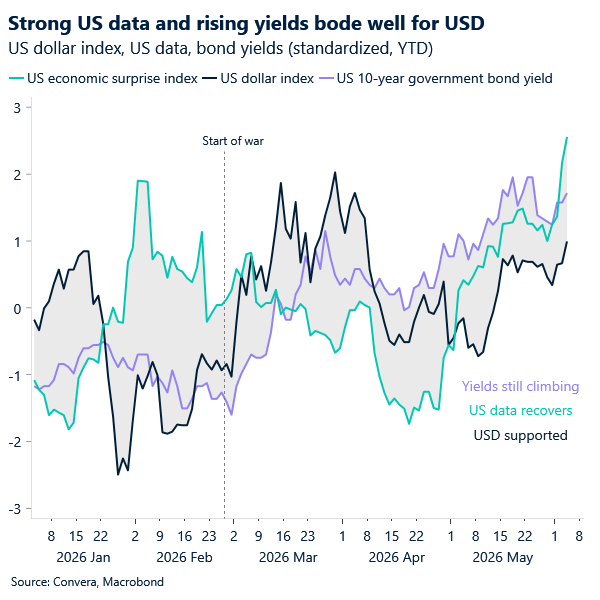

USD: Stronger dollar, conditional outlook

The US dollar remains modestly supported at the start of the week, underpinned by a renewed rise in oil – up more than 5% amid continued uncertainty around US–Iran negotiations, and firm US data.

The US economic surprise index has risen to its highest level since late 2023, while April JOLTS data showed job openings climbing to their strongest level since May 2024, earlier this week. This was accompanied by solid ADP figures (122k jobs added in May) yesterday, reinforcing the narrative of a labour market that remains resilient even as consumer finances appear stretched. ISM PMIs – both manufacturing and services – also exceeded expectations in May. Taken together, these indicators suggest the US economy may be re‑accelerating at the margin, providing a firmer macro anchor for the USD.

That said, the outlook is not one‑sided. While higher oil and relative growth strength support the dollar, this remains a conditional story. A credible de‑escalation in the Middle East would remove both the energy and safe‑haven pillars of USD strength. At the same time, renewed US policy uncertainty – particularly around trade/tariffs – or further yen‑driven USD weakness could generate broader spillovers across FX. For now, the USD remains supported, but increasingly reliant on the persistence of current macro and geopolitical conditions.

EUR: Trade and rates reinforce downside bias

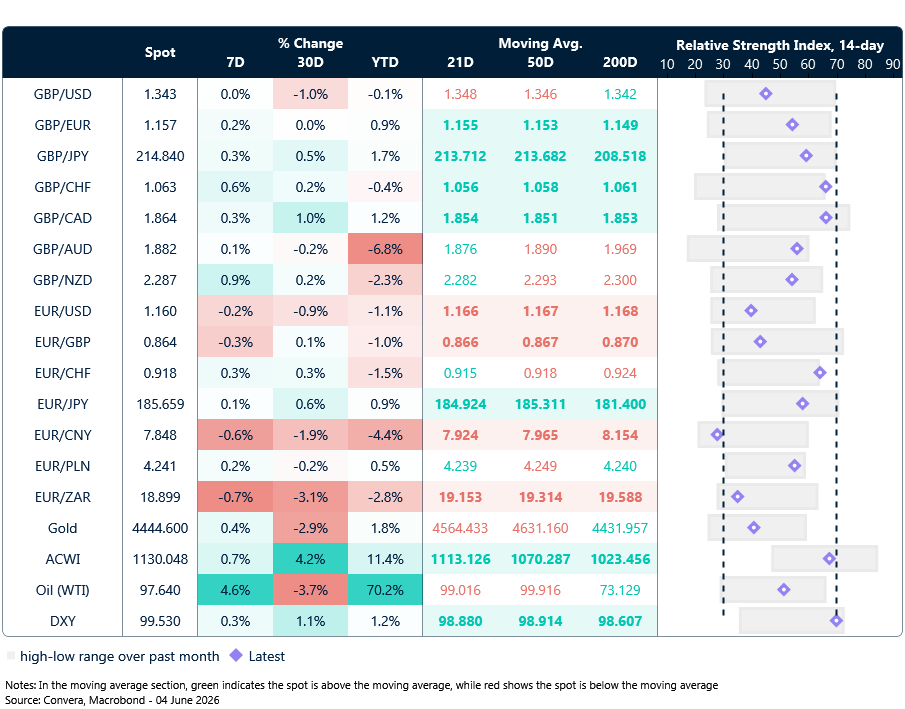

EUR/USD remains range‑bound near the 1.16 lows, trading below key moving averages and reflecting a market still lacking conviction. While month‑to‑date moves are limited, the underlying bias continues to tilt lower as geopolitical uncertainty persists, and rate differentials shift back in the dollar’s favour.

