The dollar index climbed to 98.8 as renewed instability in the Middle East spark fresh concerns over an inflationary spiral. With WTI crude futures jumping 5% to over $101 a barrel, the greenback is rebounding while energy costs hit their highest levels since early April. This rally reflects a growing market anxiety that a simple pause in fighting will not be enough to stabilize the energy market. Consequently, the pressure remains high as traders wait to see if diplomacy can actually restore the flow of goods.

Much of this tension stems from President Trump’s dissatisfaction with Iran’s latest proposal to end the three-month conflict. While Tehran offered an interim deal to reopen the Strait of Hormuz, the White House continues to demand stricter curbs on Iran’s nuclear program as a condition for lifting port blockades. Even though a ceasefire has largely held on the ground, these mutual restrictions have kept shipping traffic at a standstill. Until both nations resolve these nuclear sticking points, the energy market will likely stay volatile and keep the dollar on its upward trajectory.

CAD: Up mostly on broad USD pullback

The CAD’s last three weeks of gains look a lot more like a USD story than a fresh loonie renaissance. USD/CAD sliding toward the mid‑1.36s has lined up neatly with a broader unwind in safe‑haven demand as markets price a less binary Middle East outcome, and the US dollar slowly sheds the conflict premium it built when escalation risk felt open‑ended. That’s very much the set‑up we’ve been flagging in the Daily Market Update: when diplomacy starts to look even marginally credible, the “defensive USD bid” leaks, risk assets breathe, and USD/CAD can drift lower almost by default.

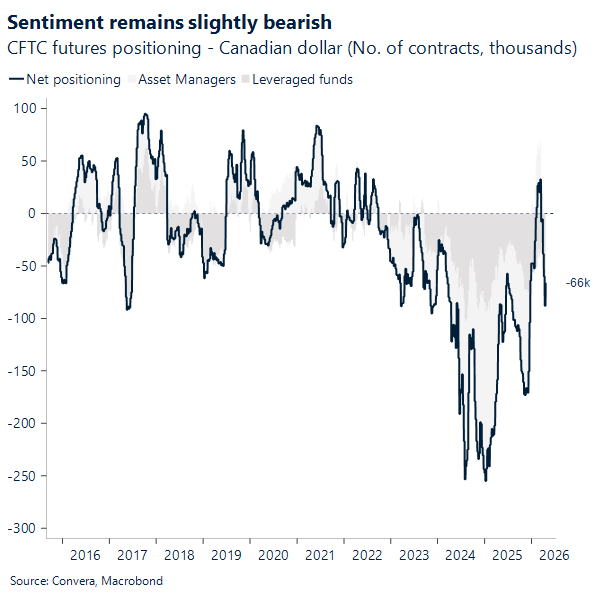

What’s telling, though, is what hasn’t changed under the hood. The CFTC “Canadian dollar” futures indicator still shows net positioning slightly bearish, investors remain net short CAD (roughly the mid‑tens of thousands of contracts), which is hardly the backdrop you’d expect if this were a genuine, internally driven CAD re‑rating. And unlike NOK, where terms‑of‑trade strength can pull a much cleaner lever through growth momentum and a more supportive rates mix, Canada’s growth and policy runway simply aren’t in the same place, so the same ToT impulse doesn’t translate one‑for‑one into sustained FX support. In other words, early‑March “CAD exceptionalism”, that oil‑and‑fear‑bid window where the loonie briefly traded like the market’s preferred energy hedge, has faded as the geopolitical beta cooled and the petrocurrency narrative reverted back to being regime‑dependent and capped by broader USD dominance.

That leaves the CAD with a slightly uncomfortable truth: it can thank a weaker USD for the recent push, but it can’t claim much homegrown alpha for it, and that’s exactly why it’s also basically flat year‑to‑date and is rebounding today as oil and Dollar rebound. Without a durable domestic growth turn, without a rates impulse that forces a repricing of the BoC path, and with trade policy uncertainty still acting like an overhead premium as CUSMA/USMCA conversations remain sluggish, there just isn’t a second engine to pull USD/CAD meaningfully closer to “fair value.” So yes, the loonie has looked better on the tape recently, but strip out the USD’s de‑escalation unwind, and you’re left with a currency still constrained by the same macro frictions we’ve been circling for months.

GBP: Politics to test sterling’s resolve

Sterling started the week mixed, reflecting the tension between resilient global risk appetite and rising oil prices. On Monday, the pound advanced against safe‑haven and low‑yielding peers but underperformed high‑beta commodity FX, including the Scandis and Antipodeans. Overnight, a hawkish hold from the Bank of Japan has weighed on GBP/JPY whilst further gains in oil have dragged GBP/USD towards 1.35 into Tuesday’s session.

Even so, the broader sterling backdrop remains constructive. GBP/USD is on track for its biggest monthly gain in over a year (>2%), consistent with historically strong April seasonality. After breaking out of the late‑January to March downtrend, the pair has remained supported above its key daily moving averages, helped by easing conflict risks. Near‑term price action looks more like consolidation than reversal, suggesting the market is catching its breath after a sharp recovery. On balance, the rally should re‑assert itself, though ongoing uncertainty around US–Iran negotiations is likely to cap upside momentum for now.

