USD: Softer on peace hopes, but we’ve been here before

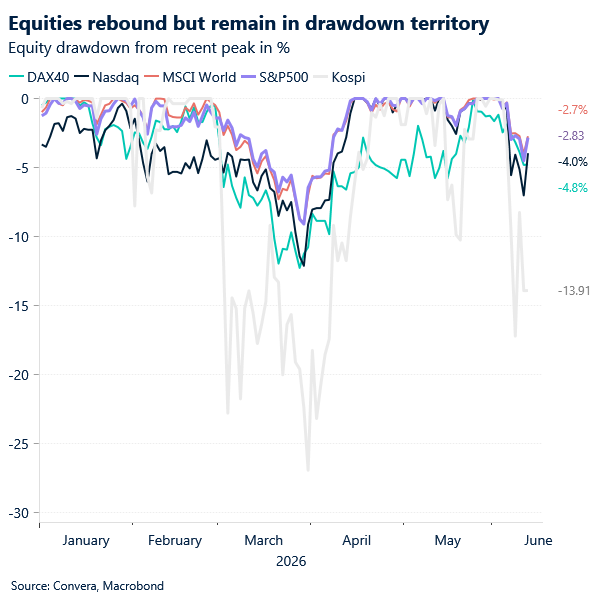

The US dollar has extended its recent pullback, with the DXY index slipping for a fourth consecutive session and again struggling to hold above the 100 level as shifting geopolitics revive risk sentiment. President Trump’s decision to halt planned strikes on Iran and signal that a deal could be finalised as soon as the weekend has supported global equities. Technology stocks are leading the move. Korea’s Kospi has surged around 8%, while US equity futures are also edging higher ahead of SpaceX’s expected Nasdaq debut later today. Still, stocks remain a way off their all-time peaks.

Last night’s announcement – calling off strikes after agreeing key terms – fits the pattern of a volatile sequence of escalation threats and subsequent reversal. But we’ve been here before and cannot rule out yet another false promise. Thus, although oil prices have eased about 5% this week, the decline remains limited by uncertainty around the durability of any agreement and the continued lack of clarity on reopening the Strait of Hormuz. That dynamic suggests a near-term floor for energy rather than a sustained collapse.

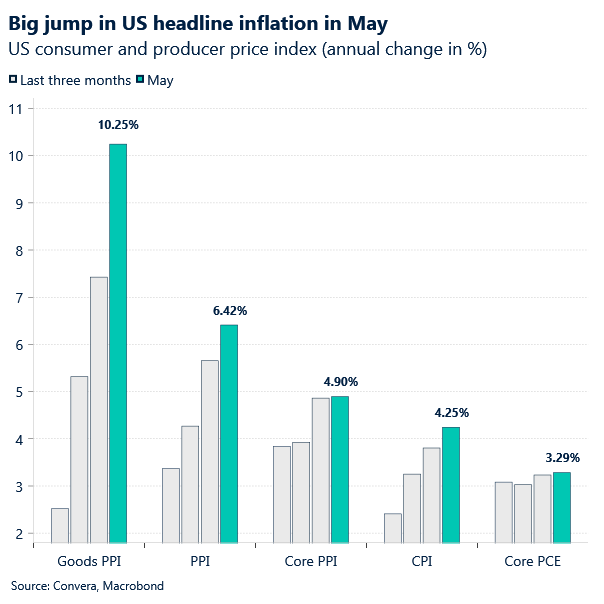

The dollar’s decline naturally reflects the improvement in risk appetite, but the downside has been restrained too. Over recent weeks, the drivers of USD support have broadened beyond geopolitics. Real yields remain elevated, inflation data continue to surprise to the upside, and Fed pricing has shifted in a more hawkish direction. After CPI came in at a 3-year high earlier this week, strong ‘supercore’ PPI on Thursday reinforced that inflation is proving more persistent than hoped.

Taken together, this explains why a more constructive geopolitical backdrop does not translate into a clear USD bearish outcome. The dollar may lose some of its defensive bid, but underlying support from rates and relative growth dynamics continues to anchor it.

EUR: Policy missteps risk an own goal for growth

The European Central Bank (ECB) delivered a 25bp rate hike yesterday, lifting the deposit rate to 2.25%, marking its first increase since September 2023. The move was expected and framed as an insurance play – a pre‑emptive strike against rising inflation driven by the Middle East energy shock, and an attempt to avoid being caught flat‑footed again.

However, beneath the headline, the message was more mixed. Updated staff projections showed higher inflation alongside weaker growth, reinforcing the stagflationary backdrop. President Lagarde emphasised upside risks to prices, but maintained a data‑dependent stance, offering little guidance on the path ahead. Markets took the signal in stride, with pricing for further tightening largely unchanged.

This is where the euro’s challenge lies. ECB hikes are no longer a straightforward positive for EUR/USD. Tightening into slowing growth risks becoming a policy trade‑off rather than a source of support – a potential own goal if it further undermines activity without materially improving the euro’s yield appeal. The FX reaction reflected this. EUR/USD was broadly muted, as the hike was already priced and overshadowed by resilient US data and a firmer Fed backdrop.

