USD: Bond selloff, dollar gains

Markets are increasingly being dominated by a renewed inflation narrative, with the Iran conflict acting as the catalyst for a broader repricing across rates, risk assets and currencies. What began as an energy shock is now feeding into a more structural reassessment of inflation persistence and fiscal sustainability, driving a global bond selloff that is starting to challenge the resilience of risk sentiment.

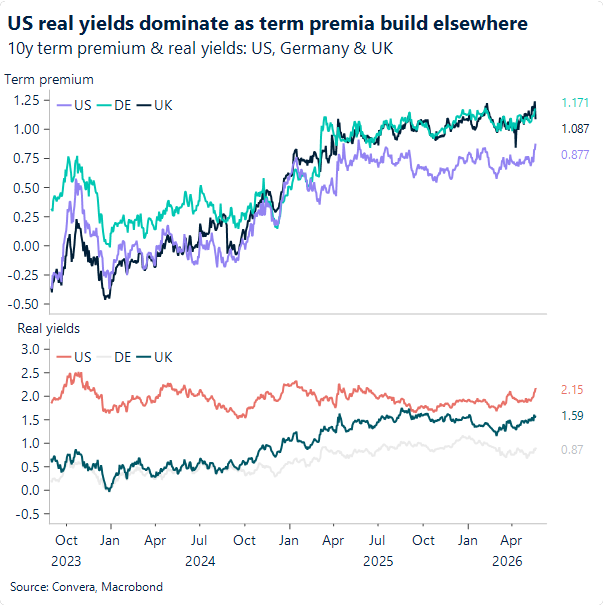

Across developed markets, bond markets are undergoing a disorderly adjustment. Long-end yields have moved sharply higher as investors demand greater compensation to hold duration amid rising deficits, sticky inflation and limited political appetite for fiscal consolidation. In the US, the Treasury curve is bear steepening, but as this remains driven by inflation concerns rather than a loss of confidence in US credit, it remains supportive for the dollar at this stage.

The shift in inflation expectations has also forced a rethink of the Fed path. Markets have moved from pricing multiple rate cuts in 2026 to now anticipating the possibility of a rate hike as early as year-end. That hawkish repricing, combined with higher energy prices, has reinforced the US rate advantage and provided a firmer underpinning for the USD.

At the same time, cracks are beginning to appear in broader risk sentiment. Equities are showing signs of fatigue, with the sharp rise in long-term yields undermining valuations. Notably, the 10-year Treasury yield now exceeds the earnings yield on the S&P 500 by the widest margin since the early 2000s – a signal that raises the risk of a more sustained equity correction. While the adjustment has been orderly so far, it raises the risk of a more sustained drawdown in risk assets if yields continue to climb.

In this environment, the dollar is emerging as a relative beneficiary. It is supported not only by higher yields and relatively stronger institutional credibility compared to peers, but also by the US economy’s continued outperformance and its relatively favourable energy position compared to other major economies. Even as oil prices have eased modestly on speculation that NATO could help secure shipping flows through Hormuz, the broader inflation impulse remains intact.

Bottom line: the market is shifting from a geopolitical shock narrative to a more persistent inflation and rates story. As that transition continues, the combination of rising yields, resilient US growth and fragile risk sentiment keeps the balance of risks tilted toward further USD strength – particularly if equity markets begin to reflect the pressure already evident in bonds.