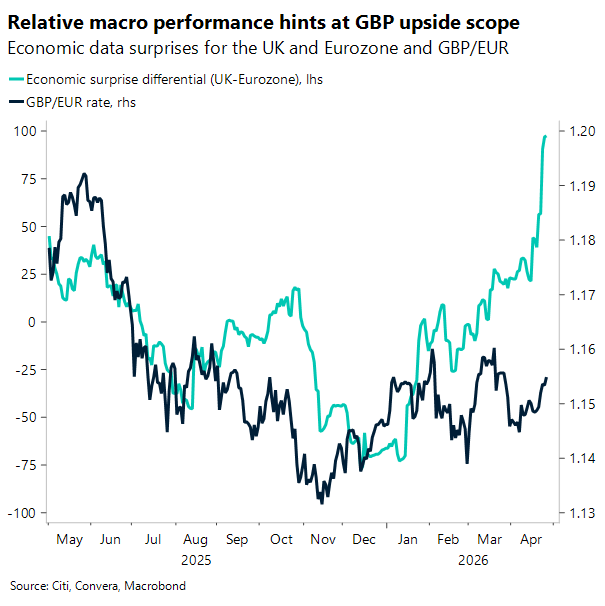

Elsewhere, GBP/EUR retains scope to grind higher. The UK–Eurozone economic surprise differential has climbed to a two‑year high, pointing to a widening gap in relative macro momentum. While the relationship is far from mechanical, the divergence suggests that sterling has yet to fully reflect the extent of the UK’s outperformance relative to the Eurozone.

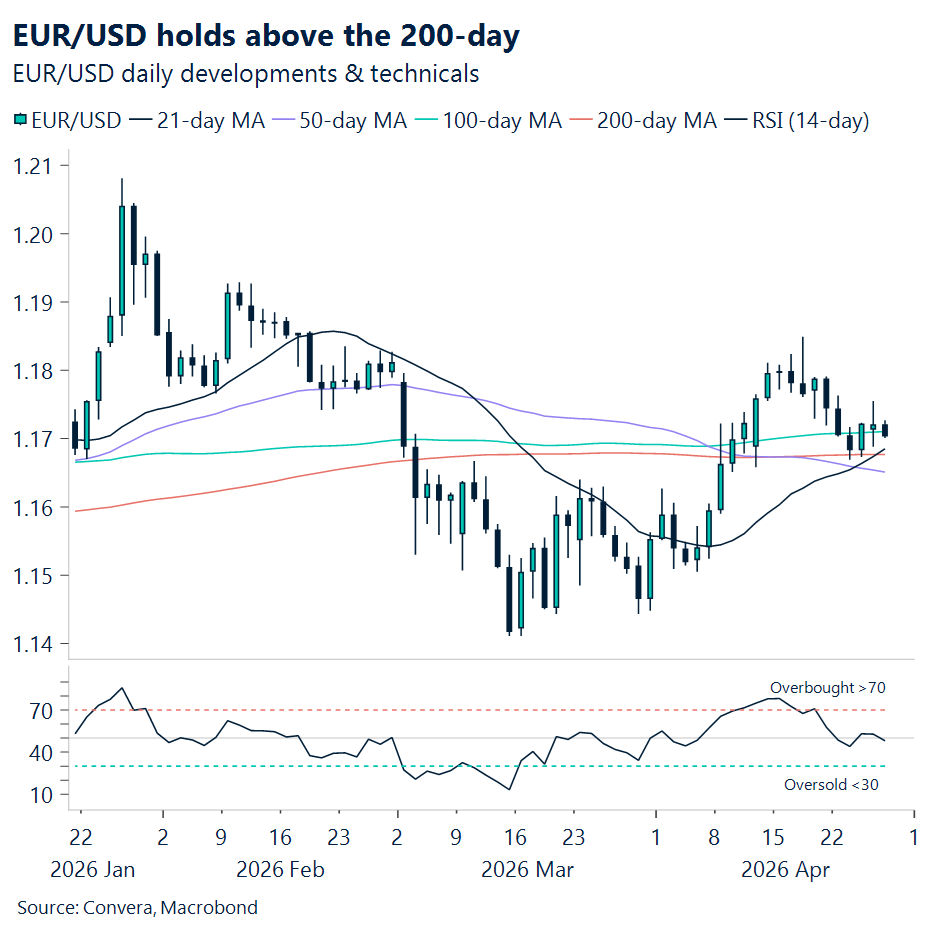

EUR: EUR/USD stabilises above 200‑day

EUR/USD hovered above the 1.1680 level, which coincides with the 200‑day moving average – a widely followed gauge of long‑term momentum. This resilience underscores markets’ still‑intact, albeit bruised, sense of optimism that the conflict in the Middle East will be resolved in the near term, particularly under a scenario in which the Strait of Hormuz is reopened. While bouts of re‑escalation persist, the broader trajectory continues to point toward tentative de‑escalation.

