USD: Data mixed, dollar holds firm

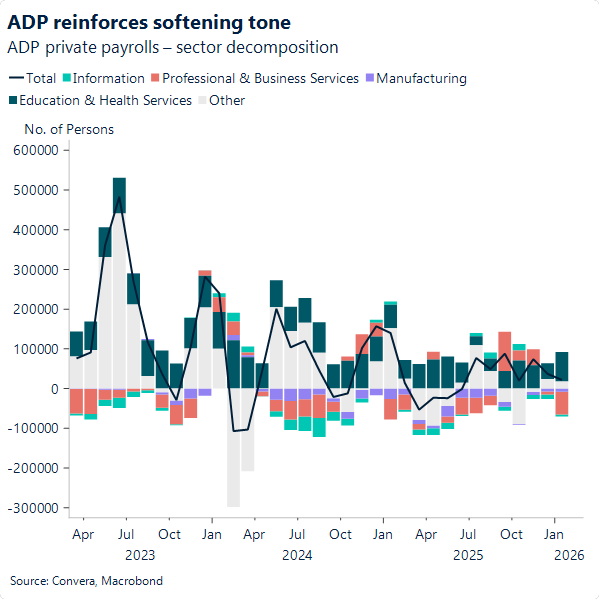

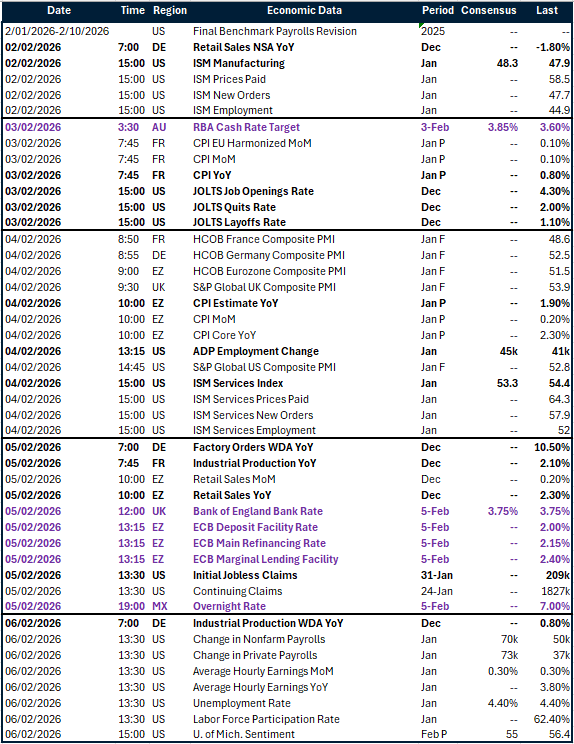

Yesterday saw the release of the ADP report, capturing private sector payrolls. It showed 22k jobs added in January, below the 45k estimate. The print points to continued cooling and, in the absence of the gold‑standard NFP this Friday, stands as the fullest picture of the US labour market for January. That said, the series is known for its volatile behaviour while the latest print still sits within the past few months’ range, suggesting no major deterioration. The dollar appeared in fact indifferent to the outcome.

Meanwhile, the ISM services survey was unchanged at 53.8 in January, maintaining the strongest levels since 2024 and underscoring robust business activity. We noted the new orders component, the most forward‑looking element, edging lower from 56.5 to 53.1. That is not entirely surprising given January’s turbulence, with renewed tariff tensions and a geopolitically fragile backdrop around Greenland likely dampening demand for future orders. The sub-index nonetheless remains aligned with its 3‑year average.

