Regional shock reprices the world

The Middle East conflict has shifted decisively into a regional shock, with markets now trading the fallout rather than the headlines. Five days of Israeli strikes on Tehran and Iran’s missile attacks on Qatar, Bahrain and Oman have pushed investors into a deeper reassessment of global growth, inflation and policy risk.

Equities have borne the brunt with the US S&P 500 sliding to its weakest level since December, while Asia endured outright capitulation. The MSCI Asia‑Pacific index fell more than 4%, extending the region’s sharp de‑risking. Korea was the epicentre of the turmoil: the Kospi plunged a record 12% in a chaotic session, triggering a circuit breaker.

The parallel selloff in bonds reflects not only a rising geopolitical risk premium but also mounting concern that central banks may have to keep borrowing costs elevated to contain an energy‑driven inflation shock.

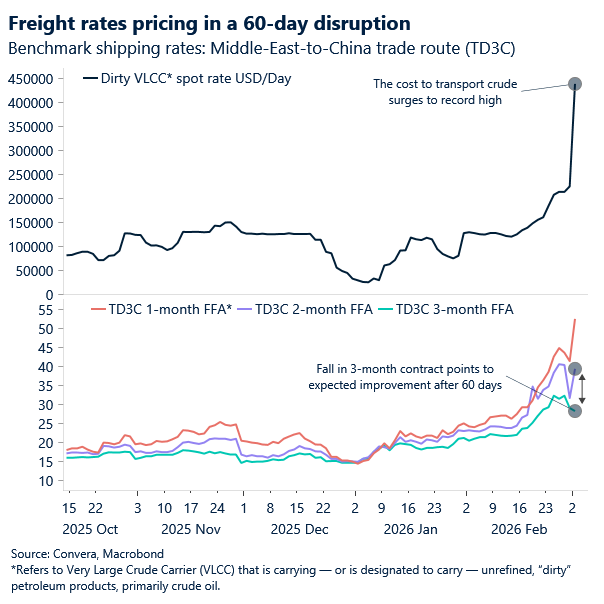

Oil’s circa 15% surge so far this week was tempered after Washington pledged to escort and insure vessels through the Strait of Hormuz, a reminder of how central the chokepoint is to global supply. But the price of black gold is on the rise once again this morning. The forward-looking signals remain uneasy too. Shipping futures on the key Middle East–to–China crude route tell the story clearly: near‑term contracts have jumped, while prices for three months out have softened. In simple terms, traders expect disruption right now but don’t yet see it lasting all summer. It’s the classic signature of a short, sharp shock rather than a structural break — but one that could flip quickly if shipping lanes come under sustained threat.

War dollar

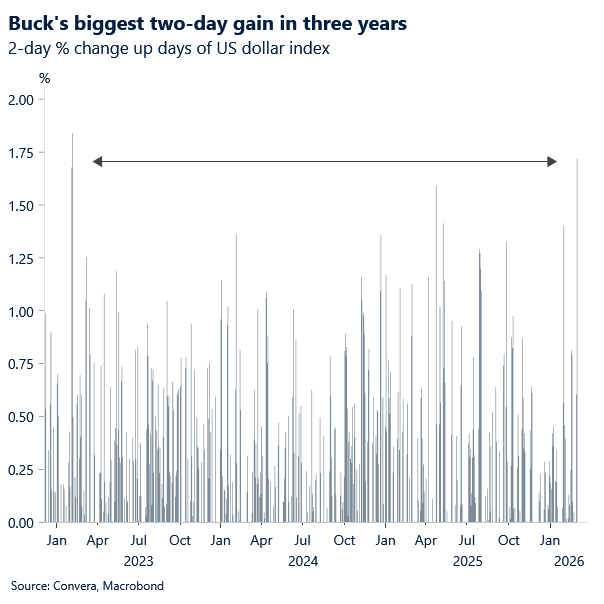

The US dollar has emerged as the clearest macro winner. It has just logged its strongest two‑day rally in nearly a year, outpacing even gold and Treasuries as investors search for liquidity, safety and relative economic insulation. The US’s position as a net energy exporter gives it a terms‑of‑trade advantage that Europe and Asia lack, and the dollar’s behaviour fits the historical template of supply‑driven oil shocks: when energy prices rise because of disrupted supply rather than strong demand, the greenback tends to outperform.

