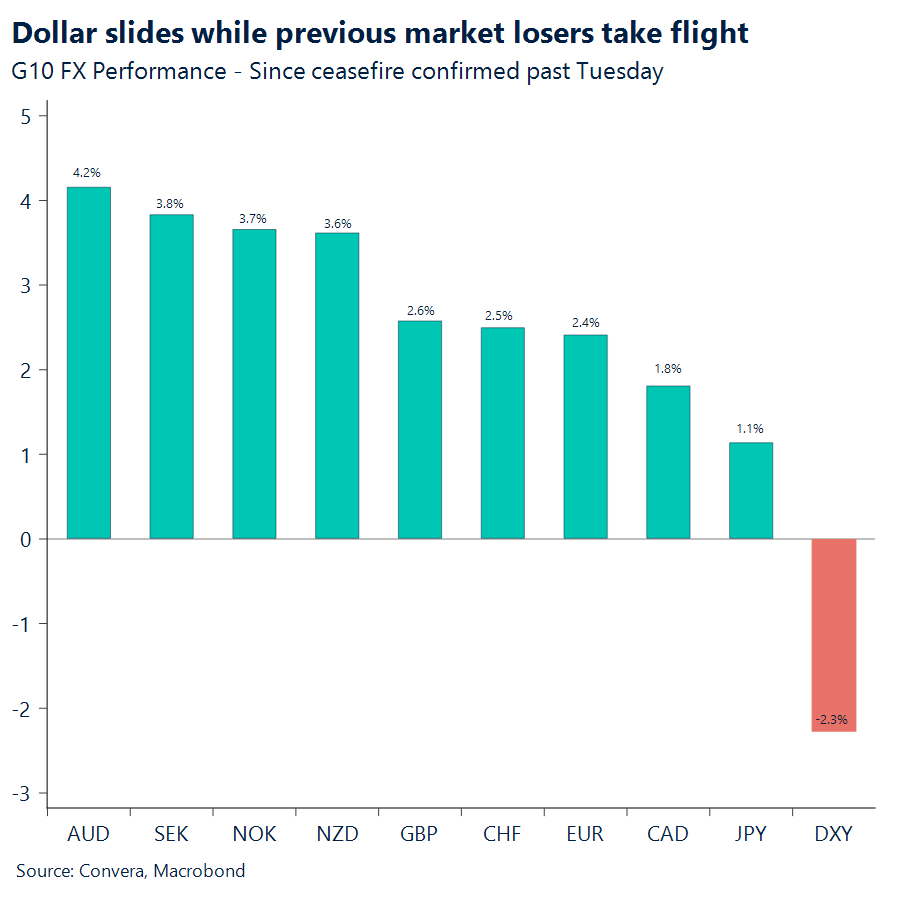

USD: Decoding the current US dollar unwind

I previously mentioned that resolving this conflict would spark a broader risk-on environment. A subsequent drop in oil prices would theoretically unwind the long-USD trade; in this mean-reversion scenario, the hardest-hit currencies were always poised to emerge as the biggest winners. Despite weekend reports that both sides violated the April 7th ceasefire, the FX market has continued to see that expected dollar unwind alongside a reversal in the G10 complex. While markets closed Friday on the understanding that the Iranian blockade had ended, highlighted by Iran confirming the reopening of the Strait of Hormuz, the situation shifted by Saturday morning. Iran has since confirmed the strait is blocked again, and diplomatic dialogue appears to have stalled once more.

Amid the volatility of these whipsawing events, markets remain hopeful that a resolution is finally in sight. The weekend’s developments are being viewed as a temporary setback rather than a derailment, as both sides appear highly motivated to find a diplomatic off-ramp. While President Trump famously favors strict deadlines, especially with April 22nd looming, he is equally pragmatic about extending them when a deal is within reach. It seems highly likely that this upcoming deadline will be pushed back. This extension should allow ongoing discussions around nuclear capabilities and other core issues to gather much-needed momentum.

