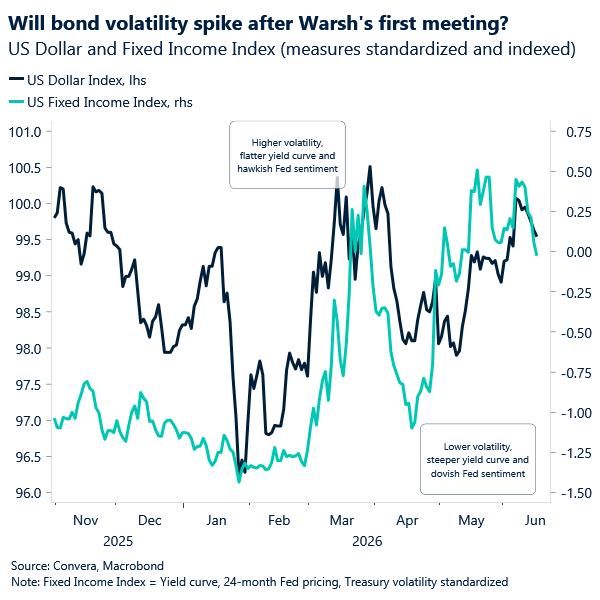

USD: No hike needed for a hawkish Warsh debut

Even if the geopolitical temperature has come down, along with oil prices, the inflation backdrop hasn’t changed much. And while energy pressure is easing, for the Fed it may be enough, as it balances out decent economic activity along with a resurgent labor market. That puts Kevin Warsh’s first meeting as chair on center stage. Today’s meeting won’t bring a rate hike. The risk event may be a tougher Fed signal dressed up as a hold. Warsh has spent years arguing that central banks over-communicate. He thinks too much forward guidance boxes policymakers in. Markets assume he plans to change that. Fast.

That shift could start immediately, starting today. A Fed that says less gives markets less to lean on. A Fed that refuses to pre-commit leaves investors to do more of the work themselves. That may be good for policy flexibility. It is rarely good for market calm. The first place to watch is the “dot plot” as this meeting brings a new SEP. In March, the median path still penciled in one cut in 2026. Now the risk is that the dots drift toward none. That would matter more than the rate decision itself.

A move higher in the projected path through 2028 would send a simple message: rates may be on hold, but they are not headed down any time soon. Higher for longer would shift from being last few years’ slogan and start looking like the base case, again. That is a risk for markets. Before the conflict, investors spent months hoping the next big debate would be about the timing of cuts. Warsh could use his first meeting to tell them not only they are asking the wrong question, but he may not be as dovish as many anticipate. The issue may no longer be when easing begins. It may be whether 2026 gets any easing at all.

The second risk ahead of today’s meeting, sits in the balance sheet. Since December, the Fed’s reserve-management purchases have slowed. Those purchases, mostly in Treasury bills, have helped cushion liquidity conditions. At the same time, Treasury issuance is poised to climb in the third quarter. More supply. Less Fed support. That is not a friendly mix.

If Warsh signals that bill purchases could slow further, or end altogether, markets will take notice. The effect would not look like a rate hike. It would still tighten conditions. Front-end yields could rise and keep supporting the US Dollar. Liquidity could thin. Duration supply would matter more and the term premium could do the rest of the work. That would fit Warsh’s thinking, at least that’s what markets have been anticipating. He has long been skeptical of using the balance sheet as an all-purpose policy tool. Lower rates paired with a smaller Fed footprint has always been closer to his thinking than easy conditions plus a bloated balance sheet. If that bias comes through on Wednesday, long-end yields may have to adjust, even if the funds rate does not.

Finally, the biggest risk over time could be less guidance. For years, markets have traded a Fed that signaled early and often. Investors got used to having a road map of sorts. Warsh may prefer to hand out fewer maps. If he does, volatility might spike around Fed meetings and even more around key macro data releases, mainly because markets have not had to handle this Fed style in a long time.

It’ll be an interesting meeting. Would there be any dissents? Unlikely. How will Warsh manage his first meeting with Powell as a part of the committee? Only a few people will know. Could this be the start of a big change in the modus operandi? We’ll see.

