USD: Dollar gains but conviction still lags

The US dollar started the week firmer against its major peers, helped by a modest rise in yields and a fresh jump in oil after renewed Middle East headlines. That said, the broader market tone has not changed much from May. US equity futures softened early on the Iran news, but the move still looks more like a knee-jerk reaction than a real shift in sentiment. Investors have seen several similar headlines in recent weeks, and markets have largely looked through them. With the S&P 500 and Nasdaq 100 closing at new record highs on Friday, and tech stocks still providing a strong tailwind for risk appetite, the focus is likely to swing back quickly to this week’s US data calendar and Friday’s May jobs report.

Even with the dollar ticking higher, the bigger technical picture for DXY still looks restrained rather than convincingly bullish. The index is trading near 99, which keeps it below the 20-month moving average at 100.94 and the 50-month moving average at 103.05. It is also still struggling just under the 100-month moving average near 99.70, an area that is acting as nearby resistance. In other words, after the sharp drop from the late-2024 highs near 109, the dollar appears to be stabilizing, but not yet breaking out. Unless DXY can reclaim 99.70 and then push through 100.94, rallies may continue to look more like range-bound recoveries than the start of a stronger uptrend.

That cautious technical view fits the macro backdrop. Recent US data have been mixed in a way that does not offer the dollar a clean bullish story. First-quarter GDP was revised lower again, personal income was flat in April, and real incomes have declined in five of the past seven months. At the same time, personal spending still rose 0.5%, suggesting households may be leaning more on savings to keep consumption going. Inflation remains sticky enough to keep pressure on purchasing power, especially for middle- and lower-income households, while softer core capital goods orders hint at some business caution too. Put simply, the US economy still looks resilient in pockets, but not decisively strong across the board, which helps explain why the dollar is finding support without yet building sustained upside momentum.

What’s happening in markets this week?

Markets start the week with geopolitics front and center, as developments around US‑Iran tensions and Israel’s expanding operations in Lebanon (Mon) keep risk sentiment fragile and energy markets on edge. Attention then shifts quickly to central bank signals, with policymakers across major economies likely to reinforce a growing divergence theme (Tue–Wed). The US economy continues to show resilience, but sticky inflation and elevated expectations complicate the Federal Reserve’s path, especially with leadership transition dynamics and a divided FOMC in play. As a result, markets will parse every speech and commentary update for clarity on how officials plan to manage persistent inflation alongside strong growth.

Data takes over in the second half of the week, shaping the macro narrative and testing the “US exceptionalism” thesis. Key releases include US JOLTS and ISM manufacturing (Tue), followed by ISM services and jobless claims (Wed–Thu), before the pivotal US jobs report (Fri) sets the tone into next week. Globally, Eurozone CPI and growth data (Wed–Thu), along with China Caixin PMIs and Australia GDP (early week), will offer a read on the broader slowdown. Canada employment (Fri) also adds regional focus.

