USD: Iran, OPEC, AI and the Fed: everything in play

Global markets are navigating a complex mix of geopolitical risk, shifting energy supply dynamics, technology‑sector volatility, and an imminent Federal Reserve meeting. Together, these forces are shaping a more uneven risk environment and reinforcing a USD narrative that is increasingly conditional rather than directional.

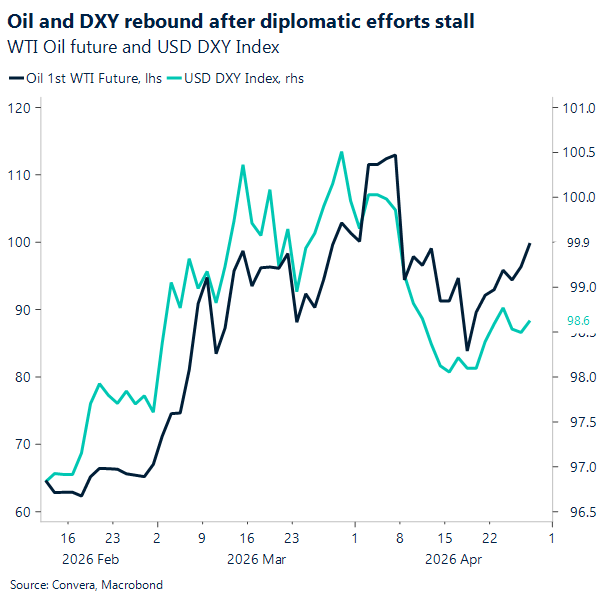

1) US–Iran stalemate puts energy risk back in play

The ceasefire between the US and Iran has reduced immediate tail risks but failed to deliver clarity on duration or follow‑through. Headline volatility has returned as negotiations remain stalled and the Strait of Hormuz stays effectively closed, keeping oil supply risks elevated. Brent climbed toward $111 amid concerns that a protracted peace process could prolong disruptions through a waterway that handles roughly a fifth of global oil flows. President Trump confirmed Iran has sought relief from the US naval blockade while talks continue, but the lack of tangible progress has reversed some of the relief seen earlier in oil and the dollar. For the USD, higher energy prices reintroduce an inflation buffer and a modest terms‑of‑trade floor, particularly against energy‑importing currencies.

2) UAE’s OPEC exit complicates the oil outlook

Overlaying the geopolitical shock is a structural shift in energy markets. The UAE’s decision to exit OPEC on May 1 removes one of the group’s most flexible producers and signals a willingness to add supply independently over time. As a result, crude is being pulled in opposite directions – near‑term scarcity from Hormuz versus longer‑term supply loosening from Abu Dhabi. That tension caps oil upside beyond immediate disruption headlines and limits how far the USD can lean into energy‑driven strength.

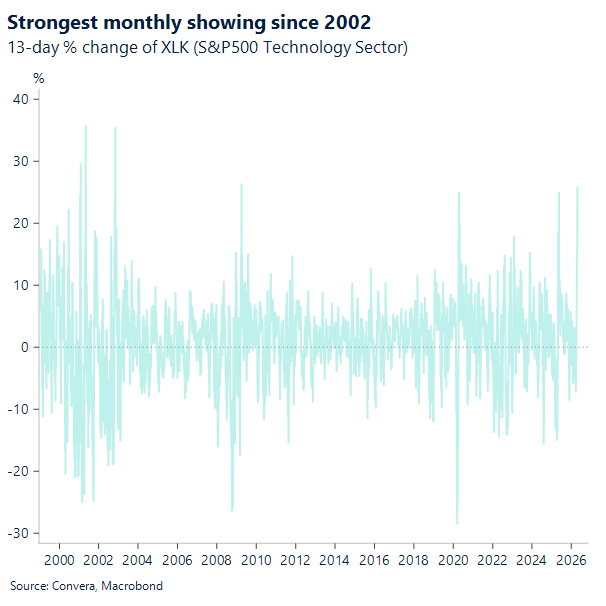

3) AI jitters dent risk sentiment

Risk appetite softened after reports that OpenAI missed sales and user targets, triggering a pullback in AI‑linked equities that have driven much of the recent rally. The S&P 500 tech sector remains up 17% this month, its strongest showing since 2002, but Tuesday’s pause highlights the need for caution.

4) Fed meeting anchors USD expectations

With no rate change expected today, attention turns to how the Fed frames risks. Officials previously flagged rising inflation risks and weaker growth prospects tied to the Iran conflict. While hostilities have eased, sustained energy disruption complicates the policy outlook. Our base case still sees two Fed cuts this year, but their timing is increasingly pushed back — a dynamic that continues to support the USD at the margin, even as upside remains capped.

Briefly on the macro front – US Conference Board consumer confidence rose again to its highest level of the year, reinforcing the resilient‑consumer narrative and helping limit USD downside amid a relatively constructive US macro backdrop.

