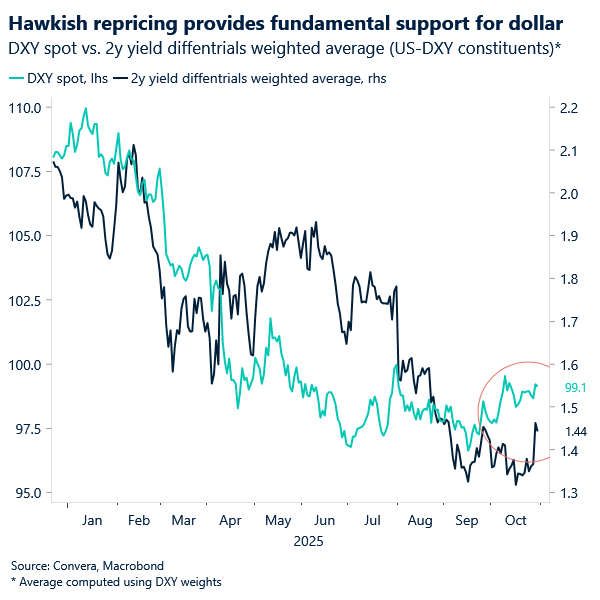

USD: Fed holds the line, trade lifts

The Federal Open Market Committee voted 10–2 to lower the target rate by a quarter point to 3.75–4.00. As anticipated, yesterday’s Fed meeting proved dollar-positive – the dollar index closed 0.5% higher. As we had anticipated, the setup echoed September: a cautious cut, with December still “far from a foregone conclusion”, keeping dollar bid.

The Fed also announced it will halt balance sheet runoff starting December 1, ending a two-year unwind that shaved over $2 trillion from its holdings.

There was acknowledgment of a broadly resilient macro backdrop, with the economy expanding at a moderate pace, underpinned by still-strong consumer spending. Inflation remains somewhat elevated – particularly tariff-driven goods inflation, which has picked up and may prove stickier than expected.

When asked about the drivers of labour market softening, Powell pointed to supply-side shifts as the primary force, citing lower immigration levels tied to Trump’s agenda. This nuanced dynamic helps explain the apparent contradiction with strong consumer spending.

What stood out was the Fed’s growing confidence in alternative data sources to guide decision-making – an essential pivot given the ongoing government shutdown. Rather than lulling in sheer uncertainty and offering no directional impetus, Powell’s remarks grounded the tone, transmitting a deliberate blend of conviction and caution, lending the statement a firmer, more directionally biased edge than markets may have anticipated.

Meanwhile, positive momentum around trade negotiations – coupled with the AI-driven equity rally and Powell’s tone – continues to dull the optics of dysfunction stemming from the shutdown, offering baseline support for the dollar. During the current trip to Asia, President Trump and South Korean President Lee Jae Myung finalized a trade deal, capping months of negotiation over a framework agreement. Under the deal, Seoul will invest $150 billion in shipbuilding, with an additional $200 billion earmarked for broader investment pledges. In return, the US will cap tariffs on South Korean goods at 15%.

Next up: China. The much-anticipated meeting is unfolding at the time of writing, and hopes are high that the two sides will strike a truce – or perhaps something more enduring. For now, only good news: the two parties have reached consensus on cooperation to combat fentanyl-related narcotics, expand agricultural trade, and address TikTok. Meanwhile, the US has extended its suspension of the 24% reciprocal tariff for another year.

We see the 99 handle as more amicable to the dollar now that the alternative data-grounded cautious tone has been reaffirmed, with sentiment further buoyed by positive trade negotiation momentum. Yet for a more sustained upside in these waters, the much-needed gold-standard hard data remains essential.

