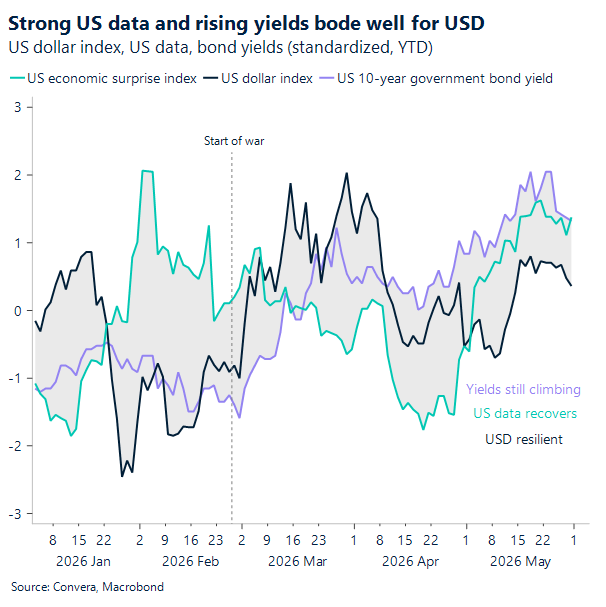

USD: Dollar holds ground amid noise

The USD narrative in May evolved from a tactical, headline‑driven story into a more structurally supported one. Early in the month, the dollar tracked geopolitical swings and oil price volatility, remaining choppy but range‑bound. Episodes such as yen intervention introduced intermittent downside pressure, but failed to alter the underlying tone.

By mid‑May, focus shifted toward macro fundamentals. Firmer inflation data and rising yields provided a more durable anchor, reinforced by a credibly hawkish Fed stance. As a result, the dollar became less reactive to short‑term de‑escalation headlines. Into late May, the USD stabilised even as volatility declined, supported by higher real yields, resilient US activity, and relative insulation from the energy shock.

June begins with a familiar tension. Progress toward a US–Iran ceasefire remains elusive and efforts to reopen the Strait of Hormuz are still stalled, pushing oil prices higher. At the same time, equities remain buoyant, driven by continued momentum in the AI trade. The dollar sits between these opposing forces – supported by energy and rates, but capped by firm risk sentiment.

Attention now turns to the US May employment report and ISM surveys. Recent data have remained resilient, but early signs of softer employment momentum and rising input costs suggest a more fragile underlying backdrop. If the Hormuz impasse persists, the balance risks a more sustained shift toward inflation pressure – a dynamic that continues to favour USD support.

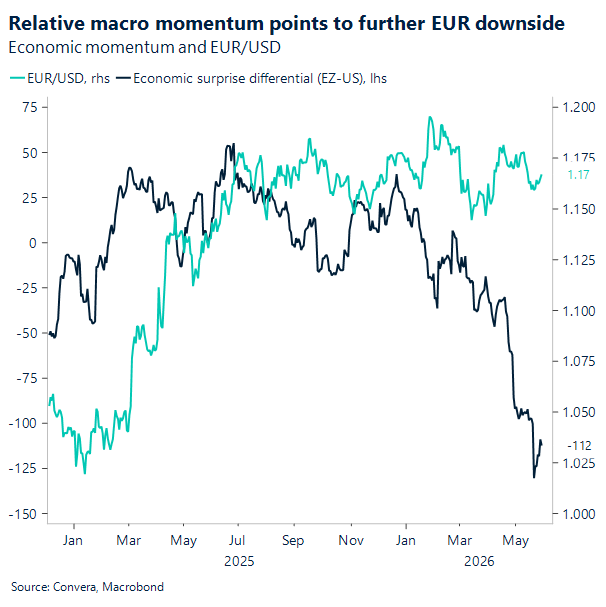

EUR: Sideways into June

EUR/USD continues to hover around the 1.16 level, lacking the conviction to move materially higher as markets remain unconvinced that a US–Iran resolution is imminent. At the same time, sentiment has not deteriorated enough to trigger a breakdown, leaving the pair anchored in a narrow, low‑conviction range.

