USD: Dollar firms as oil risk builds

The US dollar opened the week firmer against its major peers, helped by a modest rise in yields and a sharp rebound in oil after renewed Middle East headlines. Even so, the broader market tone still feels a lot like May, with equities mostly looking through the geopolitical noise while oil and rates react more immediately. However, the move in the dollar looks more like a headline-driven lift, keeping a price action pattern of a Dollar not moving in lockstep with oil for some time. The main question is whether June brings another round of markets absorbing the tension and moving on, even as hopes for a deal keep running into the same stalemate.

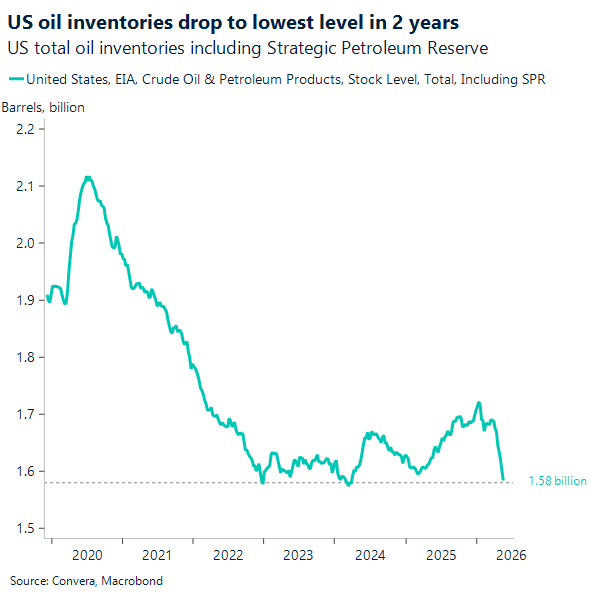

Oil is the bigger story to start the week, with WTI up about 7% and Brent up roughly 6%. Markets are reacting to fresh uncertainty around US-Iran talks, recent military exchanges involving US interests, and Israel’s expanding ground offensive in Lebanon. At the same time, as US total oil inventories decrease, markets may have less buffer if disruptions drag on. A deal may still be close, but that has been the message for weeks, and traders are putting more weight on the risk that disruption lasts longer than expected. As long as that remains the backdrop, energy is likely to keep inflation pressure elevated.