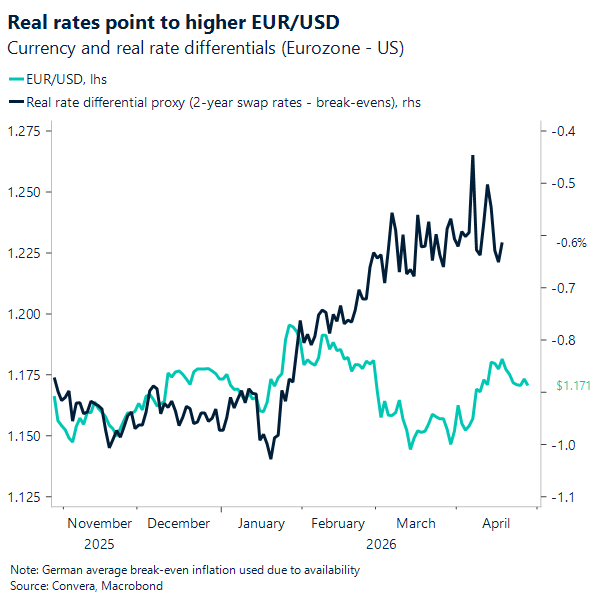

EUR: Supported but still lacking conviction

EUR/USD remains reasonably well supported above key moving averages, though the pair has struggled to break decisively above 1.18 of late as markets weigh resilient risk appetite against a still-unsettled geopolitical and rates backdrop.

The dollar’s war premium has faded as investors lean towards a more constructive outcome in the Gulf, and that has helped keep the euro underpinned. However, the move has not yet developed into a clean bullish EUR/USD breakout, with markets still lacking the conviction to push the pair sustainably beyond recent highs. The main reason is that higher oil prices and elevated global yields are still clouding the near-term outlook. While softer USD sentiment has offered support, the broader macro backdrop remains mixed. Any renewed rise in energy prices risks reinforcing stagflation concerns and limiting the scope for a more aggressive move higher in EUR/USD, particularly if the Federal Reserve maintains a cautious tone and signals that rates may need to remain restrictive for longer.

At the same time, the euro has found support from firm global equities and relatively constructive rate differentials, which are helping offset some of the negative terms-of-trade pressure from higher energy costs. In that sense, EUR/USD is continuing to trade more as a function of broader risk sentiment than as a pure oil or rate story.

Looking ahead, the ECB is the key event risk on the euro side. Markets have turned somewhat more hawkish on the rates outlook in recent sessions, and that leaves the single currency vulnerable if the Governing Council fails to validate those expectations. For now, EUR/USD still looks supported on dips, but without a fresh macro catalyst, upside momentum may remain gradual rather than explosive.

GBP: BoE hawkishness felt more keenly

Risk sentiment briefly shifted its dominant driver yesterday, away from the conflict and toward renewed concerns around AI spending, following reports that OpenAI missed internal sales targets. Sterling strengthened against high‑beta G10 currencies, which are more sensitive to the broader risk mood, but remained broadly flat versus the euro. We note that, when war headlines sour, GBP has tended to outperform EUR, with the latter more exposed to imported energy and therefore more vulnerable to conflict‑driven anxiety.

Meanwhile, GBP/USD remains highly sensitive to geopolitical developments, with markets awaiting clarity on the US response to Iran’s proposed interim deal – reopening the strait in exchange for a lifting of the US naval blockade, while deferring more complex negotiations on Iran’s nuclear programme. The initial proposal reportedly appeared unsatisfactory to President Trump, though Pakistani mediators suggest Iran may submit a revised offer in the coming days. In this context, we see scope for GBP/USD to retest mid‑April highs around 1.36 should the proposal be accepted.

For GBP/EUR, relative BoE–ECB messaging at tomorrow’s policy meetings is likely to be felt more acutely. We retain an upside bias, expecting the BoE’s hawkish tone to stand out more clearly. The BoE has already been reluctant to signal further easing amid still‑elevated inflation for quite some time now, and last week’s run of firmer macro data may offer tentative – albeit fragile – validation for a more hawkish posture tomorrow, lending support to sterling. A break above 1.1550 is our base case this week.

That said, expectations for “tough talk” from central banks are now widespread and largely priced in. As a result, more latent signals – such as revisions to the BoE’s economic projections or the vote split – may matter more than rhetoric alone (the Fed and ECB do not publish updated projections this week). Investors will closely scrutinise any revisions that skew more heavily toward downside growth risks or upside inflation risks, as well as the vote split – expected at 8–1 in favour of a hold, with one dissenter favouring a hike – which could imply a more dovish (9–0) or hawkish (2–7) tilt. We see these factors as potential amplifiers or dampeners of sterling’s support derived from broader hawkish messaging by officials.

