The Daily Market Update will take a break over the holiday period. Our final edition will be published on 19 December 2025, and the report will return on 5 January 2026. Our offices will remain open as usual but will observe local public holidays. Contact your account representative for more information.

Dollar firms before CPI report

Markets are bracing for Thursday’s CPI release, with headline inflation projected at 3.1%. Any print slipping into the 2% range could spark a Treasury rally and weigh on the US dollar, as investors recalibrate expectations for the Fed’s policy path. A beat might support the dollar through reduced Fed easing bets, but would also reinforce stagflation fears – a key uncertainty amongst policymakers.

Treasury volatility has been grinding lower, with the ICE BofA MOVE Index sliding to its weakest level since early December and now testing the subdued ranges last seen in 2021. The calm reflects a market that sees questions around tariffs, the broader economic outlook, and the next Fed chair as issues for 2026 rather than immediate catalysts.

Mixed labor market signals earlier in the week did little to shift Fed expectations: markets continue to price at least one more cut in 2026. Fed Governor Waller suggested there is room to ease more given softer employment trends, but Atlanta Fed President Bostic struck a more cautious tone, saying he does not anticipate further reductions in borrowing costs next year.

A softer‑than‑expected CPI report could knock the dollar lower and ignite a bond rally, while any upside surprise would reinforce the Fed’s cautious stance and limit USD downside into year-end.

Hawkish BoE rate cut supports pound

As expected, the Bank of England cut rates by 25bps to 3.75% today, with the vote split at 5–4. We had warned that the bigger risk was not the cut itself, but that a narrow split would disappoint doves and leave scope for sterling to strengthen. With pessimism already embedded in GBP, stretched short positioning and sterling’s still‑attractive carry profile, the setup was ripe for markets to be caught off guard — and today’s post‑decision rally in the pound reflects exactly that dynamic.

Bottom line: The cut was no surprise, but markets latched onto signs of a resilient hawkish contingent on the MPC, which has kept GBP buoyant, highlighting that the bigger story lies in positioning and market expectations rather than the headline decision..

ECB: steady rates, shifting expectations

The final ECB meeting of the year is expected to be uneventful, with policy left unchanged for a fourth consecutive time. Euro weakness could follow, however, if Isabel Schnabel proves to be a hawkish outlier and growth forecasts are revised only marginally higher.

Recent data have bolstered hawkish voices on the Governing Council, supporting steady policy and keeping the odds tilted toward higher rates rather than renewed easing. If President Lagarde’s messaging reinforces this repricing, EUR/USD could gain further support via rate differentials.

Attention will focus on updated projections. Growth is likely to be revised higher for 2026, with only minor changes to inflation, leaving the outlook broadly consistent with September’s baseline. What has shifted more meaningfully is market pricing: investors have moved from expecting modest cuts to now entertaining the possibility of a new hiking cycle — a shift that helped the euro briefly spike above $1.18 against the dollar.

Our fair‑value models show EUR/USD more balanced than earlier in the autumn, but for spot to hold comfortably in the $1.18 zone through year‑end, two conditions are likely required: weaker US data and confirmation of the ECB’s hawkish tilt.

Bottom line: The December meeting is unlikely to deliver policy fireworks. With dovish expectations already pared back, the greater risk lies in hawkish disappointment — leaving EUR/USD direction dependent on both US data surprises and the ECB’s tone.

Market snapshot

Table: Currency trends, trading ranges and technical indicators

Key global risk events

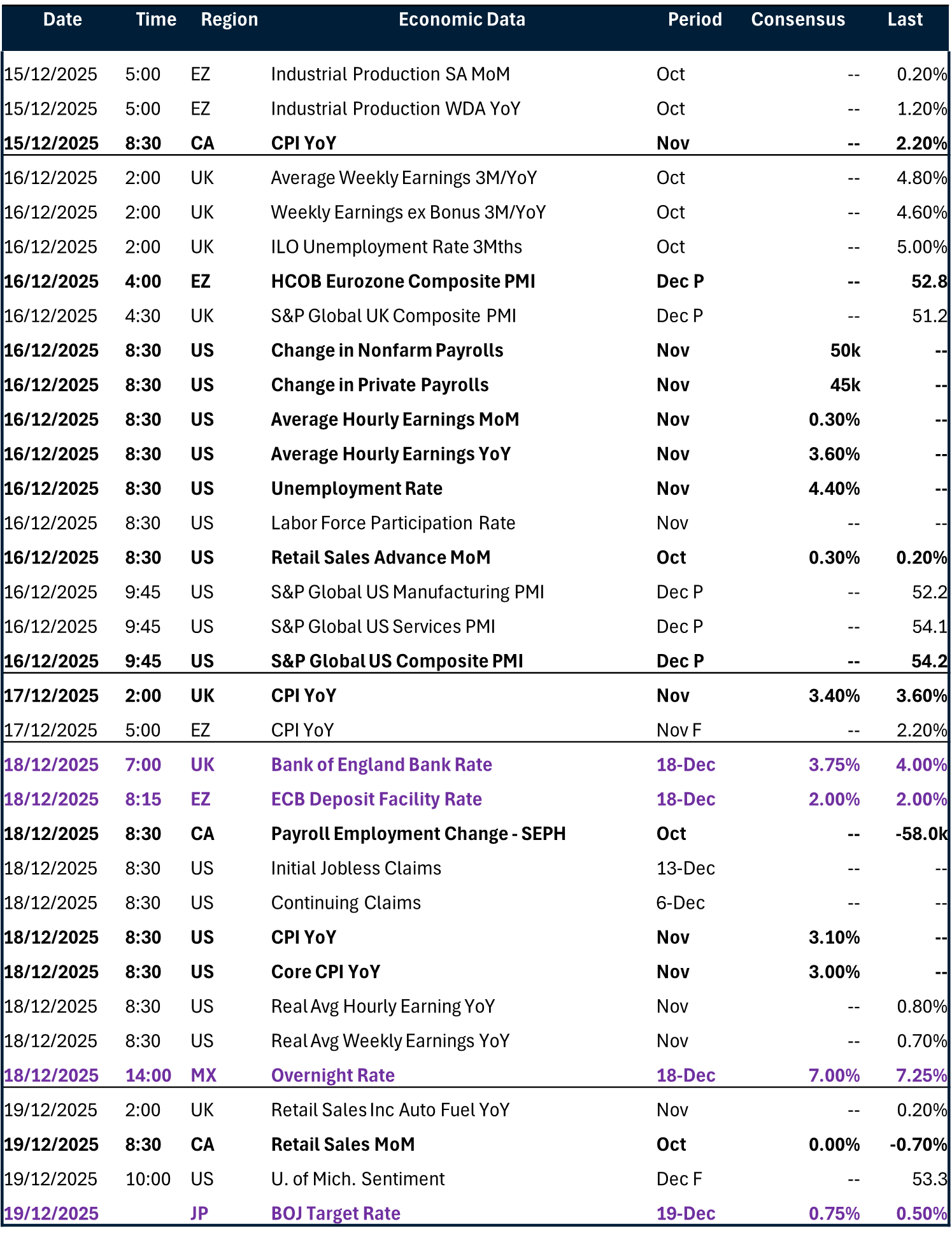

Calendar: December 15-19

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.