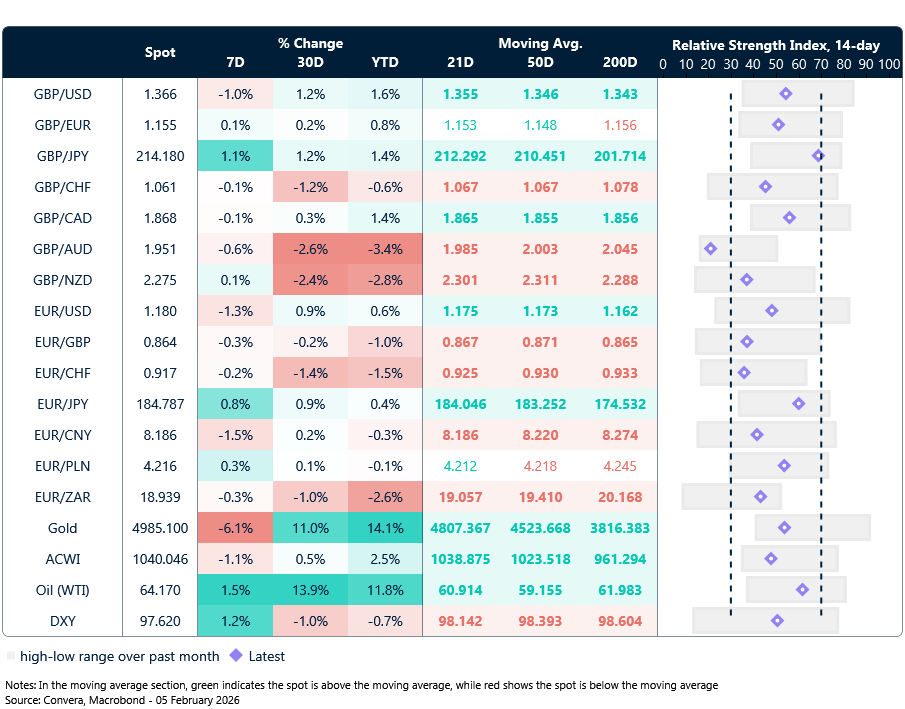

The dollar index edged higher on the data, with markets digesting the overall picture quite positively. It appears to have lifted decisively off 97.300 short-term support, now heading toward the 98 mark from its January lows at 95.551. The dollar’s resilient posture this week, despite the light data calendar, suggests investors remain keen on re‑establishing macro‑warranted upside and are awaiting further releases to commit to it. They will wait until next week, when the BLS is scheduled to release the delayed jobs report (initially due tomorrow).

Beyond the data, we believe that, Treasury Secretary Bessent’s comments in his testimony to Congress yesterday, where he reiterated that the administration supports a strong‑dollar policy, may also have contributed to keeping the dollar bid.

Today brings the delayed JOLTS report, with particular attention on layoffs. While the figure should remain contained, it may stand in sharp contrast to the Challenger layoffs report due today as well. The latter captures announced layoffs rather than actualised ones, and we may see some overshoot given the recent announcements from Dow Inc. and Amazon Inc. of substantial job cuts. Even so, we do not expect the dollar to be particularly bothered by it.

EUR: Soft core, softer euro risk

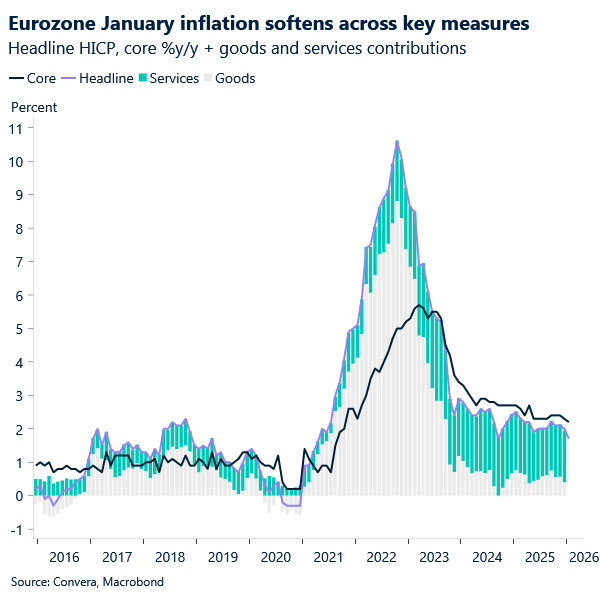

Yesterday, eurozone HICP inflation for January decelerated to 1.7% y/y from 2% (revised from 1.9%) in December, in line with expectations. More instructive was the downward surprise in the core component, which eased to 2.2% from 2.3% despite forecasts for an unchanged reading. The move was driven by a decline in services inflation, which slipped from 3.4% to 3.2%.

The clear deflationary bias may recalibrate how much weight any discussion around the possibility of another cut prompted by a stronger euro carries at today’s ECB policy meeting. In light of the release, we could see a mildly bearish reaction in the euro should Lagarde make more direct reference to such dynamics. That said, given the euro’s muted response to yesterday’s data outcome, we lean toward limited follow‑through in the currency.

Beyond the meeting, which is expected to deliver a steady hand, keep an eye on eurozone retail sales activity on the data front.

GBP: BoE poised to hold, but not to signal

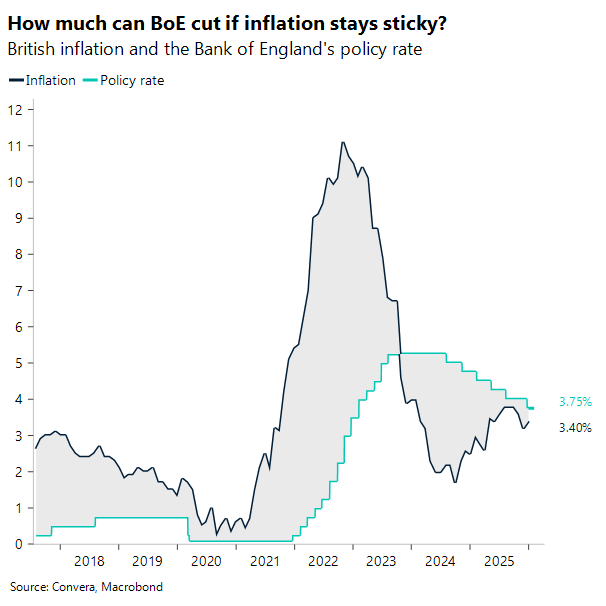

We expect the Bank of England (BoE) to hold rates at 3.75% today, with policymakers still divided on the timing of future cuts. December’s move was a reminder of the MPC’s cautious streak: even as it delivered a cut, it warned that the “cadence” of easing could slow. With inflation still above 3%, the hawkish wing remains uneasy about declaring victory, and memories of the 2022 inflation shock continue to shape the debate.