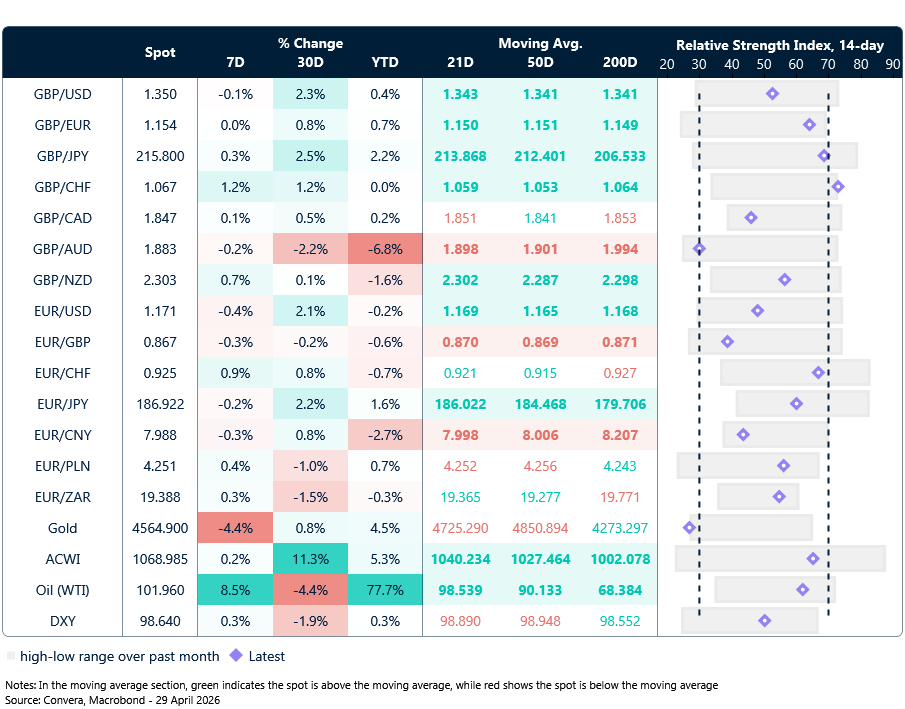

Market snapshot

Table: Currency trends, trading ranges & technical indicators

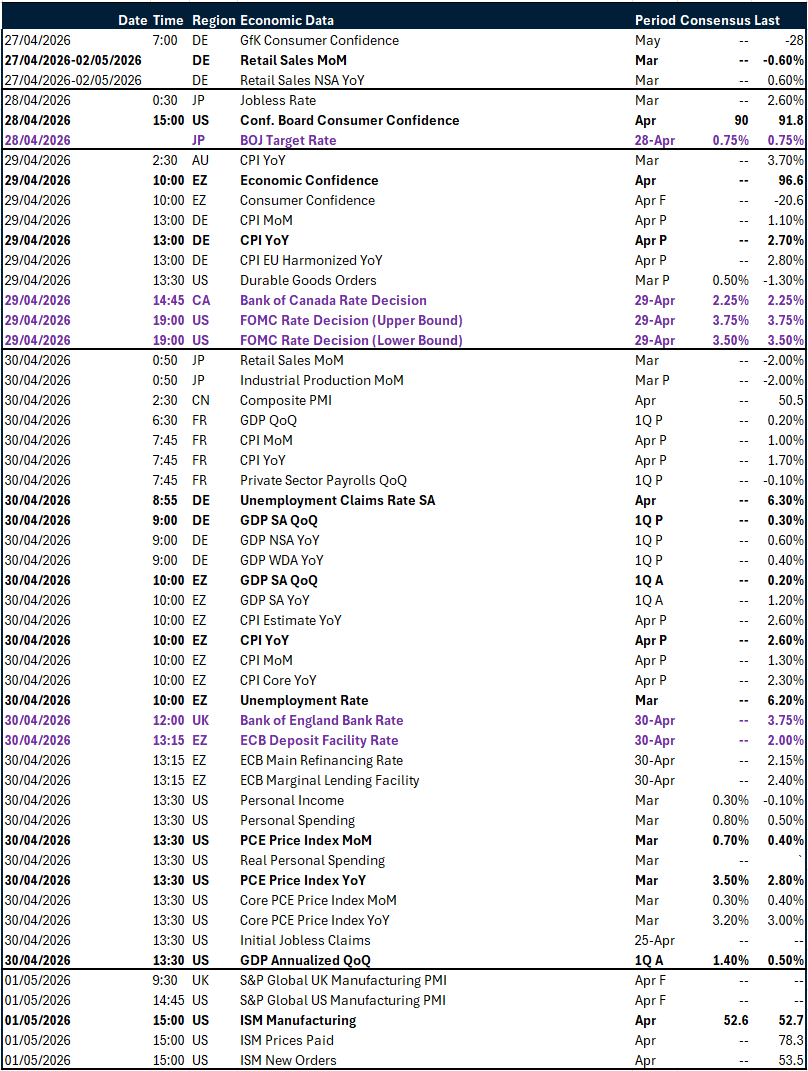

Key global risk events

Calendar: April 27 – May 1

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.