The Fed may stand pat. But a hawkish dot plot, less balance-sheet support and a deliberate retreat from forward guidance could still amount to a meaningful tightening signal. Markets looking for comfort in a hold may not get much of it, and the US Dollar may continue finding support, even as oil prices fall.

GBP: UK inflation miss nudges BoE toward extended pause

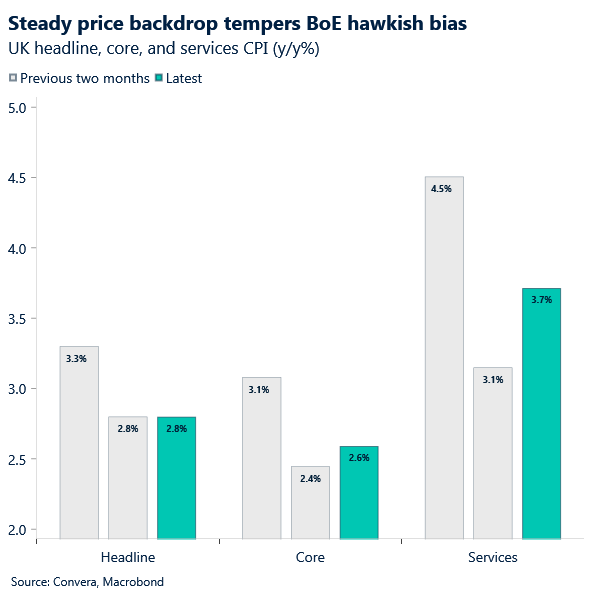

This morning saw the release of the UK’s May CPI report. Headline inflation held at 2.8%, unchanged from April and below expectations of 3.0%. Services inflation, a key gauge of domestic price pressures, surprised to the upside (3.7% vs est. 3.6%), tempering the initial hawkish unwind prompted by the softer headline print. Sterling weakened across the majors. The data strengthens the case for a prolonged Bank of England pause rather than further tightening this year. Markets had already been scaling back hawkish expectations, with a full rate hike pushed out to November 2026. Following today’s release, that pricing looks even less convincing. The UK economy continues to face a softening labour market, while the recent decline in oil prices following the US-Iran peace deal announcement has further accelerated the unwind of the market’s hawkish bias.

Attention now turns to how these easing-friendly developments shape tomorrow’s MPC vote split and forward guidance. With no updated economic forecasts and the geopolitical backdrop still evolving, a measured and cautious tone remains the most likely outcome. However, given the entrenched hawkish bias of recent months, any explicit signal that easing could resume later in the year, should inflation pressures moderate, may weigh on the pound (prior to the conflict markets priced two cuts by year-end).

Aside from the policy meeting, focus also shifts to tomorrow’s UK labour market report and the Makerfield by-election. The latter is widely viewed as a potential pathway for Andy Burnham to return to Westminster and position himself for a leadership challenge to Prime Minister Keir Starmer. The political angle is unlikely to drive sterling in the near term, as a Burnham victory would align with an already familiar narrative. The more material risk for GBP lies in how orderly any potential leadership transition proves to be.

CAD: Data points to bounce, Loonie lags

Canada’s domestic data released on Tuesday were solid. Manufacturing sales rose 4.2% in April to C$77.1 billion, extending March’s gain and marking another strong month for the factory sector. Petroleum and coal product sales hit another record, food manufacturing also reached a new high, and Alberta and Quebec led the provincial advance. With shipments outpacing stock building, the inventory-to-sales ratio fell to 1.62, its lowest since January 2023.

The strength carried into distribution. Wholesale sales rose 0.6% in April to C$89.3 billion, with the building materials and supplies subsector posting a fourth straight monthly increase. Ontario and British Columbia did most of the lifting, offsetting declines elsewhere, while wholesale inventories rose 1.1% on the month as motor vehicles and construction-related goods flowed in.

