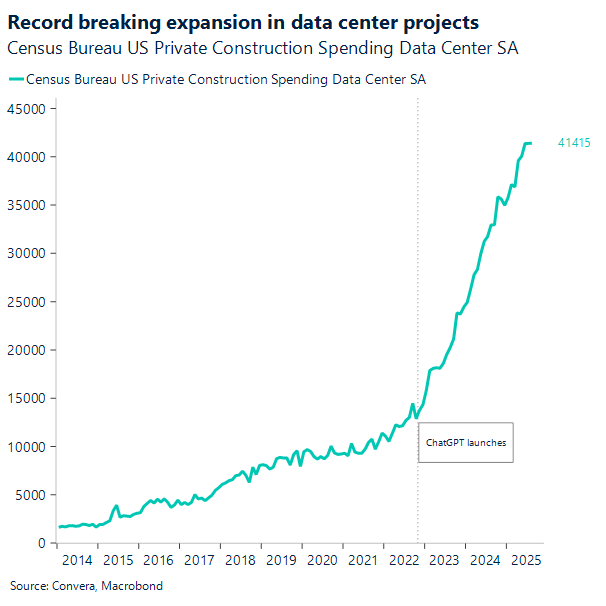

However, despite the macro fog and fears of financial contagion, the “bubble” narrative faces a reality check from the sheer scale of AI infrastructure growth. We aren’t just looking at hype; we are seeing tangible economic drivers in the form of massive data center construction by tech giants like Google and Microsoft. Global capex on these facilities is projected to top $1.7 trillion by 2030, and AI investment already contributed significantly to U.S. GDP growth in the first half of 2025. This infrastructure is rapidly becoming the backbone of the digital economy, creating a floor for the market that speculation alone can’t provide.

Yet, even this infrastructure boom has a potential trap door. Michael Burry is betting big that the numbers don’t add up, specifically pointing to a massive accounting blind spot: depreciation. His argument is that Big Tech is extending the “useful life” of their servers on paper far beyond their actual 12-to-18-month burnout rate, potentially inflating reported earnings by as much as $176 billion over the next few years. Burry’s Scion Asset Management has even shorted Nvidia and Palantir, wagering that this is a dot-com style illusion where obsolescence is being ignored to boost profits. However, the counter-narrative is just as strong; proponents argue that hyperscalers like Microsoft and Google aren’t just throwing away chips but are repurposing older hardware for inference and leveraging massive economies of scale. It’s a high-stakes debate over whether we are looking at financial engineering or genuine operational efficiency.

This is why Nvidia’s earnings beat yesterday was so pivotal. By delivering strong results and an optimistic outlook, they provided the concrete evidence investors needed to confirm that the AI boom is built on real, structural demand rather than just vapor, regardless of the accounting debates. While the Fed struggles with internal splits and missing government data, the corporate sector’s relentless push into AI offers a counter-narrative of productivity and growth, suggesting that even if the monetary path is rocky, the technological engine of the economy is still running strong.

GBP: Markets see Bailey warming to December cut

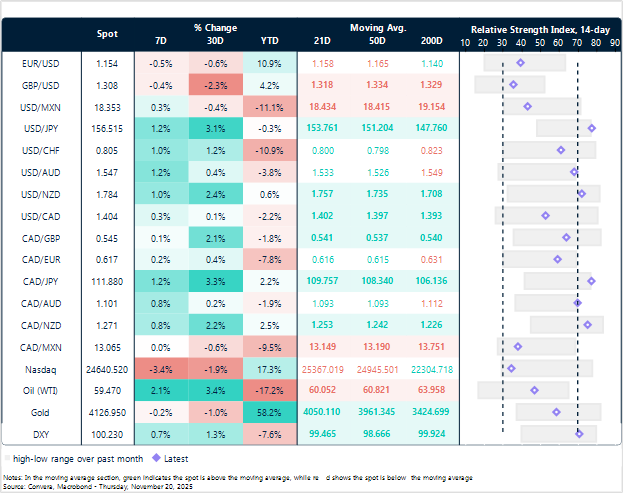

About ten days ago we were gearing up for a slew of macro data that would help us frame, from a data‑driven angle, Bailey’s hesitant dovishness at his November policy meeting. Fast forward to today, and the picture points to further deterioration in the labour market (e.g., unemployment at 5%), slower Q3 growth than expected (0.1%), and easing inflation (despite some pockets of pressure still evident – food inflation at 4.9%).

Markets may have expected more progress on inflation. After all, it did not fall as low as anticipated (3.5% est. vs. 3.6%). A December cut remains priced at roughly 87% (vs ~72% on Monday last week), a sharper easing in inflation might have closed out any residual doubts about an uncut scenario.

