USD: Fed liquidity trumps macro gloom

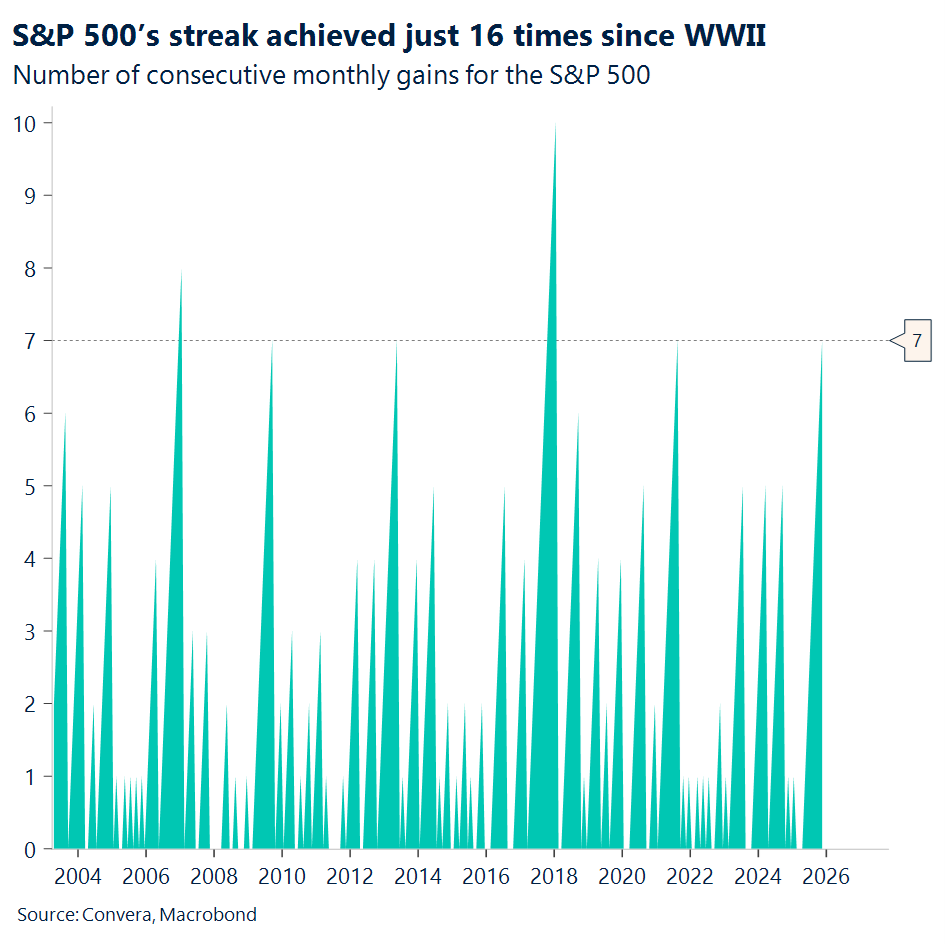

The resilience of risk assets is becoming impossible to ignore, most notably underscored by the S&P 500’s seven-month winning streak, a milestone achieved only sixteen times since World War II. Fueling this momentum is a distinct shift in liquidity dynamics, with the Federal Reserve officially concluding Quantitative Tightening on December 1 and simultaneously injecting $13.5 billion into the banking system via overnight repurchase agreements. This operation, the second largest since the pandemic and surpassing peaks seen during the Dot-Com bubble, suggests that the financial “plumbing” is now primed to support further risk-taking. However, this asset buoyancy sharply contrasts with a softening macro backdrop, where investors are increasingly pricing in a December rate cut, a conviction deepened by weak ISM data and the Beige Book’s reports of uneven economic activity and a cooling labor market.

