Dollar’s global balancing act

The US dollar slipped against most G10 peers during Asian hours, as markets unwound risk-off positioning amid easing concerns over a near-term US military strike on Iran. The retreat comes as President Trump delays a decision on joining Israel’s offensive against Iran, which is now expected “within the next two weeks.”

Stepping away from the short-term dynamics though, let’s unpack the dollar’s rough ride in 2025. It hasn’t come out of nowhere, but a key part of the story that often gets overlooked is the country’s Net International Investment Position, or NIIP. Think of the NIIP like America’s financial scorecard with the rest of the world: how much it owns abroad versus how much the world owns in the U.S. And lately? The U.S. has been deep in the red; about $26 trillion, or nearly 80% of GDP. That means foreign investors hold way more American assets than Americans hold abroad. It’s a setup that works fine when confidence is high, but in shaky times like 2025, it can become a pressure cooker.

What we’ve seen this year is a textbook example of how a negative NIIP can magnify currency pain. Foreign investors, spooked by U.S. fiscal policy concerns and erratic U.S. trade policy, have started easing off their U.S. asset exposure. And because so much of the capital propping up the U.S. financial system comes from abroad, even small shifts in sentiment can lead to big outflows. That’s a lot of dollars being sold, and fewer being bought, and voilà, the greenback stumbles.

Now, what makes this more interesting is how it intertwines with valuation effects. Most of what Americans own abroad is in foreign currency; most of what they owe (the liabilities) is in dollars. So, when the dollar weakens, U.S. foreign assets look more valuable, on paper. Sounds like a win, right? But this boost doesn’t always keep up with real-world capital flight. And when equity and bond markets are turbulent, like they’ve been, it’s easy for the NIIP to deteriorate even further, feeding back into the dollar’s decline.

Many analysts focus narrowly on the current account deficit. That’s the measure of how much more the U.S. imports than it exports. And sure, persistent deficits matter. But they only show the flow of transactions. The NIIP shows the stock, or the mountain of accumulated claims and debts. Ignoring it is like judging someone’s spending habits without checking their credit card balance. When you’re that leveraged to the rest of the world, market trust becomes your most important asset, and that trust has wobbled this year.

So, if you’re trying to make sense of the dollar’s nosedive in 2025, particularly post April 2nd, look past the headlines. Yes, trade deficits, interest rates, and Fed signals all play a role, but the NIIP tells you just how exposed the U.S. is when things go sideways. It’s the quiet structural risk lurking under the surface, ready to amplify shocks. And in a year like this, it’s been shouting, not whispering.

BoE bides times, pound holds the line

The Bank of England (BoE) held rates steady at 4.25%, as expected, and gave little signal it’s ready to accelerate easing — despite a sharp deterioration in jobs data and the fading UK growth story. But while vote split and the accompanying minutes took a dovish tilt, sterling’s reaction was muted. Instead, the pound has reacted more to UK retail sales this morning, which came in below expectations by a large margin.

First, the BoE though. The voting pattern was the main surprise. It was largely expected to come in at 7-2 in favour of a hold. However, three MPC members voted for an immediate cut, prompting some speculation of a dovish turn. But past experience suggests vote splits offer limited guidance, and the Bank reiterated its “gradual and data-dependent” stance. Hence, we expect the BoE will retain its cut-hold tempo with 25bp cuts in August and November.

While the soft labour data strengthens the case for easing, officials remain wary of upside inflation risks. Oil prices have surged over 20% this month, and while this hasn’t materially altered near-term inflation expectations, memories of 2022’s energy-driven inflation cycle remain fresh. However, a looser labour market today reduces the risk of a wage-price spiral and makes a repeat less likely — barring another oil price shock.

Meanwhile, May’s retail sales figures has added to the weak UK data flow, despite the rise in consumer confidence to its highest since December. The report showed a 2.7% m/m drop – the largest since Dec 2023, which dragged the y/y figure to -1.3%, down from +1.3% in April.

In FX, GBP/USD bounced of its 50-day moving average yesterday, which we highlighted as a key support earlier this week, but downside pressure could persist if risk aversion stemming from Middle East tensions keep bubbling away. Meanwhile, GBP/EUR barely moved yesterday — a sign that markets were largely positioned for the BoE outcome.

