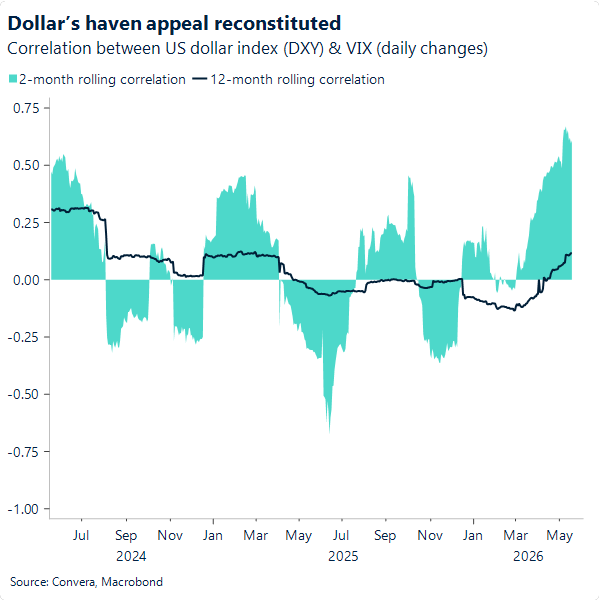

USD: Emboldened safe-haven bid

Markets are becoming increasingly desensitised to headlines surrounding the conflict in the Middle East. Speaking to reporters on Wednesday morning, President Trump indicated he is in no hurry when it comes to Iran, contradicting a potential two- or three-day deadline he had suggested less than 24 hours earlier for further strikes on the Islamic state. Meanwhile, Iran warned it would retaliate beyond the Middle East if the US or Israel were to attack again. Oil and the US dollar appeared less responsive to such bouts of re-escalation.

Markets appear to have consolidated around the view that both sides are unwilling to recommit to exchanges of fire on the same scale as seen earlier in March and that, despite the noise, there continue to be trickles of news suggesting negotiations remain ongoing. The US dollar dipped 0.2% lower yesterday as oil prices declined, lower on the week so far, with Brent crude hovering near $106 a barrel.

Yet the dollar’s trajectory is likely to remain upward unless a meaningful de-escalation in the conflict materialises. The currency has reinforced its safe-haven bid since tensions in the Middle east escalated. Amid inflation-led tightening financial conditions and fragile, AI-fuelled equity sentiment the dollar’s safe-haven appeal may have further room to run the longer the conflict persists, beyond a purely mechanical lift from higher oil prices.

Then there is the Fed, with the minutes of the April 29–30 FOMC meeting, released yesterday’s evening (BST), showing the stance shifting further in a hawkish direction. Support for eventual cuts narrowed, with “many” participants willing to drop the easing bias. There is nothing particularly new there; however, dollar buyers may have hoped to hear more discussion around the possibility of a hike. But the overall message was that policymakers are comfortable with the current stance for now, and that further firming would be appropriate only if inflation were to remain persistently above 2%.

The dollar index (DXY) has re-entered the 99 handle, a level not properly visited since the peak of the conflict back in March. Once again, despite the US-Iran ceasefire broadly still holding, the reinforced safe-haven bid in the dollar – alongside pressure across global bond markets – helps justify the move higher. We expect further upside from here in the absence of any substantive developments on the peace front in the coming days.

EUR: Downside bias builds

EUR/USD sits broadly flat relative to the start of the week, as the recent bond market sell-off – the latest expression of geopolitically driven risk-off sentiment – has taken a breather. Further upside in yields remains closely tied to additional hawkish signals emerging from central bank outlooks.

With markets having already priced in a significant degree of hawkish repricing – nearly three ECB hikes and around a 70% probability of one Fed hike by year-end – yields are understandably pausing. A renewed move higher would likely require not only a re-escalation in headlines and oil prices, but also validation from the inflation backdrop to justify investors’ fears. Last week’s upside surprises in US CPI and PPI, which acted as a trigger for the recent bond selling pressure, are a useful case in point.

Equally, the resilient US macro backdrop – crucial to the recent pressure at the long end – remains structural, tempering the extent to which any rise in yields is likely to reverse in the absence of meaningful geopolitical de-escalation.

Amid such tightening conditions and the emboldened safe haven bid in the dollar, there is little the euro can do to defend itself. The eurozone’s macro backdrop and outlook remain poor, while its high energy dependency feed growth fears that weaken the currency on souring geopolitical headlines but increasingly to rising risk premium in bond markets.

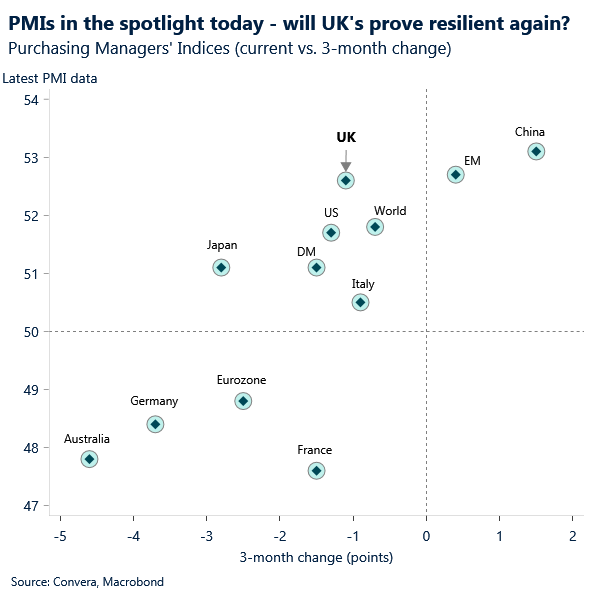

We continue to call for further downside toward 1.16 should uncertainty around the de-escalation path in the Middle East persist. Today sees the release of May’s preliminary PMI prints, which are expected to show a relatively orderly outcome compared to April. We doubt this will move the euro significantly, even in the event of a miss, as the ECB has already revised down its growth forecasts for the year and expectations for further drag are building.

