Buckle up for payrolls

The US dollar slipped alongside two-year yields after fresh US economic data painted a mixed picture, but losses were pared following the news that China’s President Xi Jinping and US President Donald Trump have agreed to start a new round of trade negotiations as soon as possible. But the relief was brief. Global risk sentiment then took a knock later in the day as President Trump and Elon Musk traded blows over X, with Tesla’s share price plunging 14%, dragging on US equity indices.

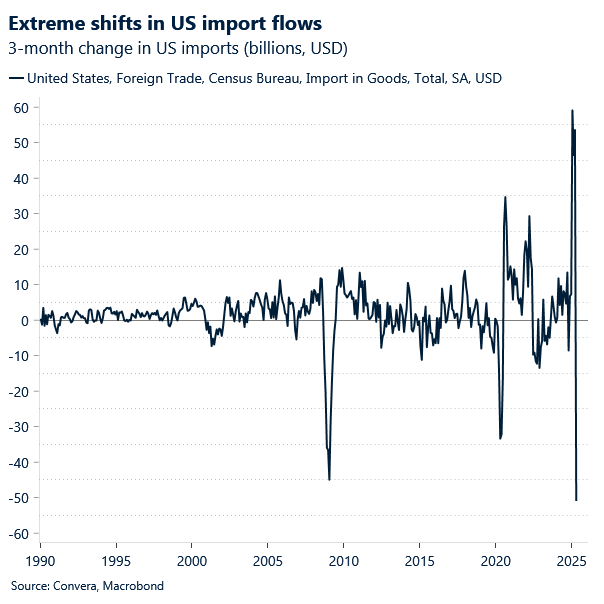

On the data front, the US trade deficit fell 55% in April, on the largest-ever plunge in imports, as companies stopped massive front-loading of goods. The retreat reflects the abrupt hit to trade, after firms had rushed products into the country earlier this year to try to get ahead of new taxes on imports Trump had promised. Shifts in US import flows have already outstripped the pandemic and look unlikely to return to normal before tariff levels reach a new equilibrium.

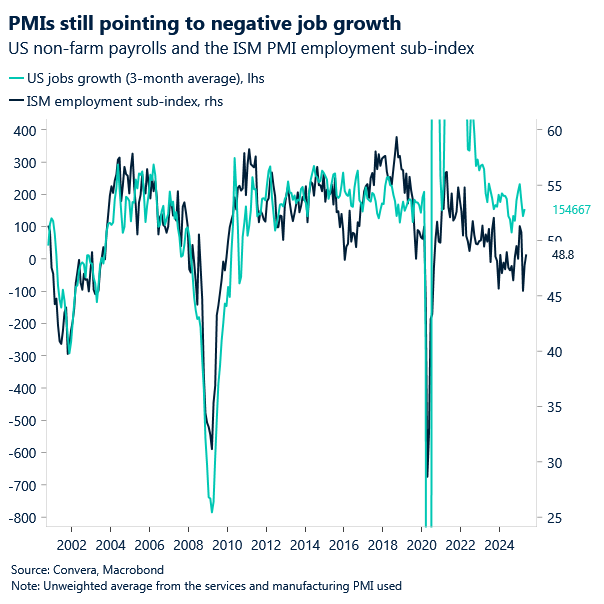

Meanwhile, higher-than-expected jobless claims signals cracks in the labour market, but rising unit labour costs and weaker productivity point to lingering inflation pressures. The challenge for policymakers is evident: navigating slower growth while inflation risks persist, a combination that complicates the Federal Reserve’s (Fed) rate stance. The next big test for the dollar is today’s US jobs report, which will be closely watched, especially for signs of Liberation Day’s impact on hiring and whether DOGE spending cuts are starting to weigh on federal employment. Markets expect the US created 126K jobs during May and the unemployment rate to have stayed at 4.2%. Recent employment components of survey data suggest May was a weak month though, with tariff-related uncertainty weighing on hiring decisions. If we get a softer than expected print today, this should be dollar negative and might send the dollar index back towards 3-year lows.

FX markets are adjusting to softer US prints, and as clarity on policy emerges, the dollar’s trajectory will become more defined. Yet, the broader concern remains: trust in the dollar as a global reserve currency continues to erode, reinforcing its position as the core of the ‘Sell America’ trade. Unless stronger trade agreements materialize, skepticism toward the dollar is likely to persist, keeping upside potential limited.