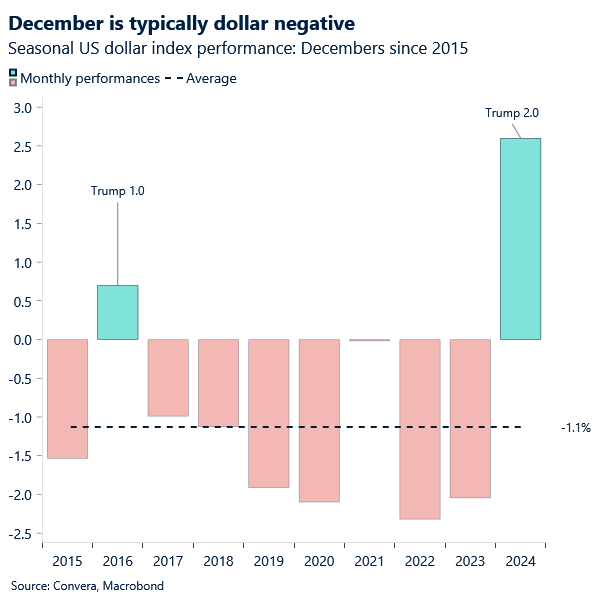

This expectation of monetary easing converges with a powerful seasonal headwind for the US currency. December has notoriously been the Dollar’s cruelest month, with the broad index suffering declines in eight of the past ten years. The current setup seems destined to rhyme with history, as easing geopolitical anxiety and firm risk appetite drag capital away from the greenback’s safe-haven appeal. The market’s gaze is now fixed squarely on Federal Reserve Chair Jerome Powell, specifically looking for any signaling regarding a sub-3% terminal rate. If the Fed acknowledges the cooling data with a dovish tilt, it would reinforce the seasonal pressure on the Dollar, leaving it vulnerable to a continued slide as we close out the year.

Beyond immediate monetary policy, the medium-term outlook is clouded by the complex legal and political maneuvering surrounding trade policy. The narrative regarding tariffs appears binary on the surface, yet a closer inspection reveals that both potential outcomes from the Supreme Court lean bearish for the long end of the bond market. If the President retains authority under the International Economic Emergency Powers Act (IEEPA), inflation is likely to remain sticky due to inventory depletion and cost passthrough, a reality seemingly confirmed by the Walmart CFO’s expectation of peak tariff impacts hitting in early 2026. Conversely, if the high court strips this authority, the administration would likely pivot to Section 301 investigations or flat reciprocal duties to achieve similar ends, meaning the protectionist agenda survives regardless of the legal vehicle used.

These trade dynamics are creating a dissonance within the Treasury market, where the yield curve is currently stuck in a range that struggles to price the developing reality. There is a palpable collision between the market’s hope for a dovish Fed in 2026 and the fiscal reality of a deficit overhang combined with sticky inflation. If the Supreme Court limits executive tariff power, Washington faces a larger fiscal hole, incentivizing greater debt issuance that further pressures the long end of the curve. Consequently, the Treasury market is left navigating a disconnect where yields may need to rise to attract buyers, irrespective of the central bank’s rate-cutting ambitions.

Ultimately, this confluence of factors creates a complicated environment for the US Dollar. A steeper yield curve, exacerbated by the threat of unanchored inflation and renewed worries about political interference at the central bank, serves as a clear negative for the currency. The Dollar has yet to fully recover from the initial shock of tariff headlines, and it now faces the compounding weight of pending Supreme Court rulings, including the decision in the Lisa Cook case. With the “tariff story” likely to result in either higher inflation or higher deficits, the path of least resistance for the Dollar appears lower, trapped between seasonal weakness and structural fiscal headwinds.

EUR: Eying up a crucial closing price

Witkoff arrived in Moscow yesterday to discuss a revised Ukraine peace plan, with Zelenskyy calling the proposal “better now” and Putin showing openness last week. Markets remain hopeful, watching for concrete steps, with high‑beta European currencies and the euro set to benefit via the lower oil price channel on more substantial progress.

That said, Putin has offered no sign of easing Russian demand, while claiming advances in Donetsk yesterday, which Ukraine disputes. Any battlefield gains underscore his insistence that Kyiv surrender the region, raising doubts about the immediacy of a deal.

On the macro front, eurozone headline CPI y/y came in above expectations at 2.2% versus 2.1%, while core y/y was steady at 2.4%. The higher inflation rate was mainly driven by a smaller negative contribution from energy prices. While downside risks to inflation remain intact in the months ahead, yesterday’s print clearly does not create any urgency for further easing at this stage. As anticipated, the FX response was muted.

