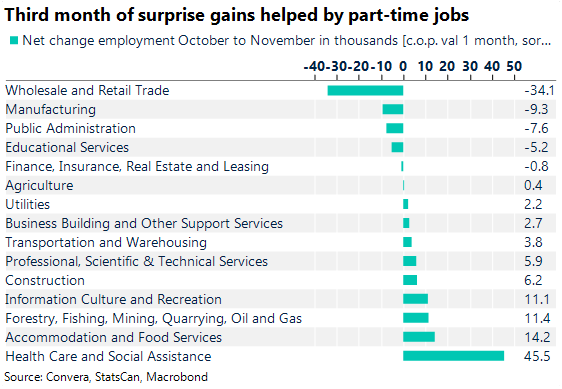

CAD: Part-Time shift drives job beat

The latest Canadian employment data for November 2025 delivered a stunning headline beat, with the economy adding 53,600 jobs against expectations of a 2,500 loss, but the underlying composition reveals a concerning trend for the second consecutive month. While the unemployment rate dropped to 6.5%, the growth was entirely driven by a surge in part-time positions, which jumped by 63,000, masking a contraction in the more vital full-time sector, which shed 9,400 jobs. This mirrors the previous month’s dynamic, where full-time employment fell by 18,500 while part-time work skyrocketed, suggesting that while the labour market remains resilient, employers are increasingly favoring flexible, lower-commitment hiring over permanent roles.

Despite the divergence in job quality, the sheer strength of the headline number triggered an immediate reaction in the currency markets, with the Canadian Dollar strengthening as the exchange rate moved lower to 1.39. Support near 1.388 should be found to end the week. This continued labour market tightness closes the deal for the Bank of Canada to keep interest rates stable in their next few meetings. With the economy still churning out jobs at a robust pace, policymakers are afforded the luxury of patience, allowing them to hold steady until they see more definitive progress on the inflation front before considering any dovish pivots.

USD: Dollar near 1-month lows

US and European equity futures advanced on Friday, with investors positioning ahead of the release of the Fed’s preferred inflation gauge. The US dollar index remains close to its weakest level since late October, as markets lean heavily into expectations of a Fed rate cut next week. Current pricing implies nearly a 90% probability of such a move, driven by mounting evidence of labour market weakness.

November’s Challenger survey showed layoffs rising over 71k, the highest for that month since 2022, pushing the year‑to‑date total to 1.1mln, the largest since 2020. This followed the ADP data earlier this week which showed a 32k decline in private payrolls, reinforcing concerns about slowing hiring momentum.

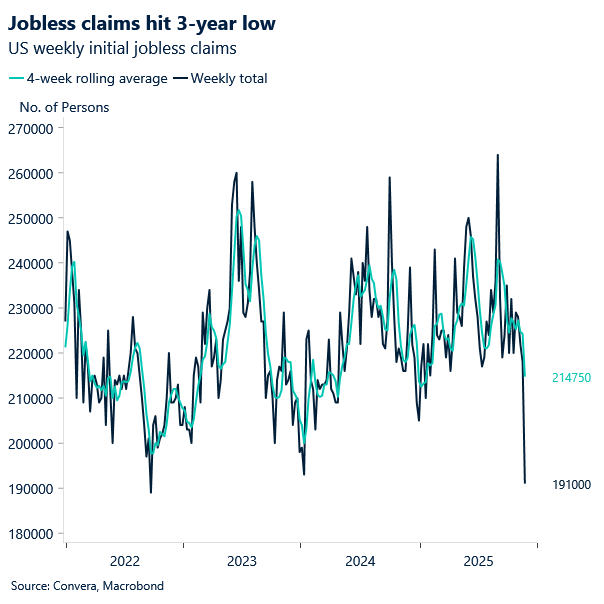

We did see initial jobless claims fell to 191k, the lowest in more than three years, though the Thanksgiving period likely distorted the figures. Even so, the four‑week average remains at its lowest this year. Investors appear to be discounting the claims data though, focusing instead on the broader trend of rising layoffs and weaker hiring intentions. That explains why the knee‑jerk reaction higher in US yields and the dollar quickly faded, with traders reverting to a dovish bias.