As this geopolitical conflict premium fades, we must ask if the US dollar is now primarily reflecting a US risk policy premium or the combination of fears around financial stability revolving private credit, a still wobbly labor market and the post-Davos hate against the dollar. Over the last year, aggressive trade stances, tariff threats, and deficit spending under the current administration have baked a distinct uncertainty premium into the greenback. Investors have demanded a premium to offset the unpredictability of these America-first economic policies and the broader risks of deglobalization.

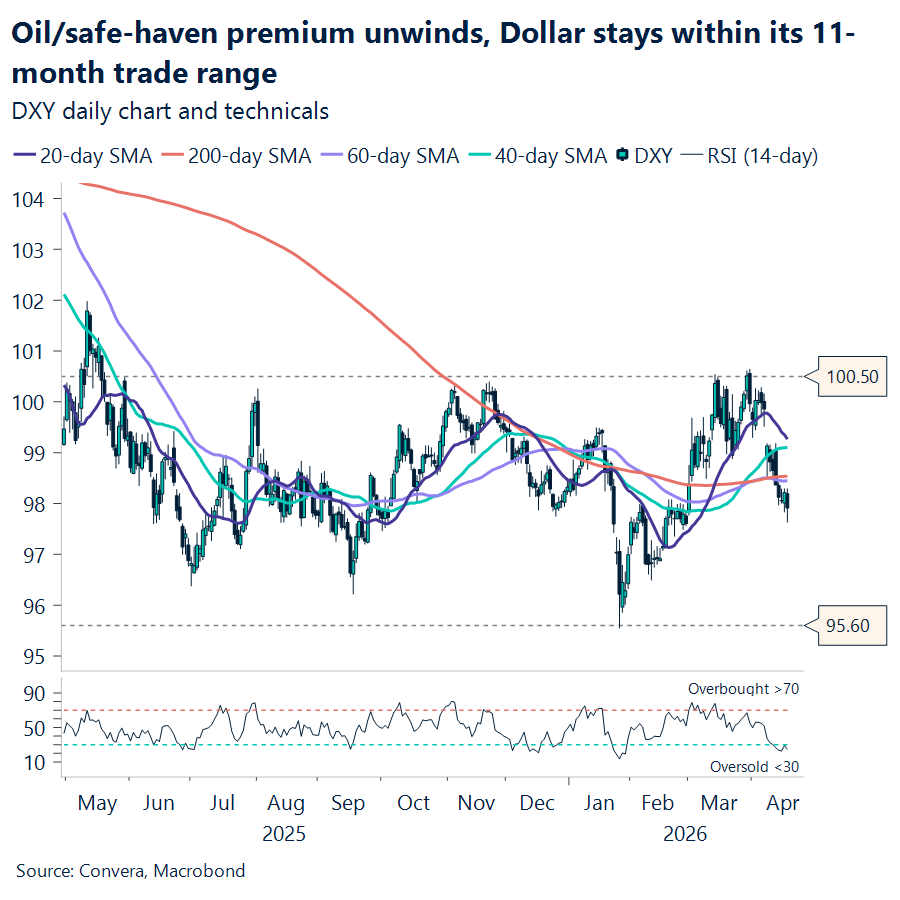

However, the math is telling that the dollar is following a high beta to oil on the downside. Recall I’ve mentioned the rule of thumb suggests that for every 10% drop/increase in oil, the dollar usually falls/surges by roughly half to one percent. With WTI crude tumbling 26% from its $113 close on April 7th to $83 end of last week, the DXY index has similarly dropped 2.5% from its 100.6 peak to 97.9. This means the dollar is currently tracking almost perfectly with historical oil-beta models on the downside, interestingly remaining trapped within its broader eleven-month trading range.