Even with the trade war taking a backseat recently though, dollar sentiment remains shaky, as attention has also shifted to President Trump’s tax bill. The Congressional Budget Office now projects it will add $2.4 trillion to the deficit over the next decade, a factor that could weigh on long-term dollar stability too.

Canadian exports take a hit, trade deficit soars

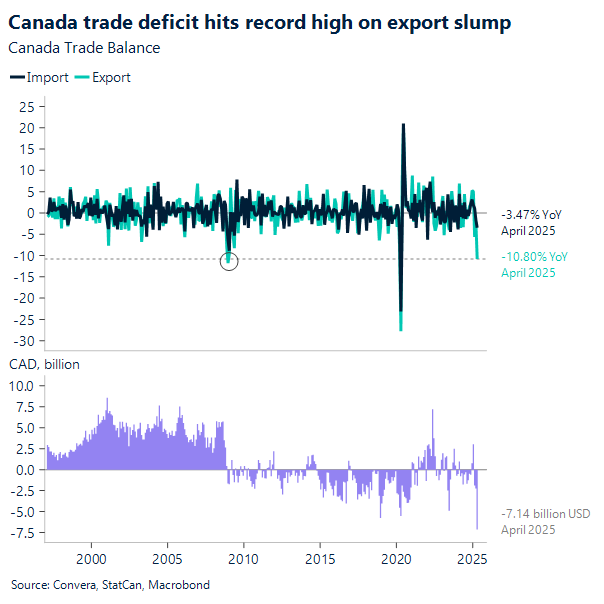

Canadian exports took a steep dive in April, plunging 10.8%, the biggest drop since December 2008, as demand from the U.S. collapsed due to tariffs. The country’s trade deficit ballooned to a record C$7.1 billion, far exceeding even the most pessimistic forecasts. Exports to the U.S. were hit hardest, sinking 15.7%, while sales to other countries saw a modest 2.9% uptick.

Imports weren’t spared either, slipping 3.5% to CAD 67.6 billion. The biggest losses came from motor vehicles and parts (-17.7%), industrial machinery (-9.5%), consumer goods (-4.2%), and electronic equipment (-5.5%). Imports from the U.S. dropped 10.8%, reinforcing the pressure on cross-border trade.

Canada’s export volumes could stay sluggish for the rest of the year unless there’s a meaningful shift in U.S. trade policy. For now, the data paints a challenging picture for economic growth, with lingering uncertainty weighing on business confidence.

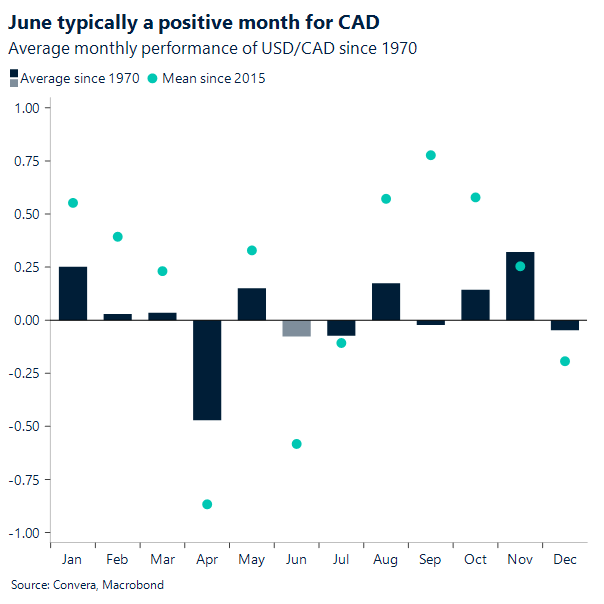

Slow grind lower

The Canadian dollar has reached a fresh 2025 low of 1.3635 amid continued U.S. dollar softness. Opening June with a high of 1.3746 and a low of 1.3635, the CAD has struggled to hold below 1.365 for long. The gradual and slow decline has pushed it beneath its 100-week SMA at 1.3763 over the past two weeks, signaling persistent downward pressure. On a daily scale, the CAD is edging toward oversold territory, as indicated by the Relative Strength Index (RSI), suggesting a potential rebound, especially if the U.S. dollar strengthens. Meanwhile, the 20-, 40-, and now 60-day SMAs have all crossed below the 200-day SMA, establishing firm resistance at the 1.377 level. To the downside, 1.36 remains the next key support, marking a crucial threshold for further movement.