Still, we view the near‑90% probability of a December Fed cut as overstated given key data pieces are missing. The Fed may well deliver a cut, but packaged in hawkish messaging as seen in September and October. Such a move would temper expectations of aggressive easing and could ultimately prove dollar‑positive, especially if markets have over‑extended in pricing downside risks.

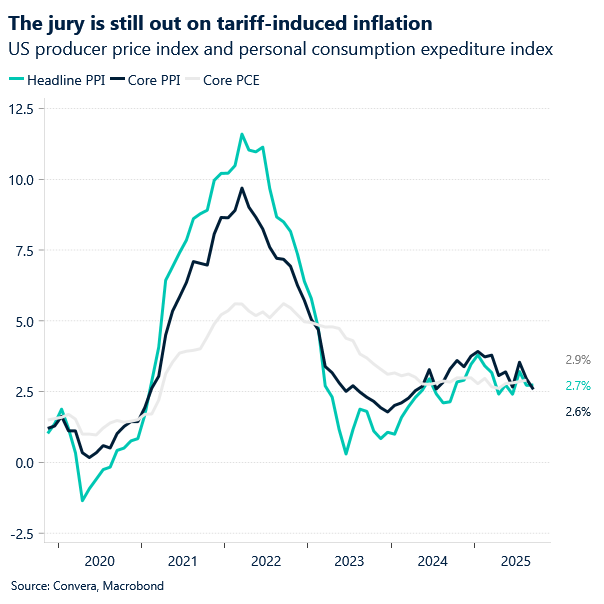

All eyes today are on the Fed’s preferred inflation gauge, the PCE price index, alongside the core measure that strips out food and energy. Consensus points to a third consecutive 0.2% monthly rise in the core index, which would leave the annual rate just under 3%. That outcome would reinforce the narrative of inflation that is no longer accelerating but remains stubbornly above target.

CAD: Elevated risk

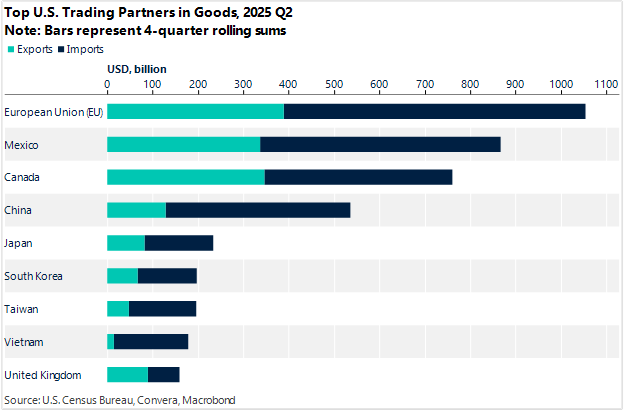

While the last two weeks the macro sentiment has been upbeat after surprises in Q3 GDP and the November employment report, the approaching review of the USMCA (or CUSMA) deal in 2026 places the North American trade relationship under significant and elevated risk. U.S. Trade Representative Jamieson Greer has confirmed that a total withdrawal is “always a scenario” under the current administration, echoing the President’s negotiation tactic of threatening to tear up the deal. This is more than a rhetorical pressure point; it reflects the administration’s stated goal of “reshoring” manufacturing jobs to the U.S., a policy already being validated by corporate decisions, such as Stellantis’s recently announced plan to invest $13 billion over the next four years to grow its business and domestic manufacturing footprint in the critical United States market. This aggressive stance is aimed at extracting concessions or potentially pursuing an entirely different trade structure, specifically the idea of divorcing the trilateral agreement into separate, more favorable bilateral deals with Canada and Mexico.