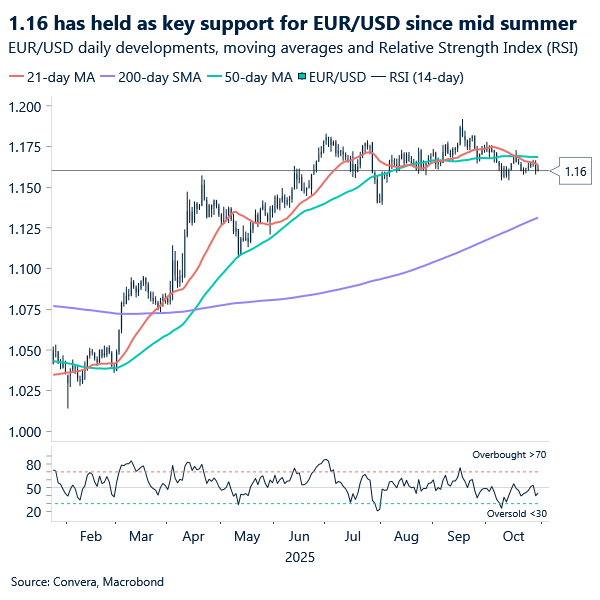

EUR: 1.16 still holding the line

EUR/USD dipped south of 1.16 yesterday, following the cautious tone from the Fed’s meeting, before paring back some losses that returned to 1.16 waters. In fact, rate guidance alone seems insufficient to justify a more sustained sub-1.16 exploration. Support has held up since it was officially tested in mid-July. A sustained move below 1.16 would likely require upside surprises in official US macro data – assuming the shutdown is lifted – to extinguish, or at least reduce further, lingering USD-negative sentiment from the tariff-driven sell-off earlier this year.

Today’s key event is the ECB policy meeting. With an ECB seemingly complacent about the current policy stance, the data backdrop since September has certainly proved too inconsistent to shake the Bank’s conviction in any meaningful way. While recent Ifo and PMIs offered broadly positive signals for the eurozone’s outlook, earlier production and consumption data had disappointed. Meanwhile, key figures – including inflation prints for Germany and Spain, Q3 GDP estimates, and the Commission’s sentiment data – are due today, but too late to inject fresh impetus into the ECB’s forward guidance.

Inflation remains the ECB’s central focus. The latest September print came in orderly, but downside risks tied to a stronger euro and falling oil prices make the prospect of a December cut a much more hotly debated issue. We expect EUR/USD to tread water around 1.16 today.

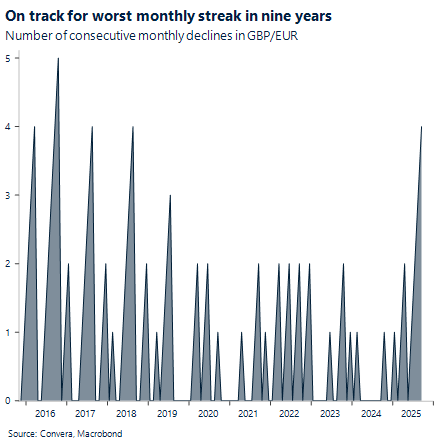

GBP: Traders bet on more pound pain

The British pound is having a brutal October, down 1.8% against the US dollar and falling to its lowest level in two years versus the euro. It’s on track for the longest monthly losing streak in nine years against the common currency. The selloff reflects mounting fiscal concerns ahead of the UK Budget and rising bets of Bank of England (BoE) rate cuts.

The pound is coming under pressure as investors brace for potential tax rises and spending cuts in the upcoming UK Budget that may exacerbate the economic slowdown. The UK’s fiscal watchdog is expected to significantly downgrade its productivity growth forecast, making it harder for Chancellor Rachel Reeves to meet her fiscal rules at the Nov. 26 budget.

If confirmed, it could blow a £25–30bn hole in the public finances, forcing Reeves to tighten fiscal policy just as growth falters. That prospect has already triggered a slide in gilt yields and raised market expectations for a BoE rate cut as early as next week. Cooling inflation is also helping the case for rate reductions. On Tuesday, the British Retail Consortium revealed that UK food prices posted the largest monthly drop since late 2020.