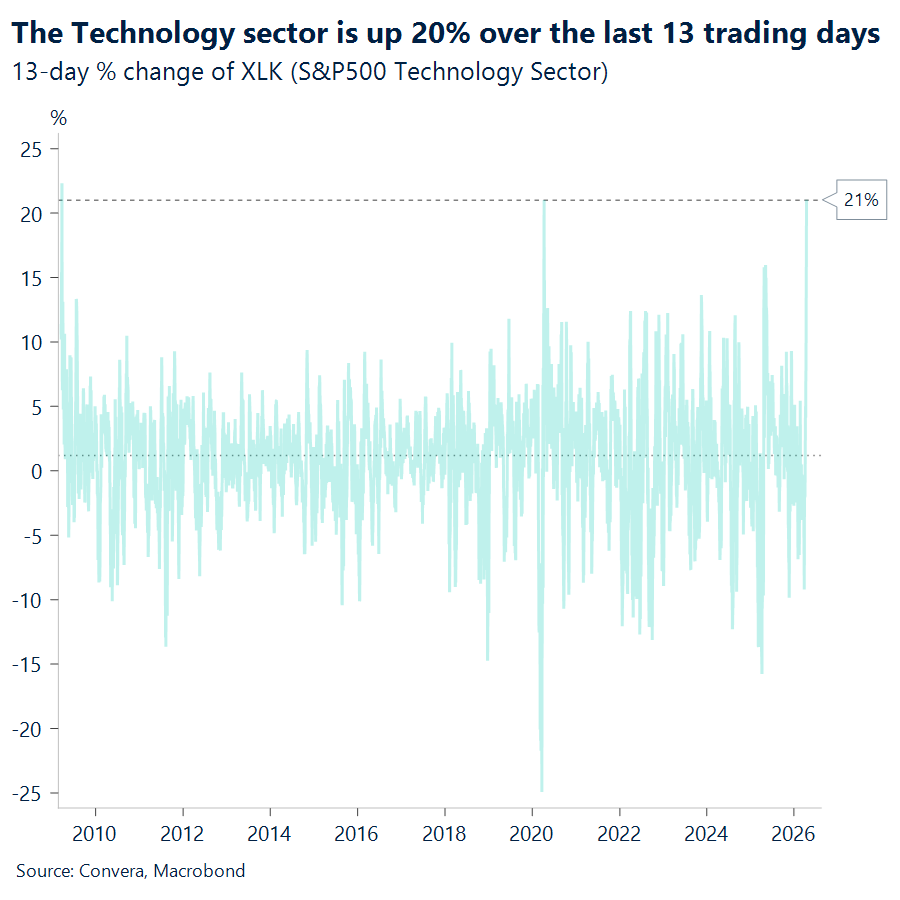

While the currency market shows the dollar sliding, elsewhere, however, financial markets ended last week absolutely partying as risk-on sentiment aggressively recovers. A perfect proxy for this mood is the US technology sector, which has surged an astonishing 20% over the last thirteen trading days. To put that massive rally into perspective, the last two times we saw comparable tech surges were during the historic recoveries from Covid in April 2020 and the Financial Crisis in March 2009.

Moving forward, the combination of a calmer global landscape and a renewed emphasis on domestic policy, the path of least resistance for the dollar remains lower in the near term. As market attention moves back and forth between overseas conflicts and back toward interest rates, it is crucial to revisit the broader macro stage. Two-year Treasury yields look ready to slip below the effective fed funds rate very soon. This shift proves the market has completely stopped pricing in an inflationary oil shock and is returning to expectations of a shallow Federal Reserve cutting cycle. Net, the dollar index will likely remain confined within its established 11-month trading range for the foreseeable future, as mentioned in our Global FX Outlook report for the month of April.

A total breakdown in negotiations and a prolonged closure of the strait would return us to the pre-April 7th environment. In this scenario, the dollar would be pulled higher by the twin forces of surging oil prices and elevated market stress. For now, it’s likely that we start week 8 of this conflict with the known defensive pattern of a stronger Dollar and higher oil.

For now, we enter Week 8 of the conflict likely partially reverting the gains from last week, in the familiar defensive pattern of a stronger dollar and elevated oil prices.