GBP: Supported by risk not rates

Sterling has strengthened against most major peers this week despite a softer domestic backdrop. GBP/USD has moved back above 1.34 and GBP/EUR above 1.155, both up close to 1% week‑to‑date, even as weaker UK jobs data and softer‑than‑expected inflation have prompted a modest trimming of Bank of England rate expectations.

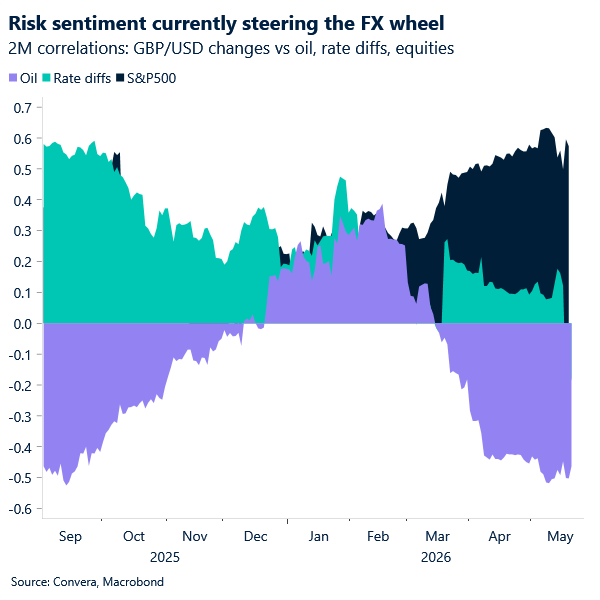

With UK yields declining relative to peers, the rates channel has not been the primary driver of GBP strength. Some support may have come from a continued unwinding of the political risk premium following Andy Burnham’s commitment to fiscal discipline, but the dominant impulse has been external. Specifically, improving global risk sentiment and declining oil prices, driven by renewed optimism around a potential US–Iran resolution, have lifted the pound.

The divide in drivers remains clear: GBP/USD continues to trade off geopolitics and energy dynamics, while GBP/EUR is more sensitive to domestic political developments. Technically, downside levels at 1.33 in GBP/USD and 1.145 in GBP/EUR have been tested but held, suggesting these may define near‑term lows absent renewed escalation.

Attention now turns to UK flash PMIs, which have become a key barometer of emerging stagflation risks. With UK data surprising positively relative to peers in recent weeks, any further resilience here could provide incremental support to sterling at the margin.

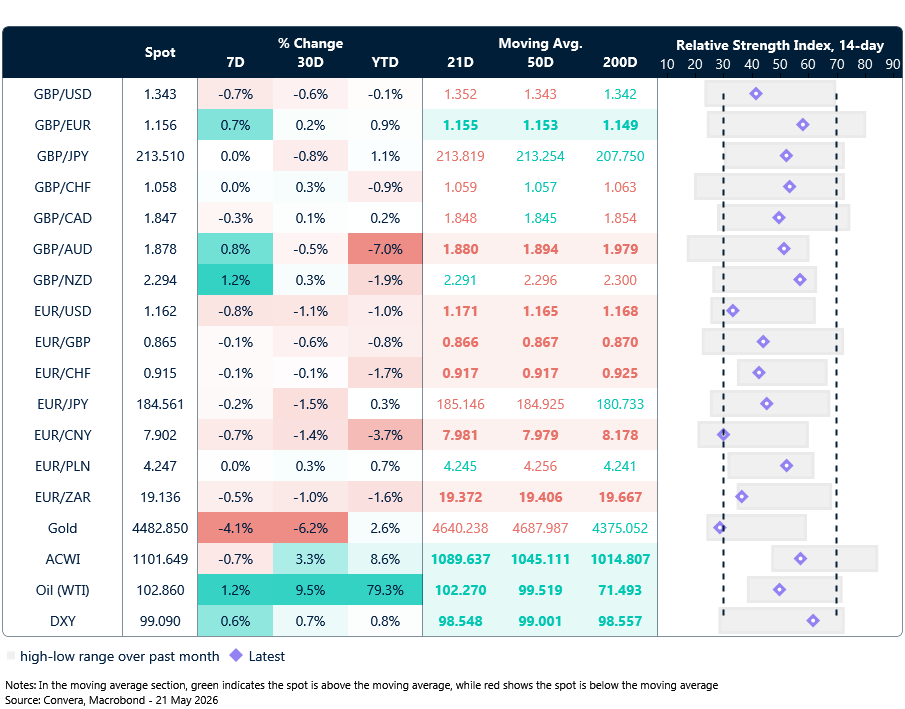

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

Calendar: May 18-22

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.