CAD: Markets expect BoC to move by October

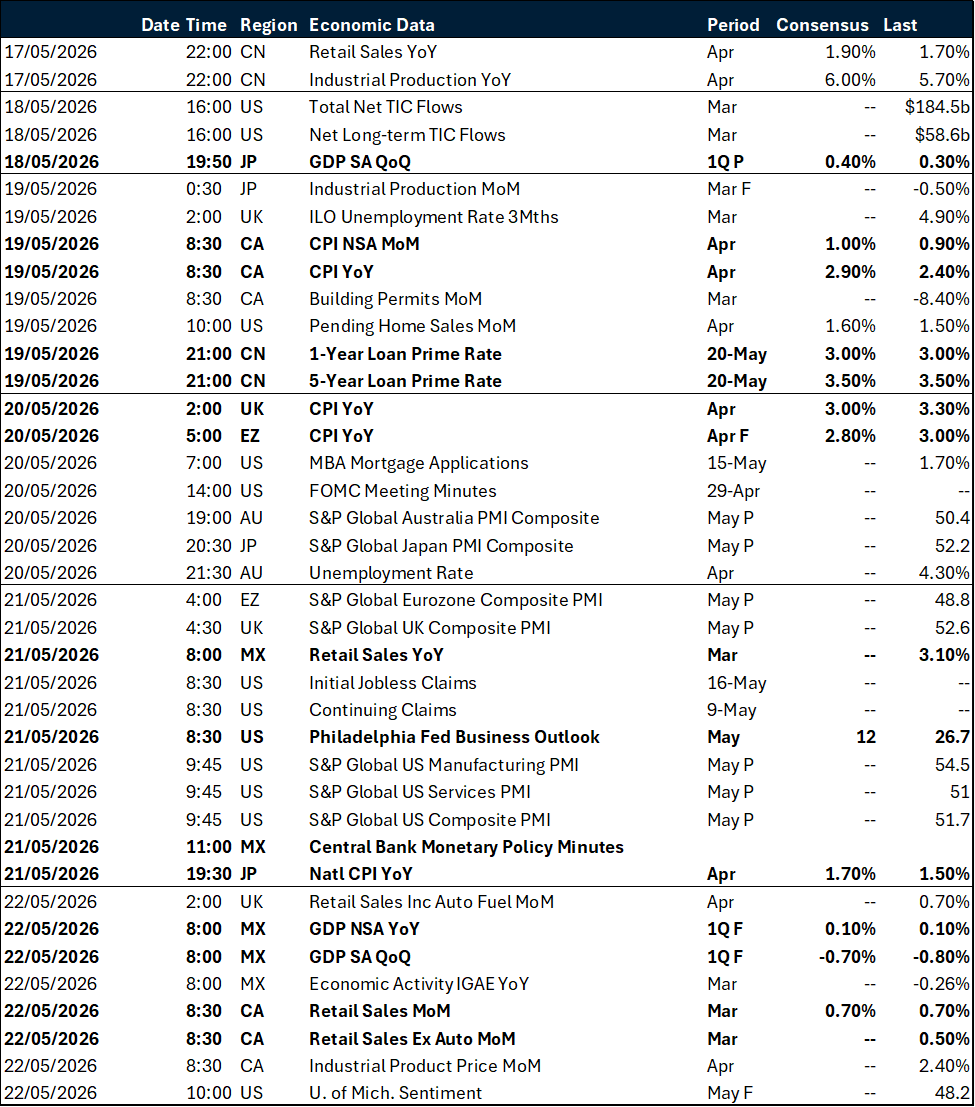

Canada’s annual headline inflation accelerated to 2.8% in April, up from 2.4% in March, driven primarily by a surge in energy costs. Gasoline prices jumped 28.6% year-over-year, largely because the April 2025 removal of the consumer carbon levy rolled out of the annual calculation window. Geopolitical tensions in the Middle East and the transition to pricier summer fuel blends further intensified these upward price pressures. However, the month-over-month seasonally adjusted gain remained contained at 0.3%, indicating that broader monthly price pressures are staying relatively stable.

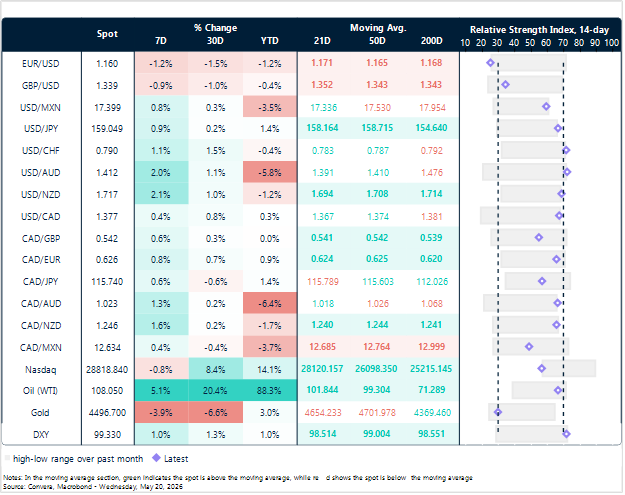

In contrast, underlying core inflation actually moderated across the rest of the economic basket. Excluding gasoline, the Consumer Price Index slowed to a 2.0% annual pace, supported by double-digit declines in travel tour costs and a cooling of rent inflation to 3.6%. While price growth accelerated regionally across nine provinces, British Columbia bucked the trend due to a notable slowdown in housing costs. That said, given how yields have reacted to the energy shock, financial markets continue to anticipate at least one interest rate cut from the Bank of Canada by its October meeting. The 2-year yield Canadian government note is trading above 3%, the highest since March this year, when the US-Iran conflict erupted.

From a technical perspective, the softer-than-expected tone helped keep the Canadian dollar on the back foot as the US dollar has stayed bid, and USD/CAD pushed above the 1.3720–1.3730 congestion zone where the 50‑ and 100‑day moving averages meet. It has been trading near 1.377 since the CPI data was released, with the next clear upside level around the 200‑day near 1.381; clearing that would look more like a re‑trend inside the familiar 1.35–1.39 range, while a stall could bring a pullback as positioning catches up.