The broader move over May was modestly negative, with EUR/USD down around 1% from the early‑month highs near 1.18. This drift lower reflects a rebalancing in rate expectations. Earlier, the euro had been supported by relatively aggressive ECB pricing, but that bias has softened. Markets now price roughly 52bp of ECB tightening by year‑end, while expectations for the Fed have edged higher to around 16bp, narrowing the relative advantage that had previously supported the euro.

This shift has slowed price action. With rate differentials stabilising and geopolitical uncertainty unresolved, EUR/USD has settled into a holding pattern rather than extending in either direction.

Looking ahead, the near‑term risks are skewed slightly lower. In the absence of meaningful progress on the Strait of Hormuz, ongoing energy uncertainty continues to weigh on the Eurozone outlook, while incoming US data remains comparatively resilient. A sustained break below 1.16 therefore looks increasingly plausible if the current geopolitical stalemate persists.

This sets the tone heading into June. Oil prices remain firm, reflecting ongoing supply risks, while global equities continue to hold up, maintaining a broadly constructive risk backdrop. The combination is keeping EUR/USD range‑bound, with neither a clear bullish nor bearish catalyst yet in place.

Attention now turns to Eurozone inflation data this week, the final key input ahead of the ECB’s 11 June meeting, which will help determine whether current rate expectations remain sustainable.

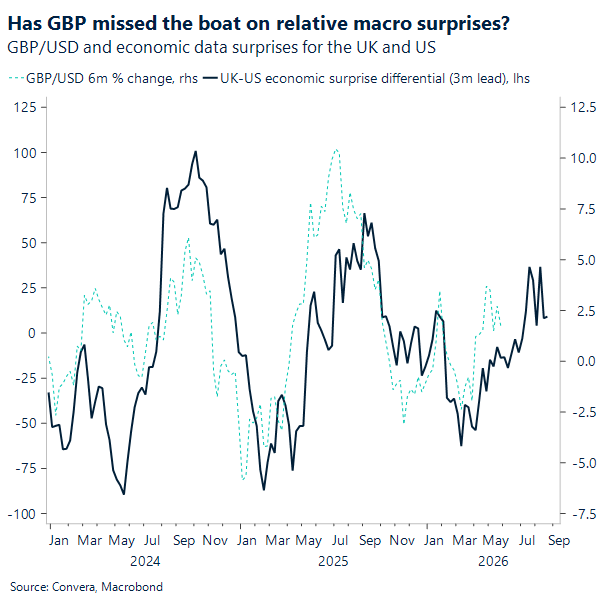

GBP: A miserable May for sterling

Sterling underperformed in May, falling over 1% against the dollar, making it the weakest G10 currency on the month. That said, GBP/USD recovered roughly half of its earlier losses, rebounding from 1.33 to the upper‑1.34s and reclaiming its 200‑day moving average, suggesting some stabilisation in near‑term momentum. Against the euro, gains remain constrained, with 1.16 continuing to cap upside – a level that also aligns with its post‑Brexit average.

The core issue for GBP is a lack of a clear domestic driver. As such, the currency remains heavily exposed to USD dynamics and global risk sentiment, but in an asymmetric way: it has recently failed to fully participate in risk‑on moves, yet still underperforms when sentiment deteriorates. This leaves the bias fragile rather than outright bearish, though downside risks are building. In particular, sterling may have already missed the window to capitalise on earlier positive data surprises, with May’s softer economic prints now pointing to a more challenging backdrop.

Political risk also lingers. Upcoming by‑election developments, particularly a potential Andy Burnham victory and renewed leadership contest, could reintroduce a fiscal risk premium and weigh on GBP.

Options markets reinforce this caution. Risk reversals remain skewed toward GBP downside, indicating persistent demand for protection against depreciation. This reflects concerns around political uncertainty, fiscal credibility, and a softening growth outlook, with GBP’s pro‑cyclical nature amplifying sensitivity to adverse shocks while capping upside potential.