Overall, while the BoE’s tone remains measured, the pound’s vulnerability to external shocks and weak domestic data reinforces our cautious GBP stance into the second half of the year.

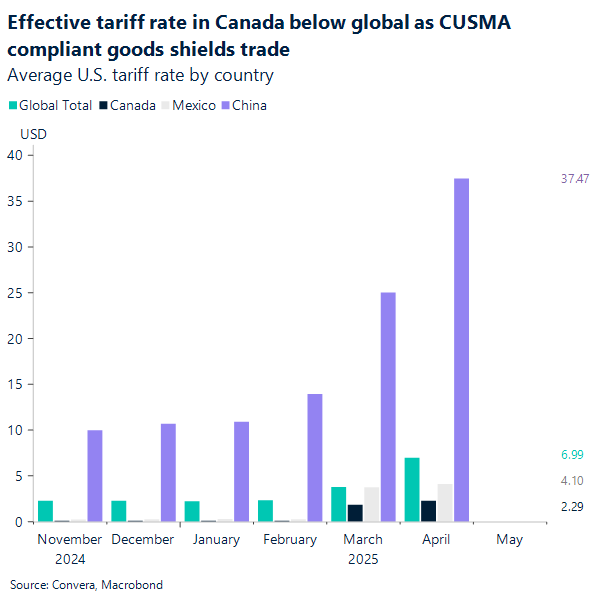

CUSMA and higher tariffs

Canada is weighing new tariffs on U.S. steel and aluminum as early as July 21, should trade talks with the Trump administration stall. At the same time, Ottawa is set to tighten federal procurement rules, mandating the use of domestic or “reliable partner” metals for infrastructure projects. To shield its industry further, Canada is rolling out tariff-rate quotas on steel from countries lacking trade agreements and drafting new anti-dumping measures.

These steps are part of a broader response to ongoing U.S. tariffs, 50% on foreign metals and targeted duties on Canadian steel, aluminum, and certain vehicles, which together account for over 8% of Canadian exports to the U.S. Canada currently applies 25% counter-tariffs. Both countries remain in negotiations, with a tentative mid-July deadline on the table.

While headlines often emphasize the U.S. administration’s 25% tariff on most Canadian imports (excluding energy products), the reality is more nuanced. Thanks to the Canada-United States-Mexico Agreement (CUSMA), many Canadian goods remain exempt from these broad tariffs.

In fact, as of April, the effective U.S. tariff rate on Canadian goods stood at just 2.3%, the lowest among major U.S. trading partners and one of the lowest globally. Nearly 90% of Canadian exports to the U.S. during that month entered the market tariff-free.

In FX, the Canadian dollar has rebounded, moving back above its 20-day moving average of 1.37. This recovery comes after a drop to 1.354, its lowest point since last October, bouncing from oversold levels. What’s more, the CAD has returned to a long-term upward support line that’s been in place since 2021, adding further weight to 1.37 as a key support/resistance level to watch in the near term.

Short-term movement in the CAD will likely be influenced by any escalation or de-escalation in the Israel-Iran conflict, as geopolitical tensions are leading market’s direction. Additionally, Canada’s May CPI report due next week could be another important catalyst for price direction.

Euro bruised but not beaten

The euro has retreated nearly 1% from its April highs of $1.1631, slipping into the $1.14 zone during Wednesday’s US session, but has reclaimed $1.15 on easing Middle East tensions (for now). With geopolitical tensions providing fresh support for the dollar, EUR/USD may face further downside pressure in the near term. A key variable remains US involvement—if it escalates, the commodity price channel could amplify dollar strength and prolong euro weakness.

The Fed’s hawkish stance is compounding the pressure. Let’s not forget: the euro’s recent rally has been almost entirely US-driven. Eurozone data has done little to offset the narrative, leaving Powell’s firm tone on Wednesday—and the Fed’s dismissal of near-term easing—as the dominant forces dragging the euro lower.