GBP: Soft inflation meets hard constraints

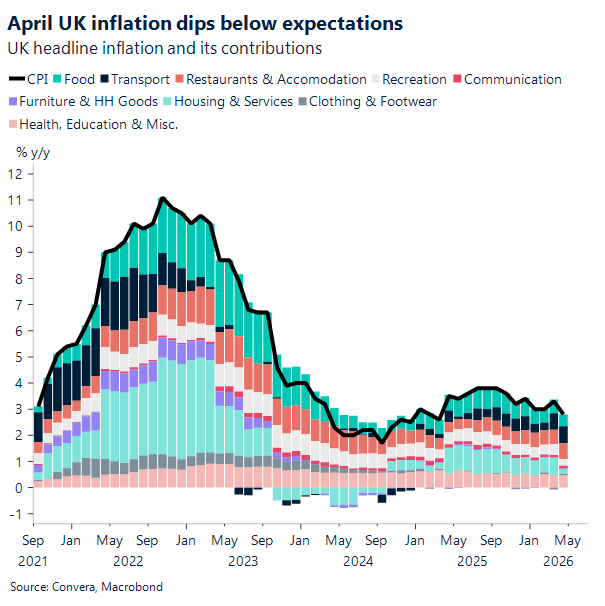

The just-released April inflation report showed headline inflation rising less than anticipated on both a month- and year-on-year basis, coming in at 0.7% and 2.8% respectively (vs. expectations of 0.9% and 3%). Core and services measures – cleaner expressions of domestic demand conditions – also rose by less than expected. Amid the ongoing conflict in the Middle East, these price measures remain particularly useful as gauges of second-round effects from energy price surges. A softer labour market acts as a cushion, containing the diffusion of energy-driven inflation spillovers. With reduced bargaining power, employees are less able to secure higher wages, limiting firms’ incentives to pass on costs through price increases.

It is also a useful reminder that, in a non-conflict scenario, today would likely have marked a return to the 2% year-on-year target for headline inflation, driven by favourable base effects as last April’s tax hikes mechanically dropped out of the annual comparison.

Sterling has so far barely budged in response to the softer outcome, adding to the muted reaction following earlier soft labour market data. We believe that the largely mechanical nature of April’s highly anticipated decline may lead markets to discount the softness of the print. Ongoing domestic political tensions, alongside conflict-driven inflation pressures feeding into continued bond market jitters, may also act as dampeners on dovish repricing.

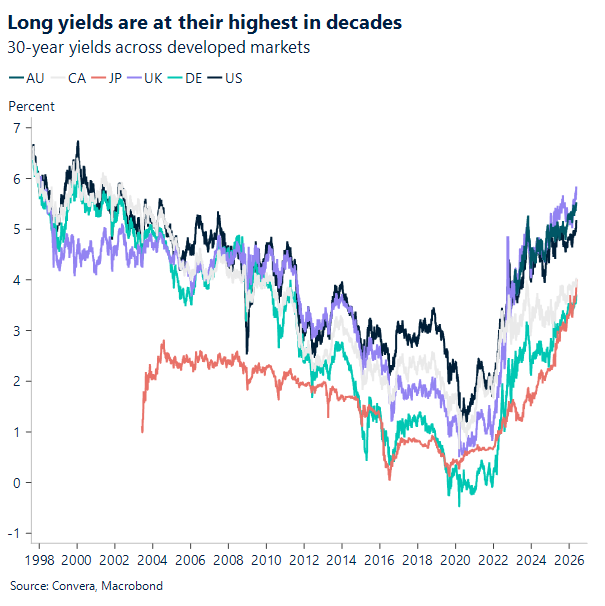

Meanwhile, sterling remains highly sensitive to bond market turmoil – beyond what domestic politics alone would justify. Long-end yields are now at multi-year highs across the G10, with 30-year Treasury yields hitting their highest level in almost two decades as conflict-driven inflation concerns, compounded by fiscal risks, continue to drive the sell-off.

The US is a particularly important case: the surge in yields is also underpinned by ongoing economic resilience, pushing real yields higher than in peer markets. In contrast, the UK and the eurozone are being forced to catch up from a much weaker macro starting point, meaning the adjustment is driven more by rising term premia than by a genuine repricing of real rates. As such, investors may require greater compensation to gain confidence in European debt.

That asymmetry is feeding directly into FX, helping to explain the recent bearish pressure on both the euro and sterling against the dollar, even in the absence of any material deterioration in broader geopolitical risk sentiment. In GBP/EUR, however, the sell-off appears to have stabilised, with the pair up 0.7% week-to-date. This suggests that geopolitics has dominated recent moves in bond markets and, as such, has not imposed a clear directional bias on GBP/EUR.

We continue to view the conflict in the Middle East and domestic political turmoil as the two defining drivers of GBP/USD and GBP/EUR, respectively. With key support levels at 1.33 in GBP/USD and 1.145 in GBP/EUR recently tested but not breached, these levels are likely to have established this week’s lows, barring any meaningful re‑escalation on either front.

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

Calendar: May 18 – 22

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.