Hawkish surprise lifts the Euro

ECB President Christine Lagarde delivered unexpectedly hawkish remarks during yesterday’s press conference, despite cutting the deposit rate to 2%, in line with market expectations. In response, the euro surged nearly 1% against the dollar, flirting with $1.15 at $1.1495, while German two-year yields climbed to a two-week peak. Lagarde stated that policymakers are approaching the end of the monetary policy cycle, as the current rate is deemed appropriate for navigating ongoing economic uncertainty. She also did not rule out upward revisions to growth projections, also emphasizing that the 25-basis-point cut was not unanimous. While trade uncertainty may weigh on business investment and exports, Lagarde pointed to government spending on defense and infrastructure as potential growth drivers in the future. Shortly after, money markets trimmed expectations for further rate cuts this year, no longer fully pricing another ECB reduction by year-end.

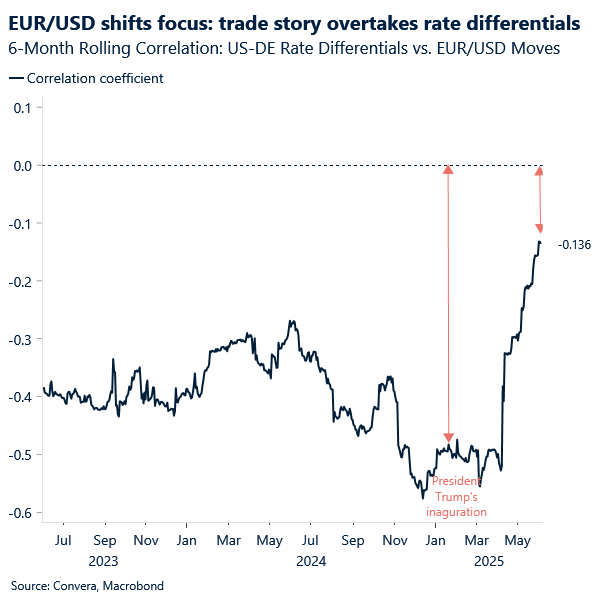

However, the euro’s rally wasn’t solely driven by Lagarde’s speech. In fact, the correlation between EUR/USD and the spread between two-year US-German yields has weakened to its lowest level in more than two years, underscoring that trade developments—rather than interest rate differentials—have been the primary driver of FX movements recently. Instead, an unexpected jump in US jobless claims, released around the same time as Lagarde’s speech, quietly contributed to EUR/USD’s surge. The data reinforced expectations that the Fed may cut rates at least twice this year, further stoking concerns over tariffs and economic uncertainty—adding to the dollar’s challenges.

Although EUR/USD lost some momentum as the session progressed, a softer-than-expected NFP report today could see the pair ending the week comfortably within the $1.14 range.

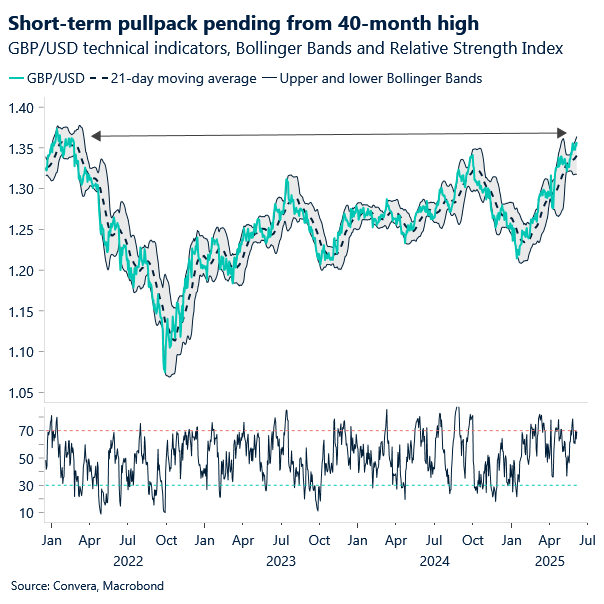

Pound notches 40-month high

The pound briefly spiked to its highest level since February 2022, finally breaking through the $1.36 resistance barrier – a level GBP/USD has only been above for 14% of the post-Brexit period. The move was triggered by a string of weak US data, which puts the US jobs report in focus today. A weaker print could jolt the pound back above this threshold whilst a stronger print could drag it back towards $1.35.