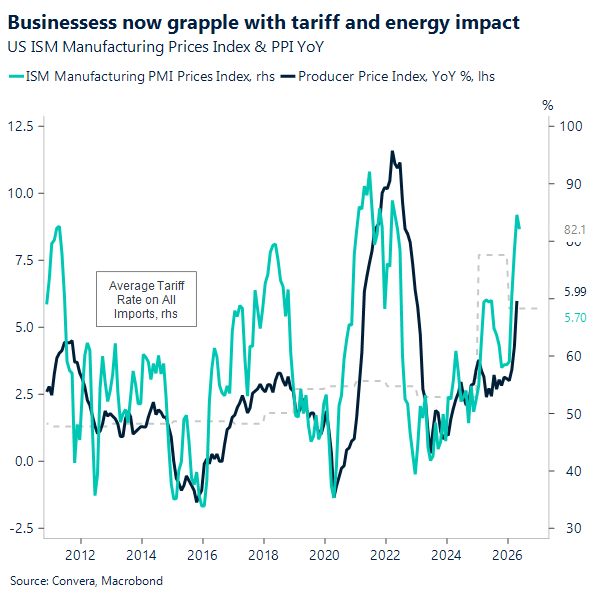

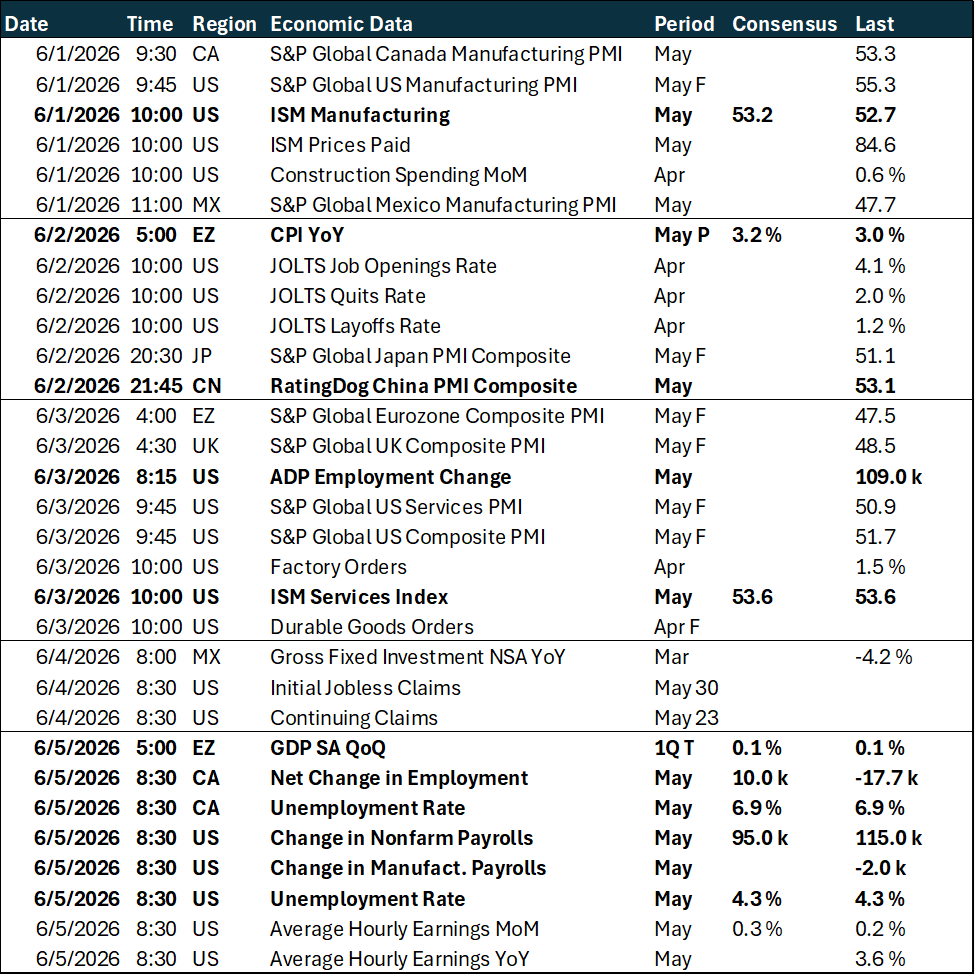

On the data side, the May ISM manufacturing report was better than expected. The headline index rose to 54.0 from 52.7, above the 53.0 consensus, while new orders climbed to 56.8 from 54.1. The release also showed prices paid stayed very high at 82.1, even if that was a touch below April’s 84.6. In simple terms, activity improved, but price pressure in the factory pipeline is still intense.

That mix gives the Fed room to keep a hawkish bias, with markets still leaning toward a long hold and seeing the next move as more likely to be a hike than a cut. Still, the details under the headline are less reassuring. Demand has been running ahead of inventories for months, and survey responses suggest some firms are questioning how long this pace can last. Manufacturing is expanding, but it is doing so in a cost environment that is becoming harder to absorb.

That is why investors should be careful about reading too much into the strong headline or the AI-driven boost to activity. Business momentum has helped support the economy, but if energy stays high and inflation remains sticky, the expansion could start to overheat rather than broaden in a healthy way. The dollar is getting some near-term support from that mix, but the medium-term outlook still depends on whether growth can hold up without inflation damaging demand. Right now, the signal is not a clean dollar bull story, while FX markets remain reluctant to fully price a more lasting geopolitical shock.

CAD: Weak momentum ahead of CUSMA review

Canada’s economy has now slipped into a technical recession, with real GDP falling 0.1% q/q SAAR in Q1 2026 after a 1.0% annualized decline in Q4 2025. That Q4 print was also revised down from -0.6%, making the downturn look deeper than initially thought. Just as importantly, the Q1 result missed the roughly 1.5% market consensus by a wide margin.

The composition of growth was also soft. Headline demand declined 0.4% q/q SAAR, with weakness driven primarily by a worsening trade balance and sharp declines in both residential and non-residential investment. Higher oil prices did provide some support through improved terms of trade and firmer nominal income, with corporate incomes rising 1.6%, but that support was not broad enough to offset weakness elsewhere. Export gains in energy were counterbalanced by softness in more trade-sensitive sectors, especially autos, where ongoing US tariff friction remains a drag. In other words, the commodity backdrop helped cushion income, but it did not generate enough momentum to keep real activity expanding.

The bigger problem remains at home. Final domestic demand dipped 0.1%, business fixed investment fell 3.0% annualized, and the household saving rate dropped to 3.5%, a two-year low. At the same time, cyclical headwinds are becoming more visible: debt servicing costs are rising, confidence is softening, and the labor market is losing momentum, with payroll employment falling by 32k in March. While the Bank of Canada’s latest Financial Stability Report suggests that higher rates have so far had only limited pass-through to mortgage arrears, the broader macro picture still points to softer demand, more cautious firms, and households leaning more heavily on dissaving as energy-related price pressure erodes purchasing power. Taken together, the commodity support is cushioning the economy, but it is not strong enough to offset weaker domestic demand, deteriorating trade dynamics, and fading investment. That leaves Canada entering mid-2026 with a fragile growth backdrop and a weaker macro-outlook relative to peers.