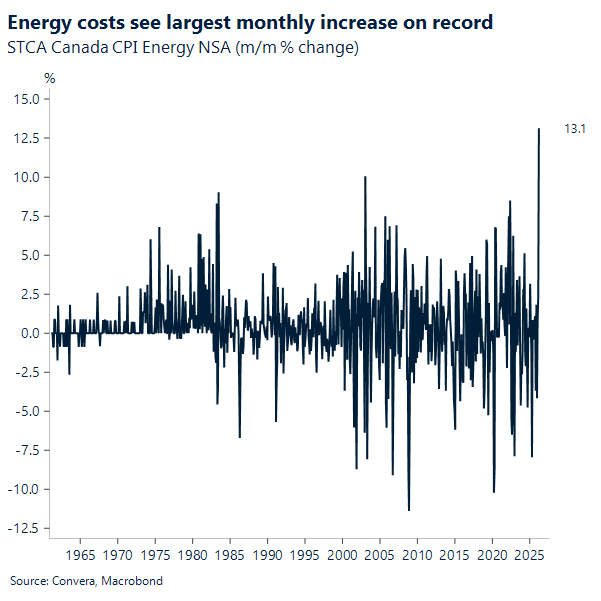

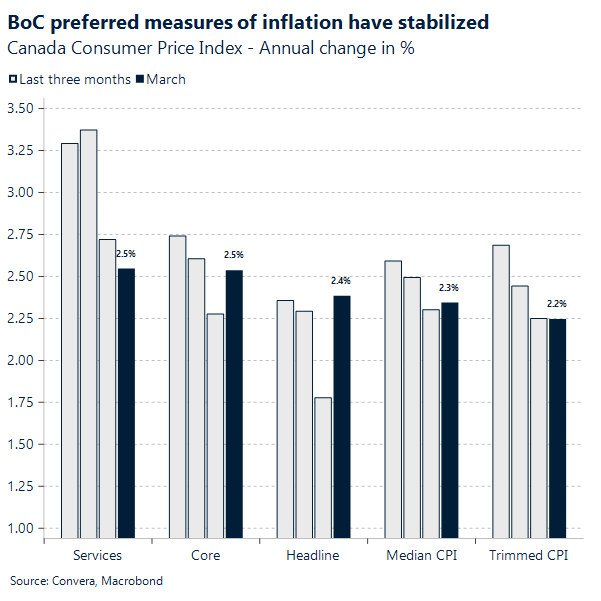

CAD: Energy costs drive March inflation higher

Canada’s inflation rate saw a big jump in March, landing at 2.4% year over year. This marks a clear acceleration from the 1.8% increase recorded in February. The primary driver behind this hotter headline number is a massive surge in energy costs. Specifically, gasoline prices spiked due to supply shocks tied to recent conflicts in the Middle East, recording their largest monthly increase on record. If we strip away those volatile fuel costs, the underlying inflation picture actually cooled slightly to a 2.2% annual pace (CPI Core- Trim YoY).

Beyond the gas pump, shoppers are still feeling a slight pinch in the grocery aisles. Fresh vegetable prices climbed 7.8% annually because of tighter global supplies and poor growing conditions. However, overall downward pressure from base-year effects helped keep the broader inflation numbers in check. The final lingering impacts from last year’s temporary GST/HST break have officially cycled out of the 12-month calculation, providing some statistical relief. Consequently, underlying price pressures remain relatively stable, with the Bank of Canada’s preferred core trim and median measures settling around 2.2% and 2.3% respectively.

Despite the noticeable jump in headline inflation, the immediate market reaction has been muted. After five consecutive sessions trading lower, it is now finding support in the 1.365 to 1.370 range. This week, the currency’s trajectory depends heavily on global risk sentiment and geopolitical developments. If diplomatic efforts succeed and the broader US Dollar softens, the loonie is well-positioned to continue testing the 1.365 level. Otherwise, a cautious pause around 1.37 seems highly plausible as traders await, with eyes turning to the retail sales data coming later this week.