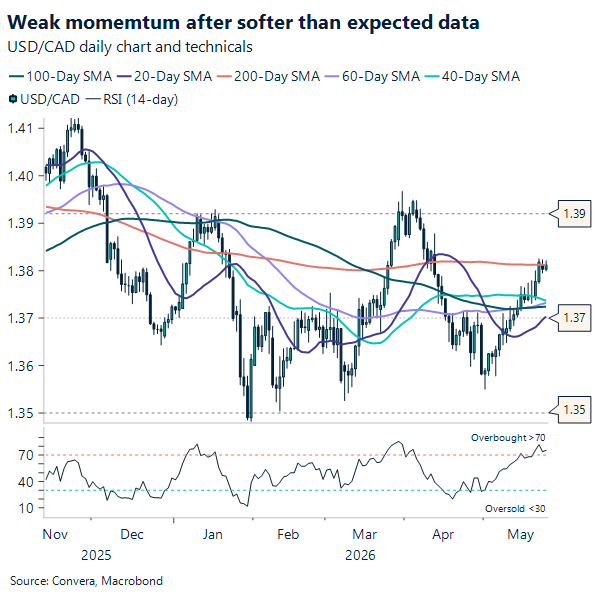

CAD: Weak momentum

Canada’s economy has now slipped into a technical recession, with real GDP falling 0.1% annualized in Q1 2026 after a 1.0% annualized drop in Q4 2025. That Q4 print was also revised down from -0.6%, which makes the downturn look deeper than first thought. Just as important, the Q1 result missed the roughly 1.5% market consensus by a wide margin. In short, is underperforming expectations in a more meaningful way.

The headline detail is that higher oil prices helped nominal income, but they did not stop the real economy from weakening. Corporate incomes rose 1.6%, and the terms of trade improved as commodity prices moved higher. However, that support was not broad enough. Export gains in energy were offset by weakness in more trade-sensitive sectors, especially autos, where US tariff friction remains a drag. So, while the energy shock lifted income, it did not generate enough momentum to keep output growing.

The bigger problem sits at home. Final domestic demand dipped 0.1%, business fixed investment fell 3.0% annualized, and the household saving rate fell to 3.5%, a two-year low. That mix points to softer demand, more cautious firms, and households leaning more on dissaving as energy-related price pressure eats into purchasing power. Taken together, the message is clear: commodity support is cushioning the economy, but it is not strong enough to offset weaker domestic demand and fading investment. That leaves Canada entering mid-2026 with a fragile growth backdrop.

For the Canadian dollar, that softer domestic story still argues for caution. Last week, renewed Middle East tensions kept risk appetite uneasy, while the US–Canada 2-year spread near 120bp continued to favor the US dollar on carry. Even so, weaker US spending data and a downward GDP revision narrowed that advantage a bit and gave the Loonie some breathing room after USD/CAD reversed from its weekly and monthly high at 1.387. The pair has moved back above the 20-day, 50-day, and 100-day moving averages and is now testing the 200-day near 1.3811. That is the key level to watch. A sustained break higher would open the door to a retest of 1.3870 and possibly 1.39, while failure there would likely consolidate above 1.375.

MXN: Consolidation continues

Last week’s MXN tone softened a touch as the USD caught a bid after hotter-than-expected US inflation and resilient retail sales reinforced the “higher-for-longer” Fed narrative, which tends to lean against high-carry EM FX. Layered on top, S&P’s decision to revise Mexico’s outlook to negative (while affirming the BBB/BBB+ ratings) added a mild fiscal-risk headline to the mix, with the agency essentially flagging that slow growth and rigid spending could make debt dynamics less forgiving if consolidation disappoints. Put together, it’s not a shock that the peso gave back a bit of ground, last week felt less like a Mexico-specific unwind and more like a modest repricing of global rates and risk, with a fiscal footnote that investors can’t completely ignore.

On the chart, USD/MXN is still trading within the broader downtrend, even with last week’s small bounce. Spot is around 17.3, and it remains below the 20/50/100/200-day moving averages at approximately 17.3 / 17.5 / 17.5 / 17.9, which keeps the medium-term technical bias pointed lower for the pair (i.e., still constructive for MXN) unless price can reclaim the short-term averages. Near-term support sits around 17.16–17.10, then the psychological 17.00 area; a clean break lower would re-affirm momentum. On the topside, the first real “line in the sand” is the 20-day near 17.34, and above that the 17.5 zone (50/100-day convergence) is the bigger resistance band.