As we’ve highlighted for several weeks, beyond dollar dynamics, GBP sentiment has notably improved thanks to strong domestic economic data, UK trade agreements, and the BoE’s relatively hawkish stance. These factors reinforce sterling’s idiosyncratic strength, making its rally more than just a dollar story. However, given the pound is approaching overbought conditions via the 14-day relative strength index, the upside potential in the short-term could be limited in scope. Traders are also trimming their expectations on further gains in the British pound, according to options-market pricing, with one-month risk reversals edging lower for a third day running.

Meanwhile, versus the euro, sterling is struggling to reclaim the €1.19 handle this week, near which lie both the 21-day and 100-day moving averages. GBP/EUR continues to trade in sideways pattern since mid May, though real rate differentials suggest the pair should be trading closer to €1.20 given the divergence between ECB and BoE policy expectations.

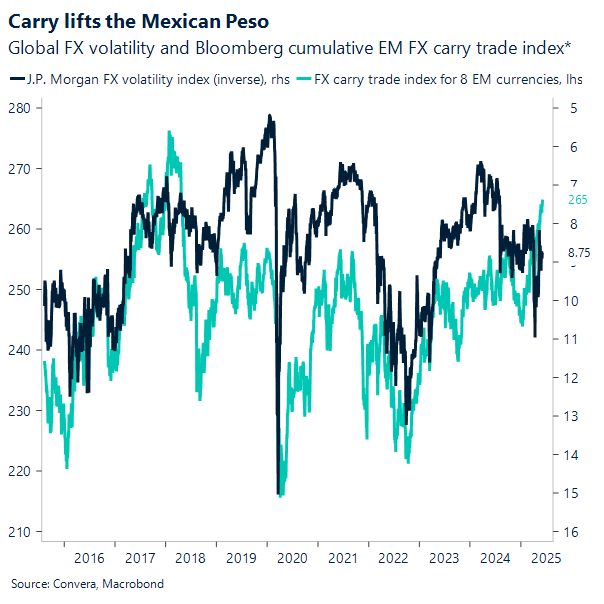

Peso lifted by EM carry

The Mexican peso has gained this week, riding the wave of low volatility and renewed enthusiasm for emerging market and Latin American carry trades. Investors are diving back into the strategy, fueled by easing trade tensions and momentum from TACO. With traders borrowing in low-yield currencies to invest in higher-yielding emerging markets, stability remains critical—any sudden shifts, especially from Trump, could disrupt the trend. A global currency volatility measure recently dropped to 8.9%, lifting Bloomberg’s EM carry trade index to a seven-year high. Meanwhile, moderating inflation is making EM bonds more appealing, with currencies like the Brazilian real and Turkish lira standing out. Asset managers have also ramped up bets on EM currencies, with positions in Mexico’s peso hitting a nine-month high.

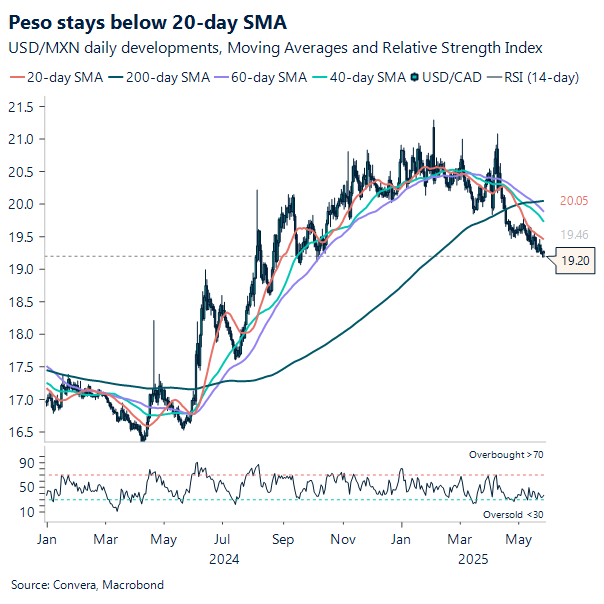

The peso has gained 0.8% this week against the U.S. dollar, bringing its year-to-date appreciation to 8.7%. It reached a high of 19.44 and a low of 19.12, its lowest level year-to-date and the weakest in eight months, as it gradually nears the 200-week SMA at 19.04. Since April, the 20-day SMA has remained a moving resistance level, presenting opportunities for USD sell-offs during upward rebounds.