EUR: Whiplash headlines, limited follow-through

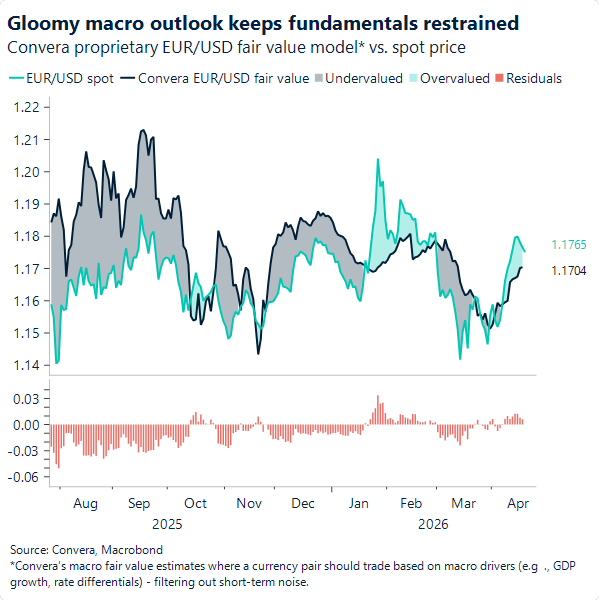

The latest twists around the Strait of Hormuz over the weekend reinforce a familiar message for market participants: it is still too early to commit convincingly to the peace trade. Oil prices jumped again on renewed uncertainty, yet FX reactions were notably restrained. As expected, EUR/USD opened the week on a softer footing, but the pullback has been orderly, with the pair holding comfortably above 1.17 for now.

More broadly, EUR/USD has unwound much of March’s war‑driven weakness, trading just below 1.18 – roughly where it sat in late February, before hostilities escalated. The pair remains above all key daily and weekly moving averages and is up around 1.7% month‑to‑date, underscoring that momentum had turned positive. However, recent price action also highlights a growing lack of conviction. In the absence of a credible and durable peace framework, markets have been reluctant to push the euro meaningfully higher.

Fundamentals argue for caution too. Our short‑term fair‑value model points to levels in the low‑1.17s, suggesting that rallies toward the 1.18–1.19 region are increasingly stretched. Elevated energy prices continue to pose a risk to the euro‑area growth and inflation mix, and although ECB rate hike expectations should offer some yield-driven support, the euro appears to lack the macro backing required for a sustained break toward the January highs near 1.20 any time soon.

The broader pattern remains one of whiplash without follow‑through. The Middle East conflict continues to generate sharp moves in commodities and headlines, but FX is increasingly trading in ranges as investors wait for clarity. Until uncertainty around escalation versus de‑escalation is resolved, EUR/USD is likely to remain resilient, but capped — supported by fading USD strength, yet constrained by limited conviction on the euro side.