The comparison with the early months of Russia’s invasion of Ukraine is instructive. Then, Brent rallied more than 30% and the dollar ultimately gained over 15% as markets digested the growth and inflation fallout. Today’s dynamics rhyme: the Fed remains the most dovishly priced G10 central bank, yet the US economy is better placed to absorb higher oil than its energy‑importing peers. That combination leaves room for further dollar appreciation if the conflict persists or broadens.

The next test is whether shipping lanes remain secure and whether missile activity spreads further across the Gulf — the point at which a short‑term shock could start to look like something more enduring.

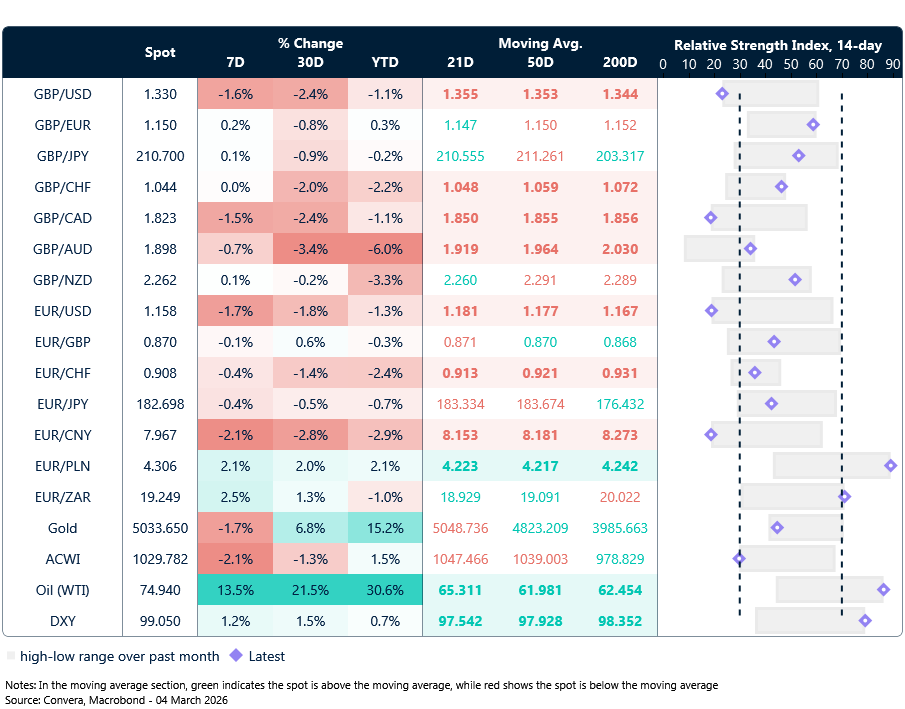

EUR: Europe’s terms-of-trade problem is back

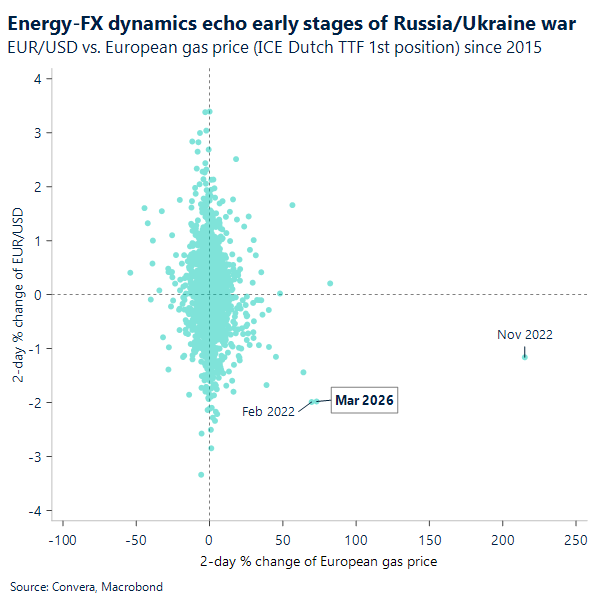

The euro is sliding back into a familiar pattern as the Middle East conflict triggers an energy‑market shock that looks uncomfortably reminiscent of the early days of Russia’s invasion of Ukraine. Today’s pattern is similar in structure, if not yet in magnitude. The Middle East conflict is again raising the prospect of energy supply disruption, and the market is responding in the same sequence: gas prices up, EUR/USD down.

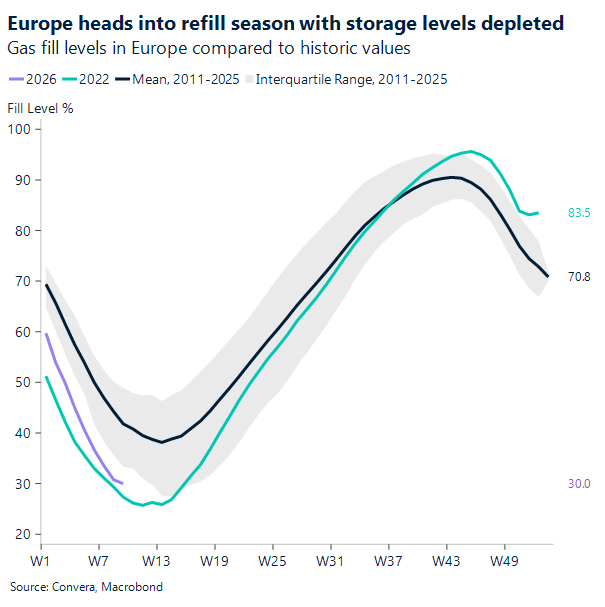

European natural gas volatility has exploded, with front‑month Dutch TTF futures up more than 80% since Friday and 30‑day realised volatility pushing toward 150% — the highest since the 2022 crisis. The halt at Qatar’s LNG facility has amplified fears of a broader supply disruption just as Europe heads into the refill season with storage levels depleted and summer contracts already trading above winter.

This energy backdrop is feeding directly into the euro’s decline. A supply‑driven shock is the worst‑case scenario for Europe’s terms of trade, and the latest inflation data only compounds the problem. Euro‑area CPI surprised to the upside in February, with headline inflation rising to 1.9% and core and services measures also accelerating. German two‑year yields jumped as traders quickly rebuilt expectations for a late‑2026 ECB rate hike, now pricing roughly a 50% chance of tightening by year‑end.

Against this backdrop, the euro is struggling on multiple fronts. Risk‑off flows triggered by the latest Iran headlines are reviving the dollar’s haven appeal, but it’s the risk of a terms of trade shock that really punishing the single currency. The US, as a net energy exporter, is comparatively insulated — whilst Europe absorbs the import bill.

With energy volatility surging and inflation risks re‑emerging, a move below $1.15 in EUR/USD looks increasingly plausible.