In response to this looming threat, the Canadian business community is united in a desperate plea to preserve the foundational agreement. Leaders from key organizations, including the Canadian American Business Council and the Business Council of Canada, are testifying in Washington with a clear message: the agreement must be extended and enhanced, but not trashed. They are advocating for the full adoption of existing chapters while seeking improvements like streamlining rules-of-origin documentation. However, the risk of being sidelined remains palpable, with Canadian leaders expressing concern that the U.S. and Mexico may negotiate their own deal, forcing Canada to accept unfavorable terms or face exclusion, a scenario that played out during the original USMCA negotiations.

The high-stakes nature of the CUSMA review extends far beyond trade politics and is seen as a major destabilizing event for the Canadian economy. The Bank of Canada has flagged the USMCA review as a “potential risk event,” noting that the United States’ ability to unilaterally withdraw could fragment the integrated North American trade landscape. This uncertainty, fueled by potential future U.S. trade actions and the looming review, is already negatively affecting investor confidence and corporate planning. Canadian businesses are advised to take the threats seriously but to track official USTR data, which often proves “less sharp” than the political rhetoric, while emphasizing the deep integration of the two economies, a reminder that harming Canada’s supply chains risks hurting the U.S. as well.

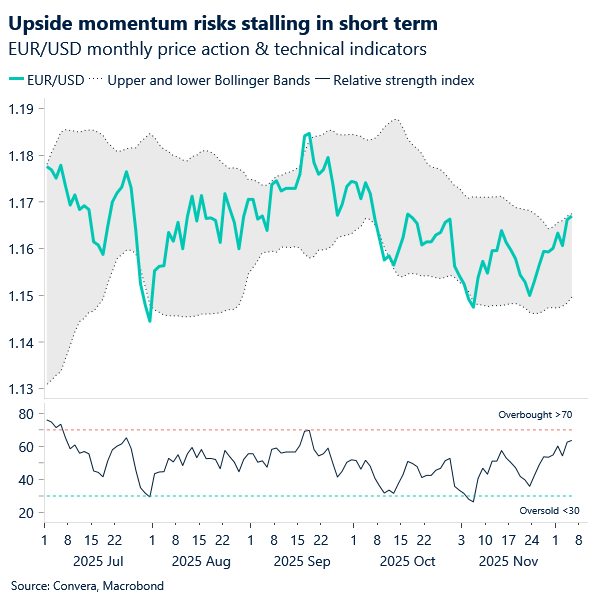

EUR: Euro rallies, but politics cloud the path

EUR/USD has staged a decisive bullish move, climbing above several key technical levels and holding above its 200‑day moving average. Options markets reflect this momentum, with positioning gauges at their most constructive in almost three weeks. The setup points to further upside potential, though a more stable risk environment is likely needed before the dollar weakens more convincingly against risk‑sensitive currencies. Sustainability will hinge on cohesive dovish messaging from the Fed, set against a still‑fractured US data backdrop.

Geopolitical developments remain a limiting factor. Witkoff’s visit to Moscow yielded no breakthrough, capping euro gains in the near term. Meanwhile, political risk is rising across Europe. In France, budget approval remains uncertain, while in Germany Chancellor Merz faces a rebellion within his party over a pension bill. A failure to pass the legislation could see the SPD withdraw from the coalition, raising the prospect of fresh elections. Such instability would jeopardize the rollout of Germany’s stimulus package and undermine efforts to restore competitiveness in Europe’s largest economy.

For traders, the risk is that optimism around the euro collides with renewed policy uncertainty. A weak German recovery, fiscal gridlock in France, and the possibility of a soft 2028 inflation projection from the ECB on December 18 could shift the conversation back toward rate cuts.

That leaves EUR/USD vulnerable to setbacks if political instability and dovish ECB signals converge, even as dollar softness provides tactical support.