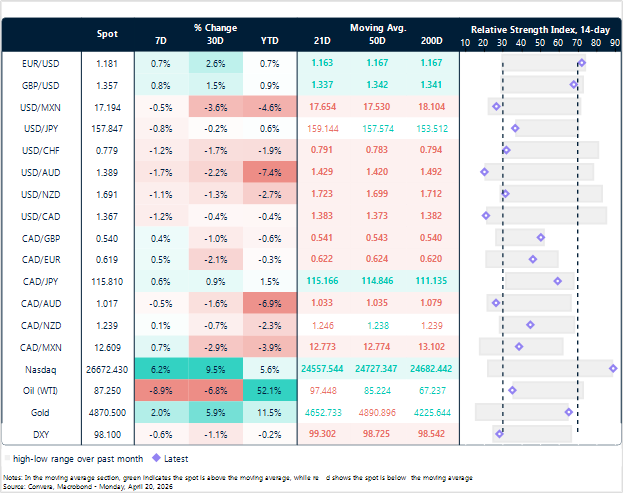

Market snapshot

Table: Currency trends, trading ranges & technical indicators

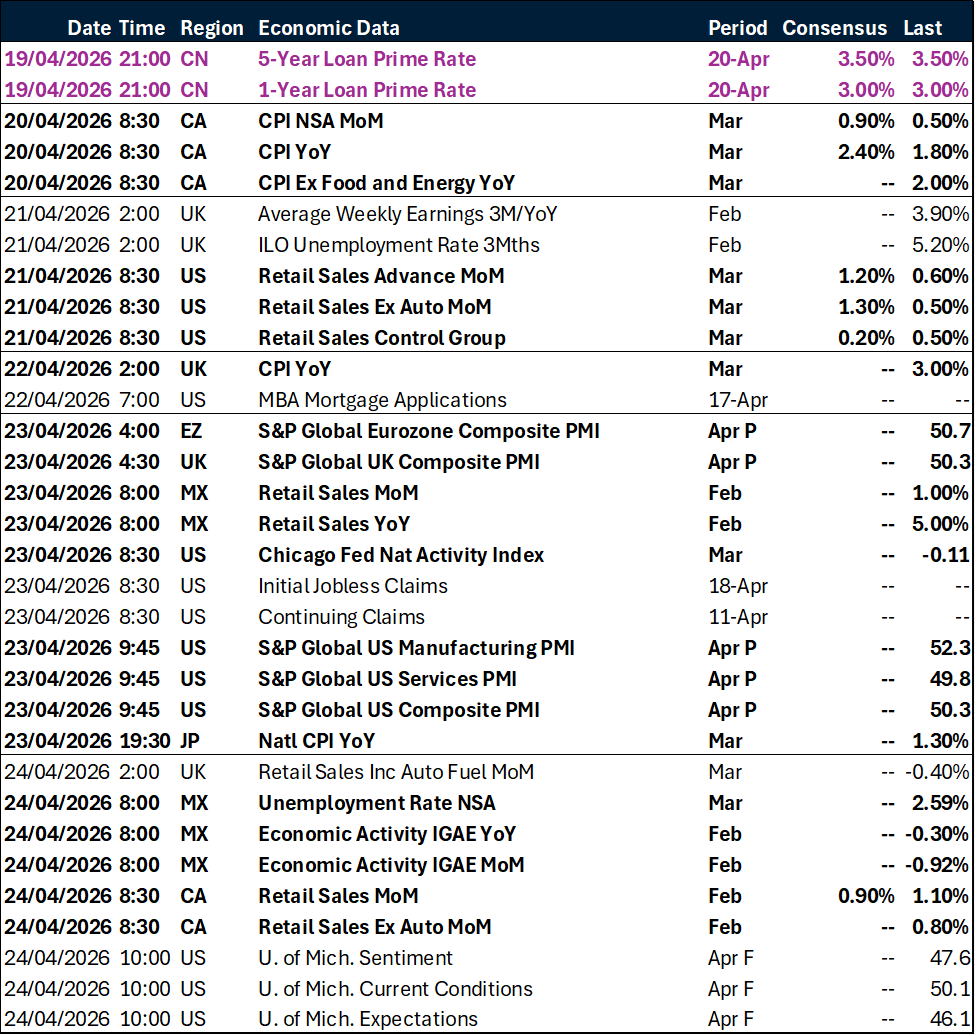

What’s happening in markets this week?

Geopolitical tensions continue to dominate markets, with investors closely watching for any sign of de-escalation in the US–Iran–Israel dynamic. The longer these frictions persist, the slimmer the chances of a meaningful economic rebound. Attention now turns to Washington, where the Senate Banking Committee will review Kevin Warsh’s nomination on Tuesday. The hearing is expected to be especially contentious, given Warsh’s roughly $100 million in unspecified holdings and Senator Tillis’s current hold on the floor vote. Complicating matters further, President Trump has been openly frustrated by the possibility of Jerome Powell remaining Acting Chair beyond May 15. As a result, the legal debate over the President’s authority to remove Federal Reserve officials has emerged as a renewed tail risk to market stability.

Beyond this, a packed calendar of economic data and corporate earnings will test the durability of the market’s prevailing “defensive” positioning after the weekend events. Highlights include Canada’s CPI on Monday; US retail sales and Germany’s ZEW survey on Tuesday; and UK CPI and wage data on Wednesday. Earnings season also shifts into a higher gear, with reports from Tesla and Microsoft on Wednesday, alongside Boeing, Intel, and Procter & Gamble. The week concludes with a global temperature check via flash PMIs for Japan, the Eurozone, and the US on Thursday, followed by Japan’s CPI and retail sales in Canada both on Friday.

Key global risk events

Calendar: April 20-24

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.