The latest US push toward broader tariffs adds another layer of pressure. A more protectionist backdrop is particularly challenging for Europe, given its dependence on external demand and imported energy. With exports to the US concentrated in sectors facing direct domestic competition, the risk is that trade frictions exacerbate an already fragile growth outlook – reinforcing the eurozone’s relative underperformance.

At the same time, the rate backdrop offers limited support. Despite inflation edging higher to 3.2%, markets already price in a near‑term ECB hike, largely as a signalling move. Beyond that, conviction fades. Weak macro data and rising stagflation risks make it difficult to sustain a more aggressive tightening narrative, suggesting euro yield support may have further to unwind.

In contrast, the US continues to exhibit stronger underlying momentum, with yields adjusting accordingly. This widening divergence leaves EUR/USD increasingly exposed, particularly if the Hormuz stalemate persists.

Bottom line: the euro remains trapped in a low‑conviction range, but with trade risks rising and rate support fading, the balance of risks continues to lean lower, with 1.16 vulnerable on renewed USD strength.

GBP: Sterling struggles for a clean hawkish narrative

GBP/USD edged lower yesterday, with most of the move driven by the USD. Conflicting signals out of the Middle East, coupled with recent escalation in the region, have pushed oil prices higher, up around 6% so far this week, with the dollar catching a bid. The pair appears modestly supported into today’s open following US reports that Israel and Lebanon have agreed to a ceasefire – a key condition from Iran for resuming peace talks with the US.

At the same time, solid macro releases out of the US strengthened the case for a more hawkish Federal Reserve outlook, adding further support to the greenback. Despite the political risk premium for the pound having eased, or at least paused for now, rate differentials have therefore shifted in the dollar’s favour since the start of the conflict in late February.

In fact, the clearest hawkish narrative can be built for the US rather than the UK. The latter’s softer macro backdrop and energy dependence make the case for hiking less straightforward. Compared to the energy crisis of 2022, the inflation starting point is lower, while the labour market is much softer. These factors help contain the extent to which inflation pressures may become more entrenched, reducing the case for further hikes.

While markets expect a steady hand from the BoE on 18 June, the number of officials voting for a hike will be worth noting. BoE members Megan Greene and potentially Catherine Mann look likely to join Huw Pill in advocating for higher interest rates. A higher number of votes for a hike may provide some support for sterling, though that support is more likely to come through GBP/EUR than GBP/USD. We see the ECB as delivering an insurance hike, but we do not expect much guidance on further tightening, providing muted backing for the euro.

GBP/USD found support at 1.3420 following yesterday’s softening, maintaining the tight range-bound pattern in place since mid-May. A more meaningful test to the downside would appear warranted should tomorrow’s US jobs report surprise to the upside.

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

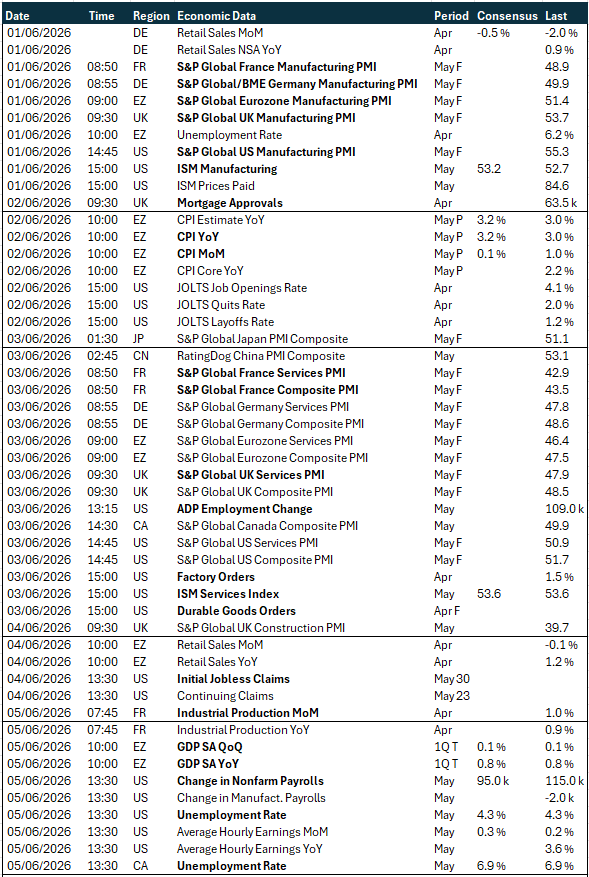

Calendar: June 1-5

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.