Market snapshot

Table: Currency trends, trading ranges and technical indicators

Key global risk events

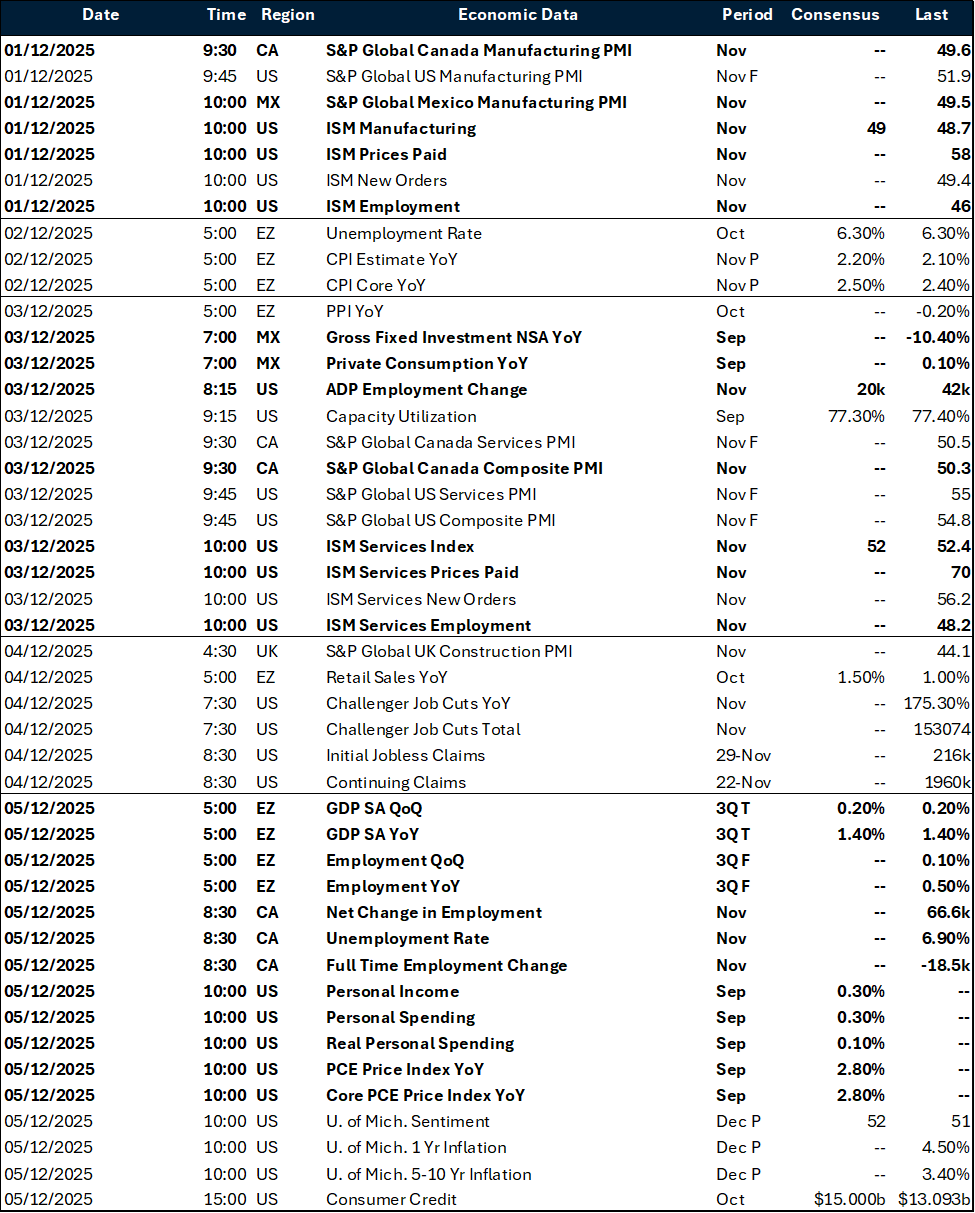

Calendar: December 01 – 05

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.