That said, the positive geopolitical developments in the Middle East allowed the euro to extend its rebound from 1.15, – a key level of support for the past few months.

Looking ahead, the euro requites this kind of external support to mount a sustained rally as ECB action alone is unlikely to be enough to kickstart a fresh uptrend. Instead, the heavy lifting would need to come from either a clearer geopolitical de‑escalation or a softer US outlook and dovish Fed signals.

GBP: Pound attempts to reclaim 1.34

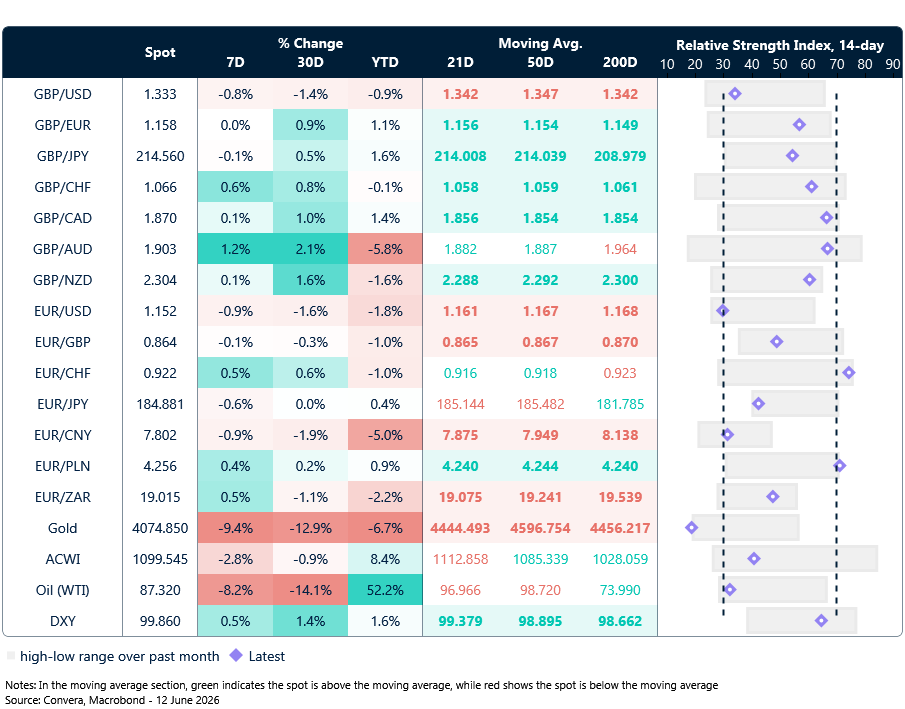

The pound traded in a relatively subdued fashion yesterday amid a light data calendar. On a week-to-date basis, the currency sits stronger against its G10 peers. GBP/USD has recovered from last Friday’s drop below 1.34 and is now attempting to reclaim the 1.3420 area, which aligns with the 200-day moving average. Since early 2026, the pair has fallen below this level only twice, during periods of heightened US-Iran tensions in March and in the immediate aftermath of May’s local elections.

Sterling continues to show limited sensitivity to domestic developments. The political backdrop remains fragile following the resignation of Defence Secretary John Healey, who cited concerns over defence funding. This morning’s macro data added little support either, with UK GDP contracting by 0.1% in April while industrial production stagnated. Together, these figures point to subdued momentum, reflecting the drag from elevated energy prices and tightening financial conditions, and mark a clear shift from a robust first quarter in which the UK recorded the strongest growth among G7 economies.

Looking ahead, next week carries greater significance for both gilts and the pound. The Makerfield by-election could reopen questions around party leadership, with Andy Burnham seen as a potential challenger, while the Bank of England’s June policy meeting will also be closely watched. For now, GBP/USD remains guided by conflicting geopolitical forces, and a sustained move higher through 1.3420 appears unlikely unless yesterday’s optimism around diplomatic progress becomes more tangible.

Market snapshot

Table: Currency trends, trading ranges & technical indicators

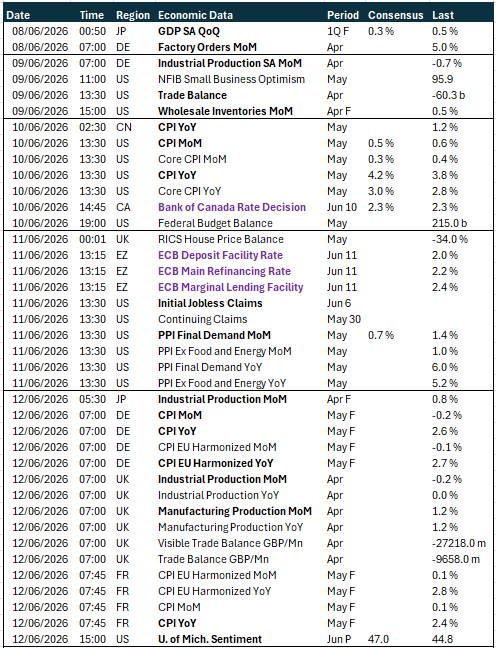

Key global risk events

Calendar: June 8-12

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.