USD: Dollar rebound ends turbulent January

The dollar spent most of January on the back foot, slipping to a four‑year low near 95.8 on the DXY, before stabilizing into month‑end as the market narrative shifted from geopolitical fears to monetary policy. Following the Fed’s decision to maintain the target range at 3.50%–3.75% on January 28—and Chair Jerome Powell’s reminder that his term concludes in May—President Trump nominated former Fed governor Kevin Warsh to succeed him. This selection of an experienced insider provided initial support to the greenback, a tone that was solidified by a hotter‑than‑expected December Producer Price Index. The data nudged investors away from expectations of early‑2026 rate cuts, forcing a reconsideration of the dollar’s trajectory against a backdrop of unfinished inflation work. Ultimately, while the month did not signal a complete macro reversal, the combination of a credible Fed successor, sticky inflation data, and a sharp position clean‑up in precious metals was enough to lift the dollar from its lows, leaving rate‑sensitive assets volatile and the long end of the Treasury curve demanding a higher premium.

Warsh’s selection sets up a credible‑but‑flexible policy mix, though he enters the fray facing major economic crosscurrents: a President demanding lower rates while sticky inflation remains a “thorn” for the public, and a stagnant job market where the benefits of expansion are skewed toward the top higher-income households. His mentor Stanley Druckenmiller noted Warsh’s primary challenge will be expanding the economy amid an AI boom without reigniting inflation. In his first stint at the Fed he built a hawkish reputation and was skeptical of expansive QE—positions that cemented his inflation‑first credentials—yet more recently he has argued for “regime change” at the central bank, emphasizing credibility and independence while signaling openness to lower policy rates alongside a smaller balance sheet.

Markets appear to be penciling only modest easing later this year rather than a rapid cutting cycle, broadly consistent with recent Fed communication that any moves will be data‑dependent and likely later in 2026 rather than immediate. However, confirmation is not guaranteed, as Senator Thom Tillis has vowed to block the process until the DOJ probe into the current Chair is resolved, citing the need to protect central bank independence.

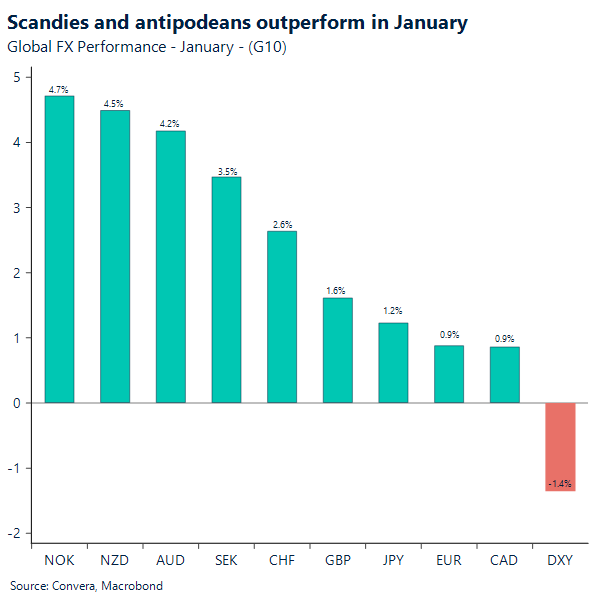

Rates and FX markets immediately digested these crosscurrents, telling a story of rapid repricing into month-end. The dollar firmed following the Fed’s hold and the Warsh nomination, holding those gains as longer maturity Treasury yields nudged higher on re-priced inflation risk, while the front end remained anchored by the Fed’s “wait-and-see” stance. In G10 FX, the early‑January leadership from “risk‑on” currencies—AUD, NZD, NOK, and SEK—faded as the greenback steadied, reversing part of the month’s initial drawdown. Commodities delivered the most dramatic reaction to this shift; after setting record highs, gold and silver unwound sharply, with silver posting a massive intraday fall driven by crowded positioning and a stronger dollar. Bitcoin dropped below $80,000 for the first time since April 2025, highlighting that cross‑asset correlations remain unstable when the dollar regains a bid.