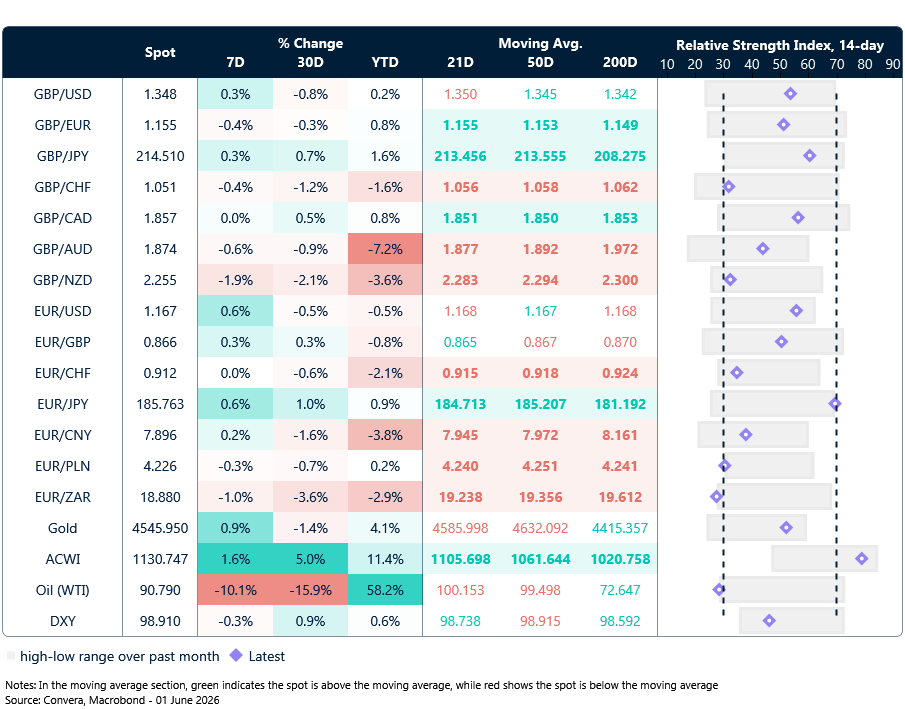

Market snapshot

Table: Currency trends, trading ranges & technical indicators

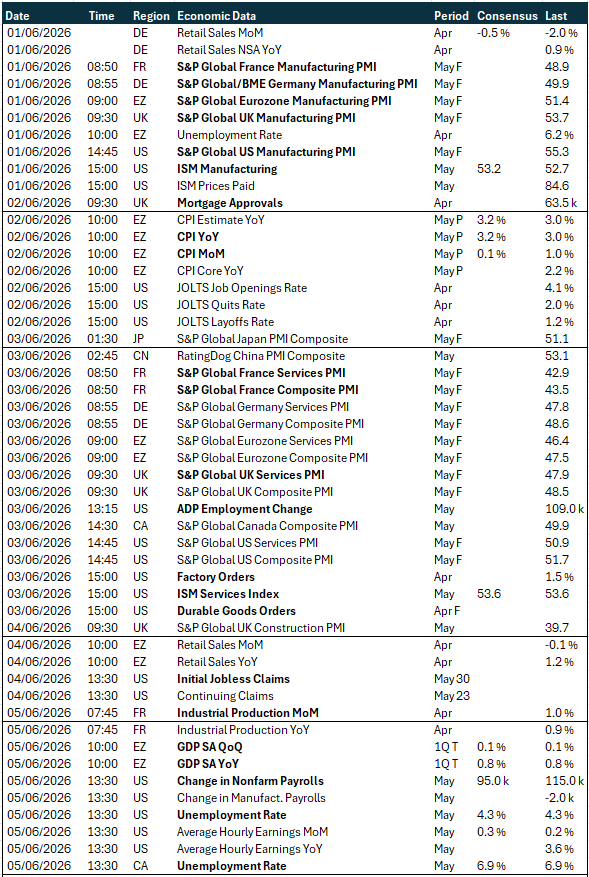

Key global risk events

Calendar: June 1-5

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.