GBP/USD had held its ground at support around 1.31, before slipping below on USD strength, yesterday. A mix of renewed hawkishness and uncertainty from yesterday’s October Fed minutes, alongside news that October NFP will not be released, has lowered the probability of a Fed cut in September to about 35% (down from ~50% earlier yesterday), leaving the greenback well-supported. Adding to this, fiscal anxiety continues to linger in the run-up to the budget, now just around the corner. Pressure persists on the long end of the curve, with 30-year gilt yields climbing to the highest in over a month (~5.45%) following Reeves’ U-turn on income tax hiking plans.

Today is a quiet one for the UK on the data front, but tomorrow brings PMIs, along with retail sales and public sector borrowing. The latter has drawn particular attention as we near the budget.

Monthly borrowing figures are volatile and prone to revision, but in recent years the UK has tended to overshoot OBR forecasts (as in September and August). With inflation still high and growth weak, forgone tax revenues combined with persistently elevated borrowing costs (as investors demand greater returns in the face of inflation pressures) have made overshooting a recurring reality – underscoring the challenge Reeves faces with the budget just a week away.

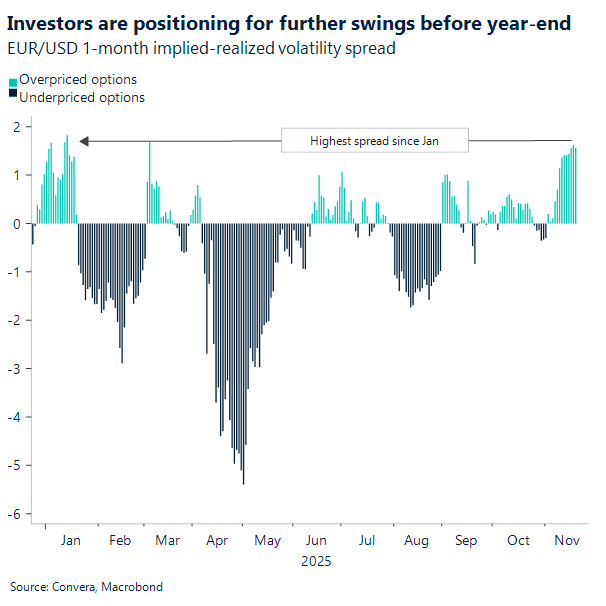

EUR: Euro’s toughest session this November

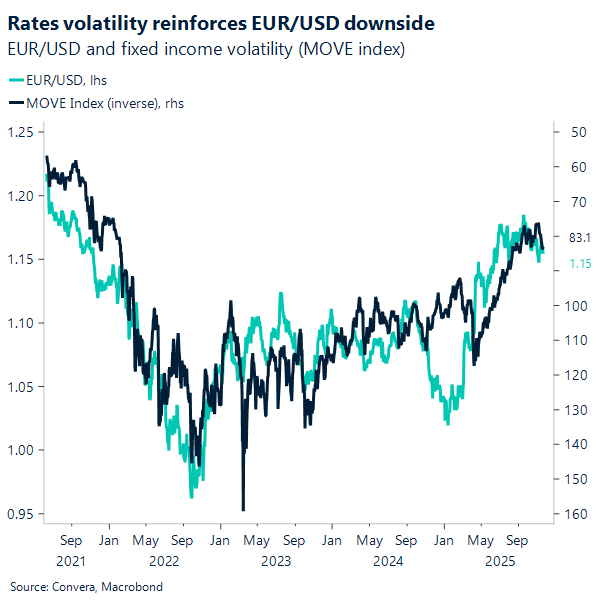

The euro endured its sharpest drop of the month against the US dollar yesterday as risk-off flows drove demand for the safe haven USD. Bond market volatility has surged to a two‑month high, with the ICE BofA MOVE Index climbing almost uninterrupted through November. Elevated rates volatility typically strengthens the dollar’s defensive appeal, and EUR/USD has once again tracked lower in line with that historical correlation.

Interestingly, realised one‑month EUR/USD volatility has slipped to around 4.9% through November yet implied volatility has firmed to 6.5%. That divergence signals investors are positioning for further swings before year‑end. Risk reversals remain skewed toward EUR upside, showing markets haven’t abandoned the idea of a late‑year euro rebound. But for that to materialise, softer US data and a December Fed cut are key — and with the jobs report delayed, near‑term risks lean lower. A break under $1.15 is plausible, with the 200‑day moving average at $1.14 acting as both a magnet and potential support if dollar demand persists.

Elsewhere, the yen remains the weakest G10 currency, allowing the euro to extend gains. EUR/JPY is up more than 2% month‑to‑date and over 11% year‑to‑date, hitting fresh all‑time highs this morning. With the ECB effectively done easing — and a rate hike still a live possibility despite markets pricing in a tail risk of cuts — the policy backdrop favours further upside. Even in uncharted territory, EUR/JPY looks set to carry momentum into year‑end.

DXY breaks north of 100, once more

Table: Currency trends, trading ranges and technical indicators

Key global risk events

Calendar: November 17-21

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.