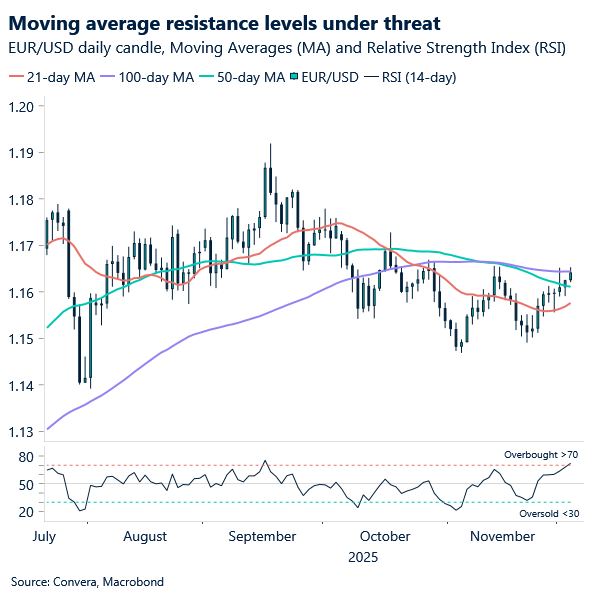

The euro was broadly flat versus the dollar on Tuesday, but has since pushed above the 1.1630 resistance due to broad-based dollar weakness. A sustained close above the 50- and 100‑day moving averages at 1.1611 and 1.1644 respectively would mark a short‑term bullish signal, challenging the pair’s bearish technical downtrend in place since mid September. Keep an eye on US industrial production and ADP labour market data today, which could push the pair to challenge that resistance if they deliver a meaningful miss.

GBP: Sterling’s tactical range

Sterling is under pressure against most of its G10 peers this week, underscoring how the post‑Budget bounce has failed to gain lasting traction. The exception remains the US dollar: broad‑based USD weakness has allowed GBP/USD to hold above the $1.32 handle, even as sterling softens elsewhere.

Short covering and December’s favourable seasonality offer sterling bulls a potential path toward $1.34. Yet sustained upside remains conditional, with the pound’s resilience ultimately tied to broader USD trends. If dollar weakness fades into 2026, sterling’s gains are likely to stall.

From a technical perspective, GBP/USD’s 21‑day moving average is bending higher, reinforcing a short‑term upside bias. However, the climb toward $1.34 is crowded with resistance, as a confluence of key moving averages is likely to act as barriers. This sets up a tactical range where dollar dynamics, rather than UK fundamentals, are the primary driver of sterling’s performance.

Still, the UK Budget’s fuel‑duty freeze and measures to reduce household energy bills introduce a disinflationary bias, reviving the prospect of a December BoE rate cut and reinforcing expectations of a more dovish policy trajectory into 2026. This shift matters at a time when growth and yield differentials are set to be the prime drivers of G10 FX.

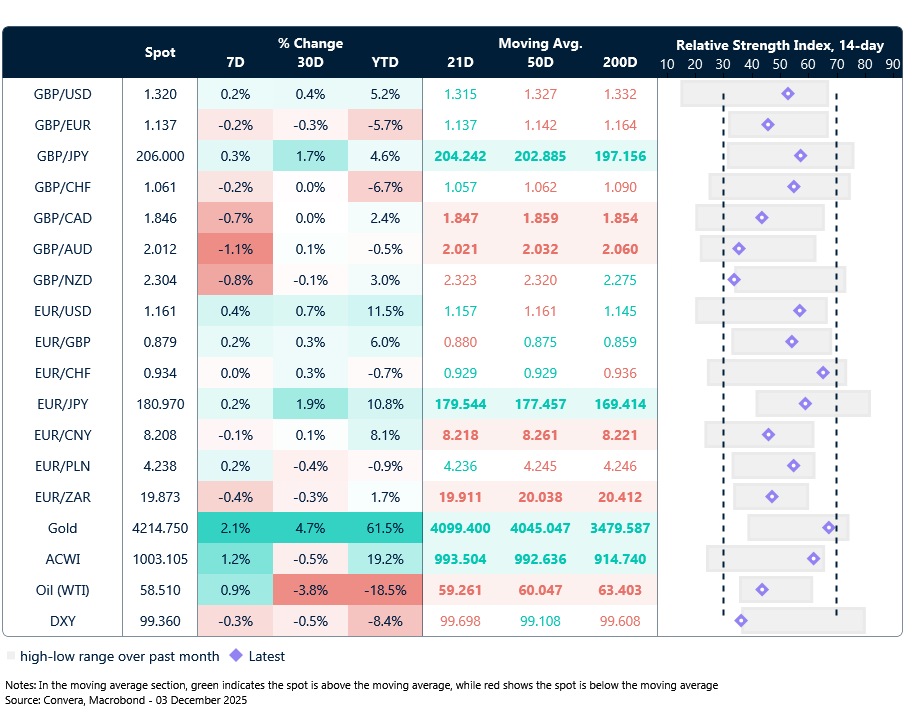

Market snapshot

Table: Currency trends, trading ranges and technical indicators

Key global risk events

Calendar: December 1-5

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.