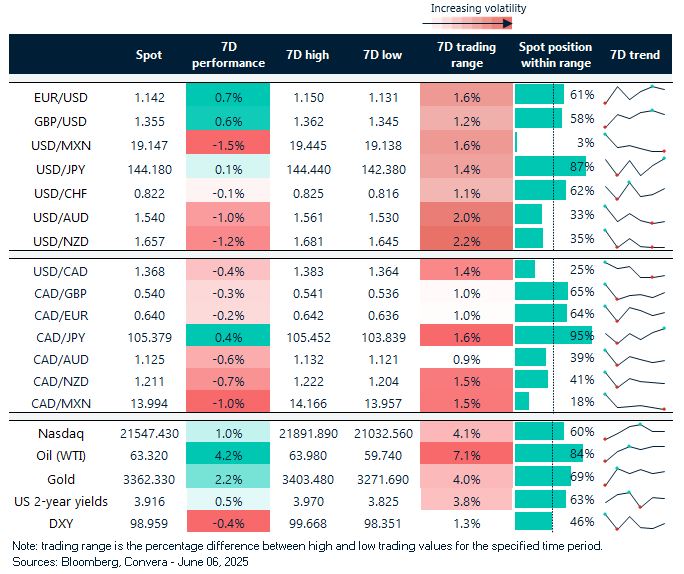

Dollar index holds near lower third of 7-day range

Table: 7-day currency trends and trading ranges

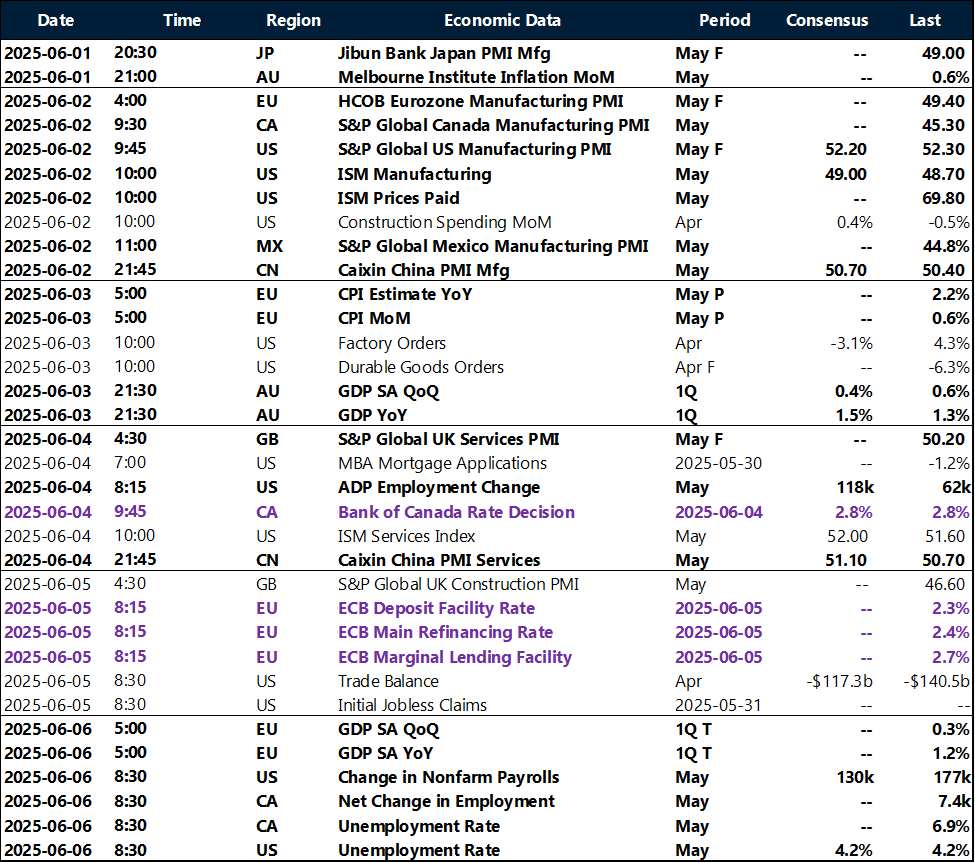

Key global risk events

Calendar: June 2-6

All times are in ET

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.