The data since the last meeting has been limited and mixed. Softer labour‑market signals have been offset by firmer PMIs, while December inflation surprised slightly higher. Wage expectations in the Decision Maker Panel survey remain stuck around 3.7% — a level repeatedly cited as a reason for restraint. A 7–2 vote to hold looks the most plausible outcome, and while we still see a strong case for a cut by March or April, the MPC is unlikely to pre‑signal anything today. Expect the familiar line: keep options open, stay data‑dependent, and avoid validating market pricing unless absolutely necessary.

A hawkish hold could propel GBP/USD to fresh multi‑year highs. Cable has already rallied hard in 2026 despite narrowing UK–US rate differentials. January’s broad dollar sell‑off briefly pushed the pair above $1.38 — levels last seen in 2021 — before a modest USD rebound pulled it back into the $1.37s. But the structural forces weighing on the dollar haven’t disappeared. If the BoE continues to resist early‑easing calls and keeps short‑end gilt yields supported, the UK–US front‑end spread could widen again, giving sterling another leg higher.

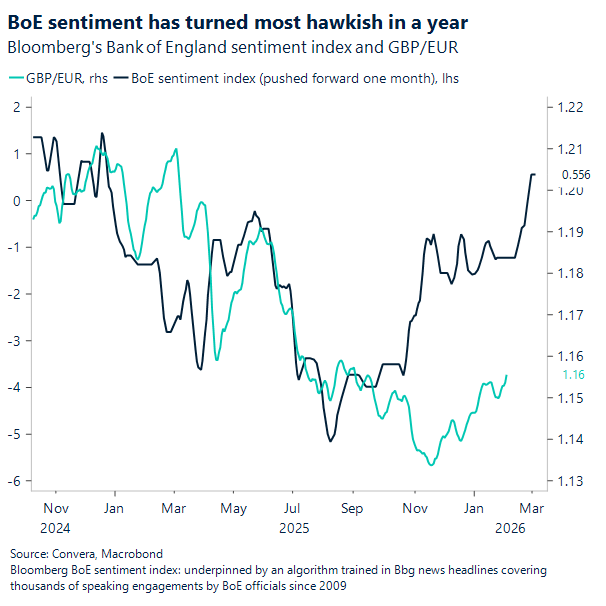

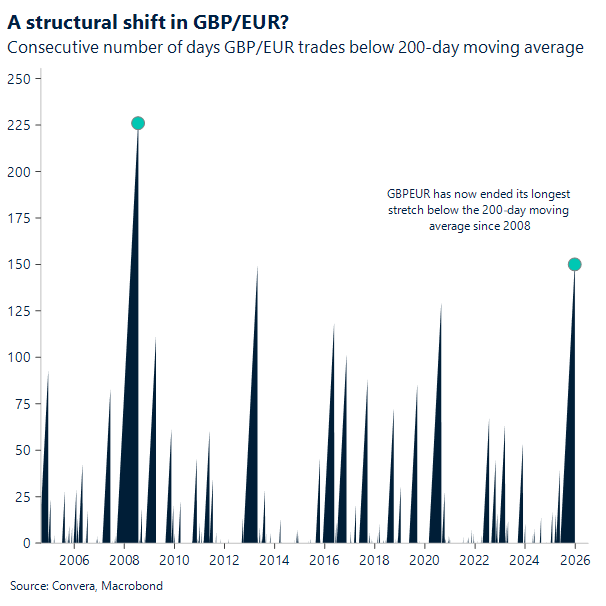

GBP/EUR is trading at its highest level in around five months. Bloomberg’s BoE Sentiment Index has turned its most hawkish in over a year, and GBPEUR has historically lagged this shift — hinting the pair could catch up. But that signal is only one side of the story: with the ECB unlikely to cut while the BoE still has easing ahead, the correlation is softer this time. Even so, both nominal and real rate differentials still point to GBP/EUR being undervalued, with the UK holding a modest advantage on both measures.

The technical backdrop reinforces that message. GBP/EUR has just ended its longest stretch below the 200‑day moving average since 2008 — a meaningful shift after months of persistent downside pressure. Reclaiming the 200‑day signals a potential momentum turn, with trend metrics stabilising and a long‑term resistance line finally giving way. The sheer duration of the sub‑200‑day streak shows how entrenched the bearish trend had become, making the recent recovery more significant.

Still, part of the valuation gap likely reflects the euro’s role as the main liquid alternative to the USD during periods of US policy uncertainty. When the dollar carries a higher risk premium, global flows tend to favour EUR over GBP, suppressing GBP/EUR even when fundamentals argue for a stronger pound.

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

Calendar: February 2-6

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.