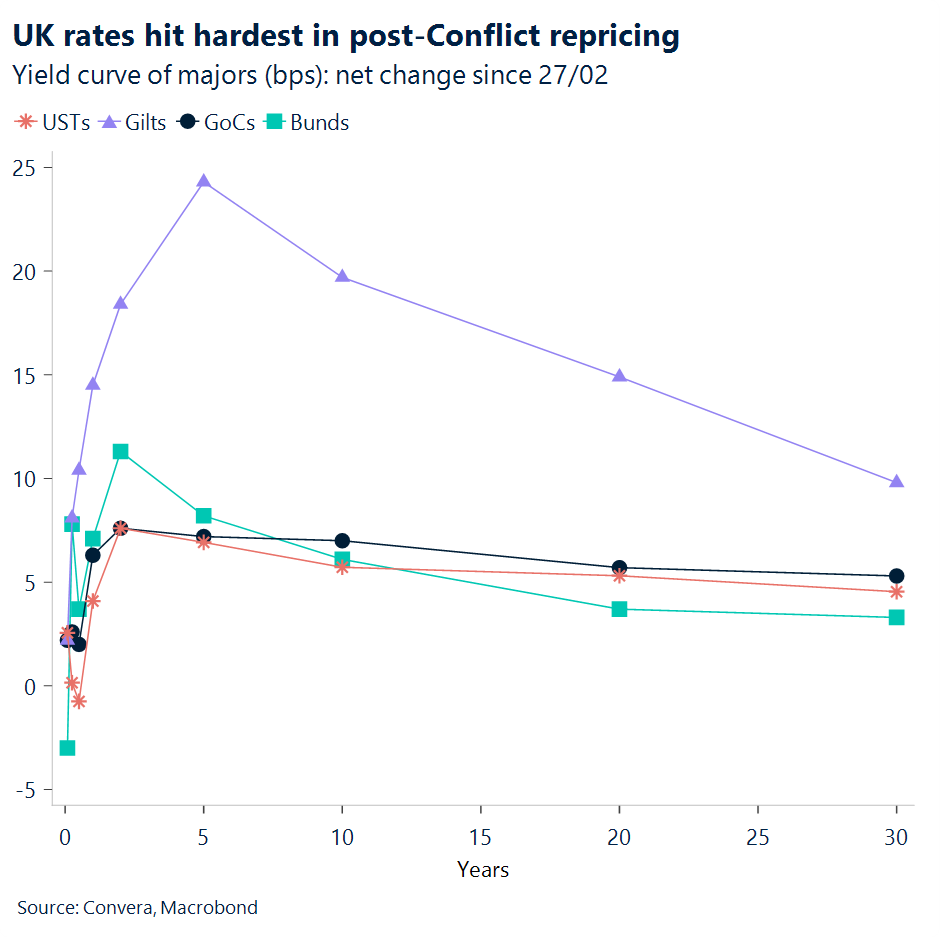

GBP: Middle East shock exposes UK fragilities

Sterling extended its losses yesterday as the conflict in the Middle East shows no signs of easing, keeping geopolitical risk elevated. Domestically, the Spring Budget delivered updated OBR forecasts but no policy changes. The OBR now projects UK growth of 1.1% in 2026 (previously 1.4%), 1.6% in 2027 (previously 1.5%), and 1.6% in 2028 (previously 1.5%), with 2029 and 2030 unchanged at 1.5%. The downgrade to 2026 is partly offset by a slightly firmer medium‑term outlook.

That said, the conflict in the Middle East may pose a clear near‑term risk if sustained. And while it is too early to assess whether it will translate into a material downside risk for the economy, the UK specifically warrants attention given its vulnerable political and economic backdrop. Higher oil prices could weigh further on 2026 growth while pushing inflation higher. This would reduce tax revenues and raise government borrowing costs through higher risk premia. The improved fiscal headroom announced yesterday – £23.6bn (vs £21.7bn in November) – may therefore mean little, as it was finalised before the latest escalation in the Middle East. Fiscal slippage remains a concern, particularly against entrenched uncertainty that predates the conflict, including the risk of a shift in political leadership that replaces Starmer with a more spendthrift alternative.

In response, the conflict exposes and reinforces existing UK vulnerabilities, exerting compounded pressure on government bonds and the currency. It follows that even if the BoE were to turn more hawkish on the back of a higher inflation outlook – since Friday 27 February, markets have scaled back expectations of BoE easing by December from more than two 25 bps cuts to just about one – the domestic setup would likely blunt meaningful GBP support. Rates markets clearly capture the UK’s increasingly fragile backdrop, with gilt yields across maturities rising the most as risk premia proliferate more aggressively relative to peers.

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

Calendar: March 02-06

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.