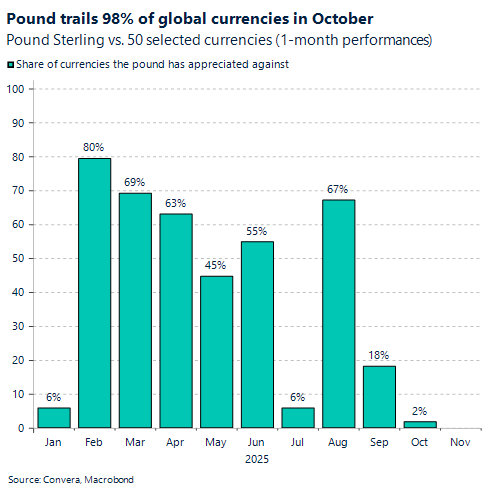

Lower yields may offer some relief to the Treasury by reducing debt servicing costs, but they’ve also eroded the pound’s relative yield appeal. Out of a basket of 50 currencies we track, sterling has appreciated against just 2% this month – making this its worst monthly showing since September 2022.

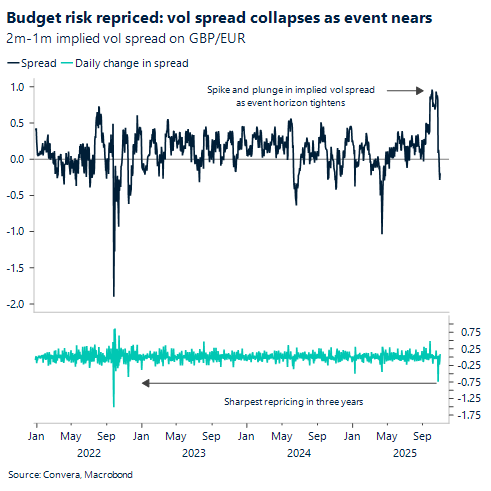

Options markets point to further pound volatility and weakness. The cost of insuring against swings in sterling has surged to its highest premium over the euro since 2023. Risk reversals — a key barometer of sentiment — are now the most bearish on the pound since July, underscoring the market’s growing unease. Finally, as seen in the chart below, the implied volatility spread between 2-month and 1-month GBP options spiked in early October as markets priced in Budget-related risk. But as the event drew closer, that risk shifted into the front-end, collapsing the spread in one of the sharpest one-day moves in over three years. The message is clear: markets view the Budget as a near-term volatility catalyst.

Sterling sits at the bottom of the RSI spectrum

Table: Currency trends, trading ranges and technical indicators

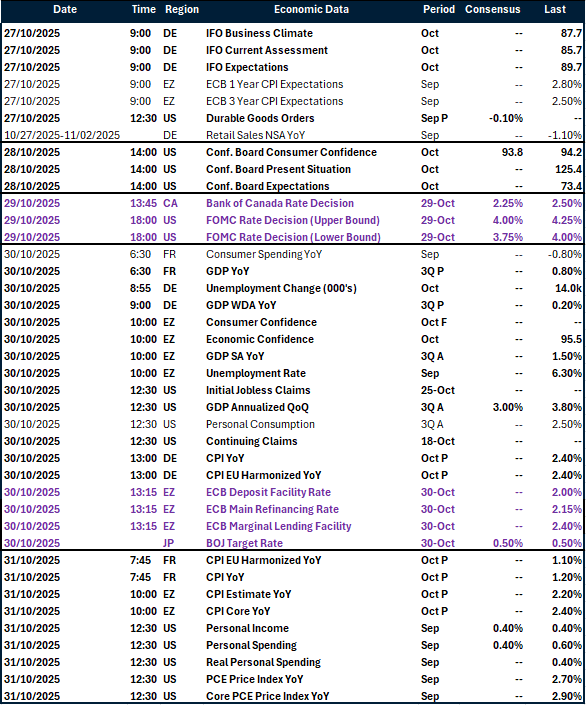

Key global risk events

Calendar: October 27-31

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.