Indeed, after trading below the 200‑day moving average for most of March, the pair re‑established itself above this level in early April as de‑escalation momentum gained traction.

With little in the way of data today, and with the Fed and ECB meetings scheduled for tomorrow and Thursday respectively, we expect consolidation around the 1.17 handle, with limited directional impetus as markets await further clarity on both the geopolitical front and central bank signals. Absent any significant geopolitical developments, we continue to favour mild downside for the euro relative to the dollar this week. This view is anchored in the Fed’s relatively hawkish leanings, which we see as more credible to markets given expectations that the US economy will prove more resilient than the eurozone in absorbing any spillover from ongoing geopolitical risks. Yet we do not view this factor as a sufficiently strong bearish impulse to drive a clear‑cut break below the 200‑day.

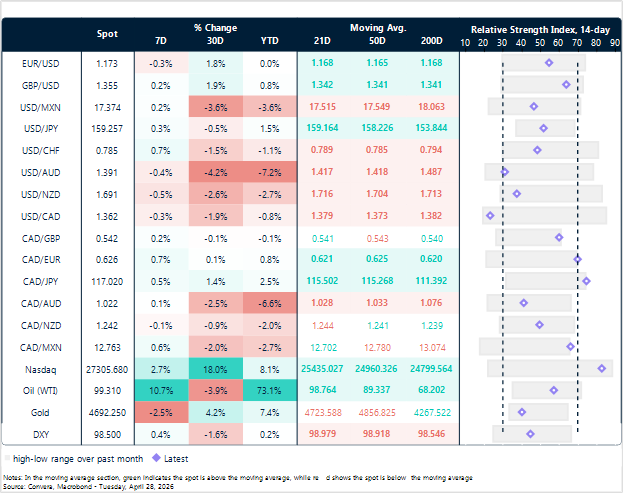

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

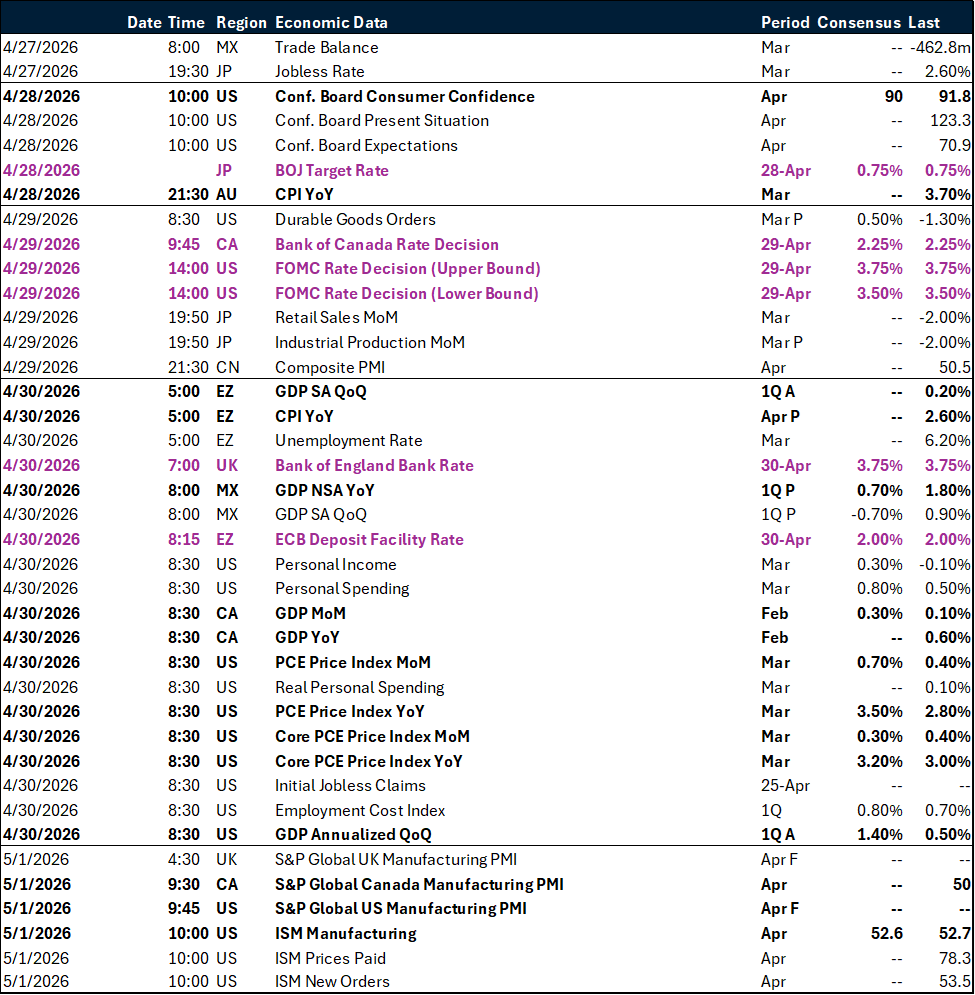

Calendar: April 27 – May 01

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.