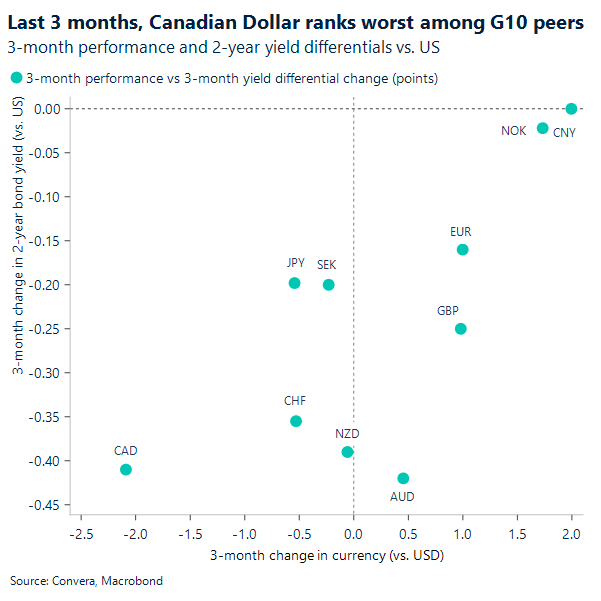

Put together, the data strengthen the case that Canadian activity found firmer footing in Q2 after back-to-back GDP contractions. Yet USD/CAD continues to hover near 1.40. Domestic data have improved, but yield spreads remain decisively in the US dollar’s favor, still north of 130bp. As the chart below shows, the Canadian dollar has been the weakest performer in the G10 over the past three months, with the widening rate gap doing a big part of the damage. Attention today will be on Warsh debut as Fed Chairman.

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

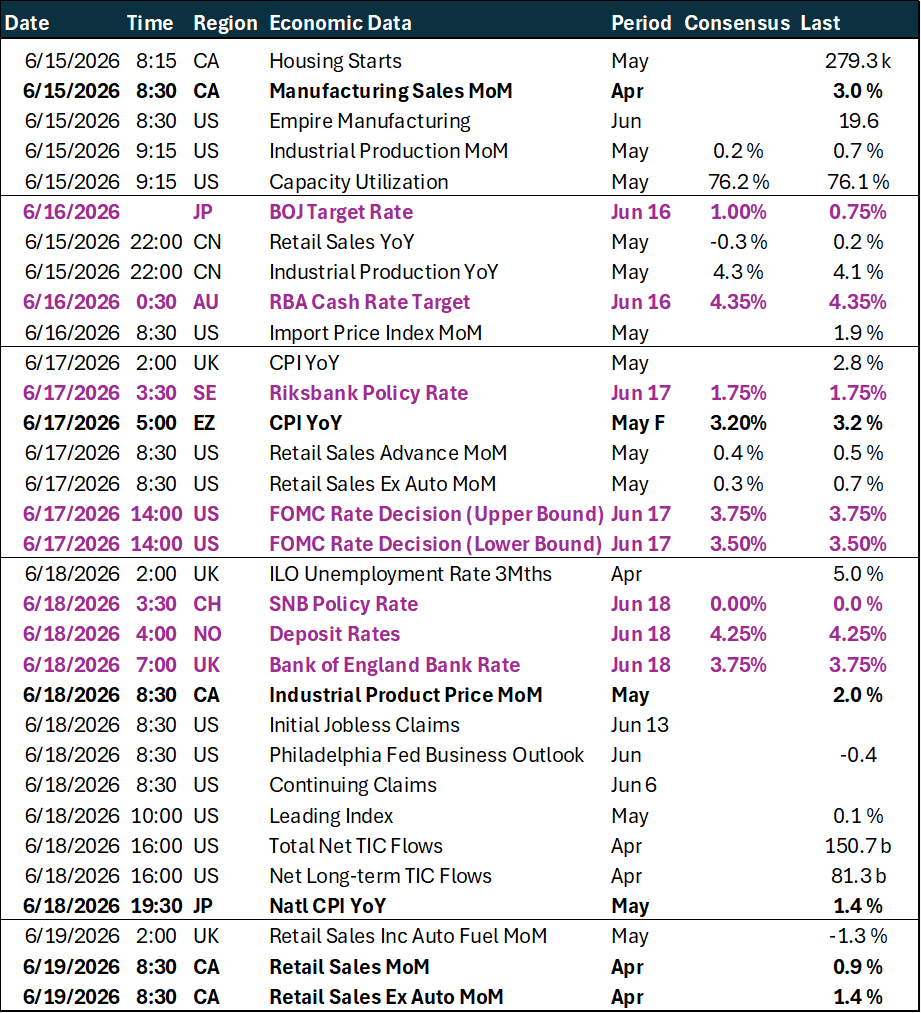

Calendar: June 15-19

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.