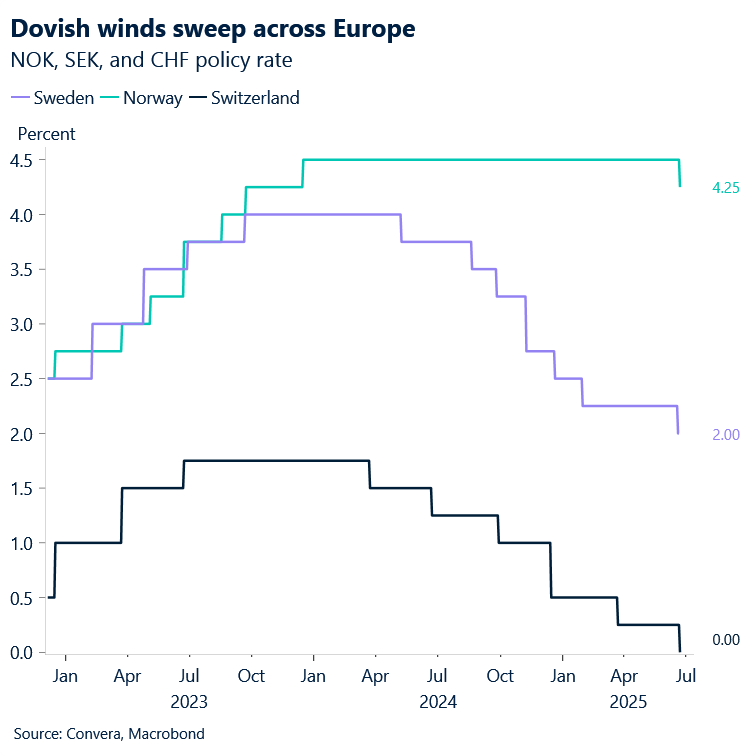

The broader macro backdrop was shaped by central banks yesterday. Three interest rate cuts in just over 24 hours across Europe – Switzerland, Sweden and Norway – as policymakers attempt to pre-empt the economic fallout from Donald Trump’s unpredictable trade agenda. The cuts stand in stark contrast to the wait-and-see approach from the Fed, Bank of Japan, and BoE. This cross-border dovish tone unfolds against a July 9 deadline that could see the US reimpose punitive tariffs globally. Combined with continued uncertainty over the war in Ukraine and the potential for a US strike on Iran, the three European central banks are signaling the potential for further rate cuts.

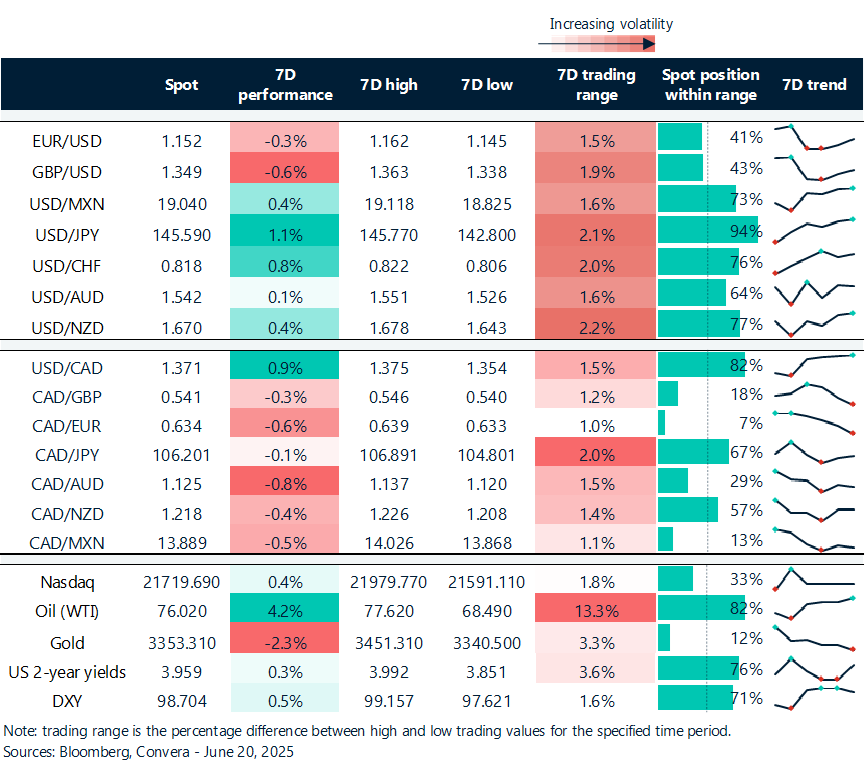

Traditional safe havens on the defensive

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: June 16-20

All times are in ET

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quote