The week ahead will rigorously test the theme of policy divergence and the pulse of global growth. The ECB and Bank of England are expected to hold policy on Thursday, while the RBA is widely tipped to hike after upside surprises in Australian inflation—an asymmetry that keeps the AUD particularly sensitive. In the U.S., the data calendar is heavy with ISM Manufacturing (Mon) and Services (Wed), followed by the mid-week ADP report and Friday’s pivotal January employment data; consensus expects 40k payroll gains with unemployment in the mid‑4s, though wage revisions will be key for policy. Corporate results will add vital macro color on consumer demand and capex, with Disney reporting Monday, followed by Alphabet on Wednesday, and Amazon on Thursday.

EUR: Cyclical cheer, structural fear

Last week ended on an overall upbeat macro note, with eurozone GDP growth confirmed at 0.3% QoQ in 4Q 2025 – largely driven by accelerating activity in Germany, Spain and Italy. Of course, the data is backward‑looking, but if we linger on what recent sentiment indicators have been signalling – the European Commission’s economic sentiment index hitting a three‑year high as an example – then the narrative points uphill from here. Germany’s defence and infrastructure investment plans may be contributing, along with a period of relative tariff tranquillity.

The big question is whether these cyclical, growth‑supportive forces eventually collide with Europe’s well‑known structural obstacles. Risks remain that the economic resurgence proves more subdued than many anticipate, dampening sentiment as the year progresses and ultimately weighing on the euro – especially if its archenemy, the dollar, benefits from a relatively stronger, AI‑powered US economic performance. These dynamics matter even more this year, as macro‑implied FX price action has taken on a more sentiment‑driven character. The effect is amplified by the US adopting a more defensive, independent stance that can sharpen divergence in economic trajectories and feeds, therefore, more forcefully into FX. In a more globalised past, one could argue that FX moves tied to relative economic performance were more subdued, as US economic strength typically acted as a precursor to global growth too – but times are certainly changing.

For the week ahead, expectations are for yet another quite boring ECB meeting, with the policy path likely to remain steady for the entire year, most probably. More instructive may be the raft of macro releases across key eurozone members. Given that much is expected from Germany, especially those forward‑looking indicators – factory orders, for example – will be closely scrutinised for any early‑year transition from recent upbeat sentiment to hard‑line economic momentum.

Our bias remains for EUR/USD to slip back under 1.18 in the coming days/weeks, as the pair gravitates toward its familiar 1.15–1.18 corridor.

GBP: Dollar story gives way to BoE week

Sterling’s recent moves have been driven far more by the dollar than by anything happening at home. Last week, GBP/USD broke above $1.38 to reach fresh four‑year highs as broad USD weakness intensified. But that momentum quickly reversed: Friday’s announcement of Kevin Warsh as the next Fed Chair triggered the pound’s largest daily drop since early November, pulling the pair back below $1.37 and prompting markets to scale back bullish bets. Even so, GBP/USD continues to trade above its key daily and weekly moving averages, suggesting underlying momentum remains constructive.

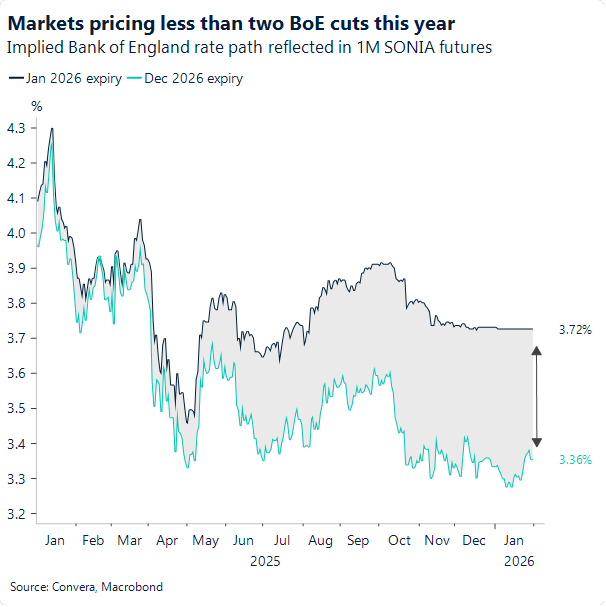

This week, however, the domestic narrative comes back into focus with the Bank of England’s policy meeting. The BoE is widely expected to keep rates unchanged, but the real story lies in the medium‑term guidance. Markets still anticipate further cuts, though the timing remains contentious. A deeply divided MPC means the vote split may prove more revealing than the decision itself. Any firm resistance from the more dovish members — even as the Bank stands pat — would hint at growing urgency for additional easing, marking a shift from the cautious approach seen so far.

