USD: Macro backdrop is dollar positive

All macro releases yesterday coming out of the US were dollar positive. Initial applications for jobless benefits in the US fell to the lowest since mid-July, according to Labor Department data. This decline signals a resilient labor market with relatively few layoffs, and the number of claims remains too low to suggest an impending recession. The four-week moving average, a smoother gauge of claims, also dropped to 237,500. Meanwhile, continuing claims, which measure the number of people receiving benefits, were largely unchanged at 1.93 million after the previous week’s data was revised upward.

Furthermore, the revised Q2 GDP reading was updated from 3.3% to 3.8%, marking the fastest pace in nearly two years. This upward revision was driven by stronger-than-expected consumer spending. These recent data points, combined with recent hawkish ‘Fedspeak’, have propelled the USD to climb almost 1% in the last five days.

Since August, we have been arguing that the bar for continued US dollar weakness has risen. The market’s recent dollar depreciation was largely a result of currency hedging and portfolio repositioning, not a wholesale dumping of US assets. While the consensus view still points to further dollar weakness toward the end of the year, we’ve noted several factors that make a continued decline more challenging. These include the resilience of US economic growth, the continuous floor provided by historical fiscal deficit, a cautious Fed, and a market that has already priced in much of the expected easing. The dollar’s performance is now more dependent on actual economic outcomes rather than just market expectations of a dovish Fed.

The dollar’s recent resilience is difficult to ignore. Many market participants had anticipated that last week’s Fed meeting would be the catalyst for the USD to weaken further. However, Fed Chair Powell made it clear that the normalization path isn’t a done deal and the two rate cuts that markets are expecting in the remaining two meetings this year are far from guaranteed.

Today, we’ll get the core PCE report, the Fed’s preferred measure of inflation. We’ve been flagging since August that the Fed’s dilemma isn’t going away, and that stagflation, even in a mild form, remains the primary macro risk. This risk could cap the momentum in global equities, which have recently seen indexes around the world hit all-time highs. Given that underlying pressures are broad-based across the US CPI basket, with 72% of CPI components now increasing at an annualized pace above 2%, a level not seen since mid-2023, markets may be in for a reckoning.

EUR: Dollar drives, euro drifts

There was nothing soft about yesterday’s US macro data revisions. For a deeper dive, see the USD section by my colleague Kevin – but in short, both GDP and the core PCE price index were revised higher quarter-on-quarter, while weekly jobless claims continued to edge lower. The euro, in turn, is adjusting to this ongoing reshuffling of Fed expectations – now tilting more convincingly hawkish.

Days like yesterday highlight how the euro’s reliance on dollar dynamics throughout its ascent this year may become its hindrance. A combination of factors exerted downward pressure on the euro, causing it to bleed another ~0.6% for two days in a row.

To start, just as mixed tones from Fed speakers emerged regarding the policy outlook – with caution prevailing – there come these data revisions, clearly favouring a more hawkish path forward. Meanwhile, there continues to be particularly strong sentiment component attached to US macro releases, which investors are dissecting to untangle the lingering effects of tariff distortions. When data surprises to the upside, the dollar tends to benefit more than fundamentals alone would justify – leaving the euro exposed. Finally, headline risk tied to tariff announcements has faded, removing yet another source of fuel from the euro’s ascent.

Looking ahead, if US macro data continues to overshoot expectations (today’s PCE and personal spending in focus), EUR/USD is poised to breach support at $1.1650, followed by $1.16. Beyond that, there’s little until $1.14 – a level only briefly breached back in late July, before staging a bounce.

GBP: Sterling under stress as gilt yields surge

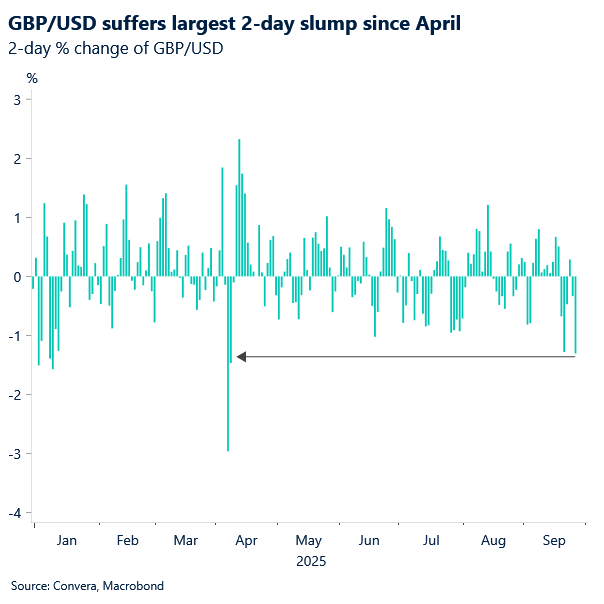

Sterling has endured its sharpest two‑day drop against the US dollar (-1.3%) since April’s tariff‑driven turmoil. The currency remains under pressure as surging UK long‑term yields collide with a resurgent dollar, buoyed by strong US data and fading Fed easing bets. From its Sept 17 peak, GBP/USD has now fallen nearly 3%, leaving the pair hovering near monthly lows after tracing a technically bearish shooting‑star pattern.

On the domestic front, rising yields on long-dated bonds suggests investors are losing faith in the government’s long-term financial credibility. UK 10‑year yields hit their highest since early September and 30‑years edged back toward the 27‑year peak of 5.75%. While Andy Burnham’s comments that the bond market shouldn’t dictate government policy grabbed headlines, markets tend to discount remarks from figures without direct policymaking power. Rather, the move reflects supply concerns as the Bank of England (BoE) continues to run down its holdings and fiscal needs remain elevated, amplified by weak demand at yesterday’s short‑dated auction.

As for the pound weakening while yields rise – this is not a healthy sign. It usually means the market is treating higher UK rates as a symptom of stress (fiscal, credibility, or growth risks) rather than as a positive carry story. As we stated in yesterday’s support, a break below $1.34 would expose the September swing low at $1.3333. The next key support is the 200-day exponential moving average located at $1.3254, which if broken, opens a path toward August’s low of $1.3142.

GBP/USD drops into oversold territory

Table: Currency trends, trading ranges and technical indicators

Key global risk events

Calendar: September 22-26

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.