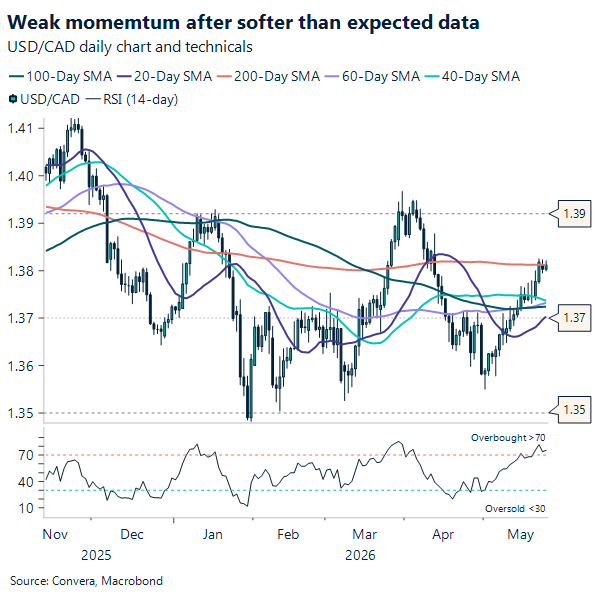

For the Canadian dollar, that softer domestic story continues to argue for caution. Starting this week, renewed Middle East tensions kept risk appetite uneasy, while the US–Canada 2-year spread near 120bp continued to favor the US dollar on carry. Even so, weaker US spending data and a downward GDP revision narrowed that advantage somewhat and gave the Loonie some breathing room after USD/CAD reversed from its weekly and monthly high near 1.387. The pair has moved back above the 20-day, 50-day, and 100-day moving averages and is now sitting above the 200-day near 1.381, which remains the key level to watch. A sustained break higher would open the door to a retest of 1.3870 and possibly 1.390, while failure there would likely leave the pair consolidating above 1.375.

From a policy perspective, the weak growth backdrop strengthens the case for the Bank of Canada to remain on hold through 2026. Near-term, upcoming labor market and PMI releases should provide additional clarity on whether domestic weakness is deepening, while attention is also likely to shift toward CUSMA negotiations in the weeks ahead as another potential source of uncertainty for the outlook.

MXN: Consolidation continues

Last week’s MXN tone softened a touch as the USD caught a bid after hotter-than-expected US inflation and resilient retail sales reinforced the “higher-for-longer” Fed narrative, which tends to lean against high-carry EM FX. Layered on top, S&P’s decision to revise Mexico’s outlook to negative (while affirming the BBB/BBB+ ratings) added a mild fiscal-risk headline to the mix, with the agency essentially flagging that slow growth and rigid spending could make debt dynamics less forgiving if consolidation disappoints. Put together, it’s not a shock that the peso gave back a bit of ground, last week felt less like a Mexico-specific unwind and more like a modest repricing of global rates and risk, with a fiscal footnote that investors can’t completely ignore.

On the chart, USD/MXN is still trading within the broader downtrend, even with last week’s small bounce. Spot is around 17.3, and it remains below the 20/50/100/200-day moving averages at approximately 17.3 / 17.5 / 17.5 / 17.9, which keeps the medium-term technical bias pointed lower for the pair (i.e., still constructive for MXN) unless price can reclaim the short-term averages. Near-term support sits around 17.16–17.10, then the psychological 17.00 area; a clean break lower would re-affirm momentum. On the topside, the first real “line in the sand” is the 20-day near 17.34, and above that the 17.5 zone (50/100-day convergence) is the bigger resistance band.

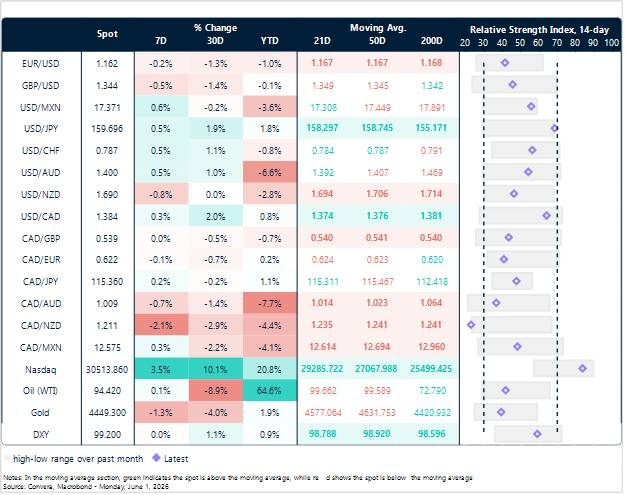

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

Calendar: June 01 – 05

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.