Recent data since the December meeting offers a touch of reassurance on inflation persistence, particularly in the labour market. Private‑sector regular pay growth, the MPC’s preferred wage metric, slowed to 3.6% in the three months to November, slightly below the Bank’s latest projections. That moderation may help ease some of the committee’s concerns, but it is unlikely to settle the debate over how quickly policy should be loosened.

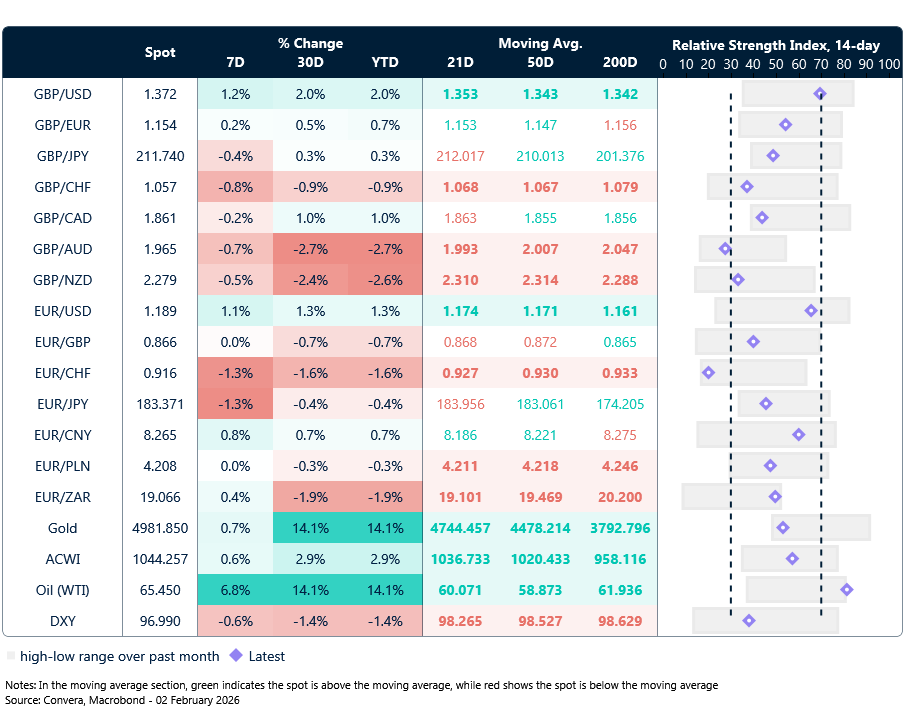

Market snapshot

Table: Currency trends, trading ranges & technical indicators

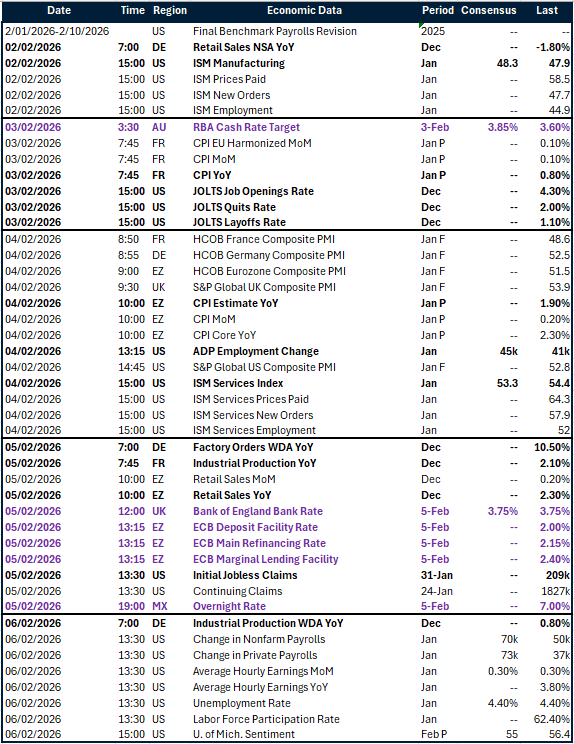

Key global risk events

Calendar: February 2-6

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.