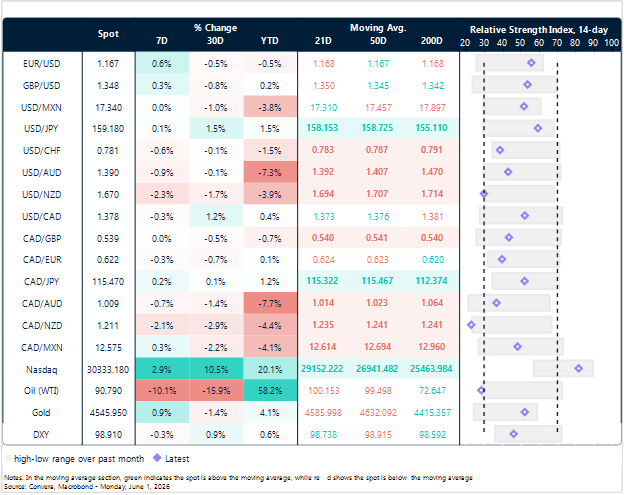

Market snapshot

Table: Currency trends, trading ranges & technical indicators

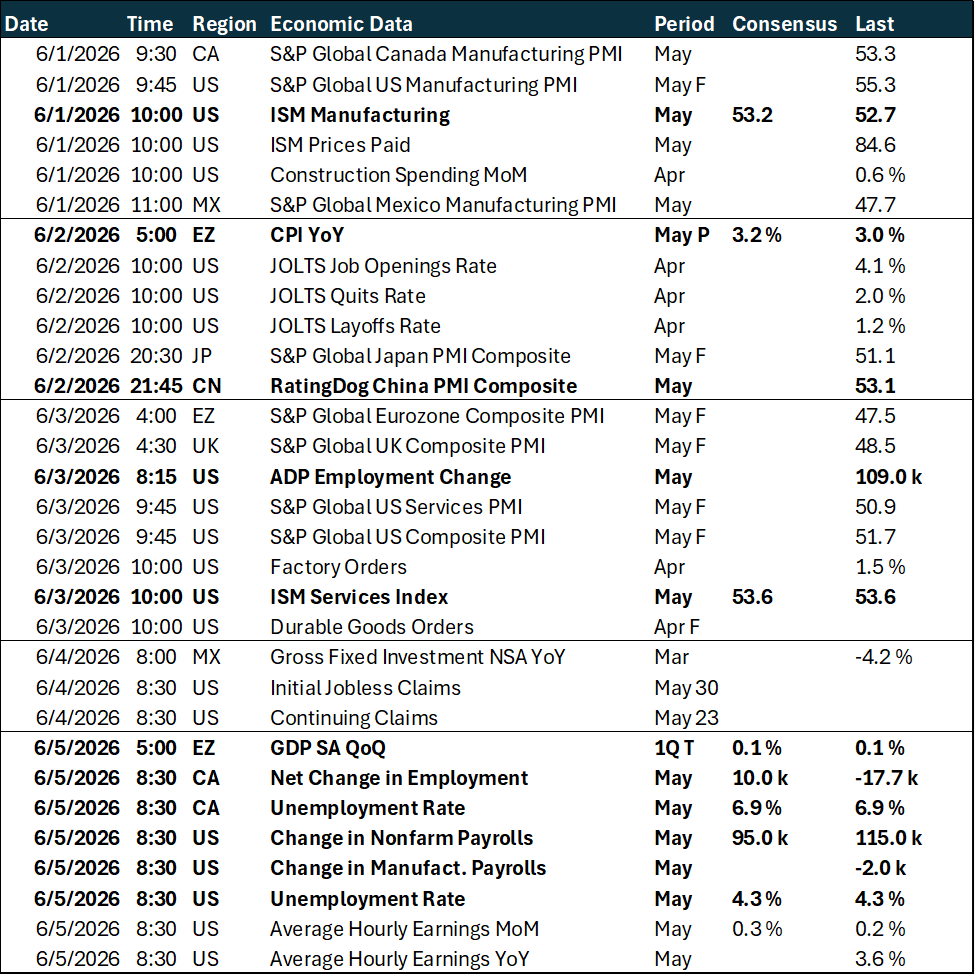

Key global risk events

Calendar: June 01 – 05

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.