USD: Greenback’s year‑end balancing act

As we enter December, two things stand out to watch: how hawkish the tone will be at the Fed’s upcoming meeting, and whether year‑end seasonality will prove as bearish a force for the dollar as it typically does.

On the first point, it is typically the messaging in forward guidance after the policy rate decision that drives FX, as by the time the meeting arrives the cut or no‑cut (or hike) decision is usually priced in. This year, caution has prevailed, and even the two cuts delivered at the past two meetings came with hawkish‑leaning language that ultimately supported the greenback. For December, with easing expectations nearly 90% priced in and the picture still muddled by mixed (not cohesively soft) data – or in some cases a lack of data altogether (shutdown) – we could see yet another dollar‑positive event.

Meanwhile, Trump appears to have settled on his choice for the next Fed chair, with markets debating how credibly dovish that candidate might be. While this remains more of a 2026 story, the mere prospect of a dovish tilt is enough to cap further dollar upside in the absence of stronger bullish catalysts.

On the second point, seasonality is typically dollar‑negative in December. Portfolio rebalancing often drives flows out of typically outperforming US assets, weighing on the currency. But this year may be different. US assets have faced headwinds from tariffs and the recent equity selloff, while significant hedging of previously unhedged portfolios has already taken place earlier in the year during bouts of sharp dollar weakness. That could mute the usual seasonal drag.

Taken together, these dynamics suggest December could be supportive for the dollar if the Fed cuts with a cautious tone and rebalancing flows prove less forceful than usual. Still, risks remain: if the Fed holds instead of cutting on the “we need more data” premise, post-meeting releases – NFP, CPI, and Q3 GDP – will take on outsized importance, and any dovish signals from those could weigh on the dollar more severely.

For now, technicals continue to dominate. Price action is carving out higher highs and higher lows, with 99.400 established as most recent support. With most easing already priced in for December, fresh US macro data will be needed to challenge what remains a fragile but persistent ascent. For this week, keep an eye out on ISM, ADP and PCE figures.

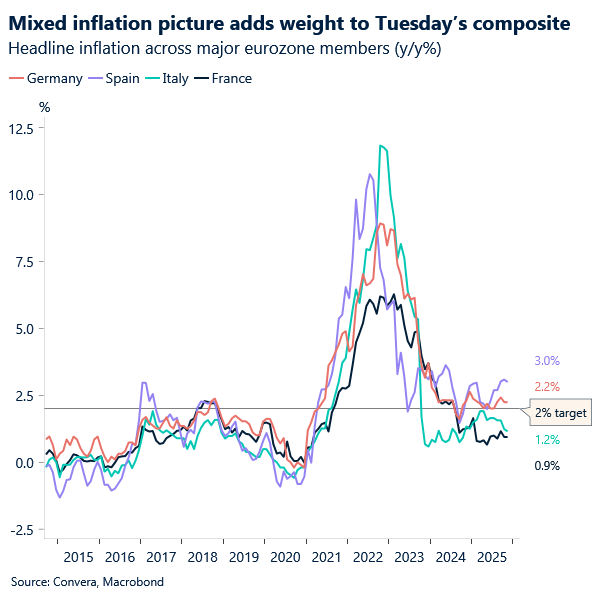

EUR: Euro mixed CPI, eyes on Moscow

Friday closed the week with mixed CPI readings across the eurozone’s four largest economies: price pressures were weaker than expected in France and Italy, but stronger in Spain and Germany. Notably, Germany’s inflation rose to its highest level in nine months at 2.6% in November, up from 2.3% in October. This week’s bloc‑wide reading for the 20‑nation eurozone – due Tuesday – is now highly anticipated to provide more cohesive context to the mixed picture, though it is still expected to remain close to 2%.

Overall, the backdrop continues to lean toward keeping rates steady for now, muting immediate impact on the euro. Instead, geopolitical developments may carry more weight in the nearer term. US and Ukrainian negotiators appear to have held productive discussions after meeting in Florida over the weekend, with US special envoy Steve Witkoff expected in Russia this week to continue talks with the Russian counterpart. The visit could positively influence the common currency if markets perceive meaningful progress, following Putin’s openness last week toward a redrafted peace proposal.

For the week ahead, we expect EUR/USD to remain range‑bound, with firm support at 1.15. Resistance is seen at 1.1620/1.1630, with scope to break above it should substantial progress emerge on the geopolitical front. Realistically, however, we see a meaningful US data miss as the more likely trigger for such a breach.

GBP: Relief rally fades, risks resurface

Renewed risk aversion is weighing on the pound this morning, leaving it on the back foot against most majors. We also highlighted last week that sterling’s post Budget climb looked more like a relief rally than a lasting trend, especially given the scope for a more dovish Bank of England (BoE) policy trajectory. Short-term risks are skewed to the downside in our view, but note that seasonal trends are positive.

Markets welcomed Chancellor Reeves’ signal of fiscal restraint, reflected in the favourable gilt and FX reaction as fiscal risk premia unwound. Yet the political backdrop remains unstable, with calls for Reeves to step down amid accusations of misleading the public on the state of the UK’s finances.

Meanwhile, traders lean toward a December BoE cut and have pulled forward expectations for another move to May, eroding sterling’s yield advantage. GBP/USD momentum stalled at its 200-day EMA near $1.3270 last week, reinforcing that near term strength is tactical, not structural.

From a broader lens, sterling’s H2 struggles underscore the UK’s weak economic backdrop and fiscal fragilities. GBP/EUR’s near‑6% slide highlights how domestic headwinds have weighed more heavily on the pound than the euro. Indeed, the euro’s resilience has broken the usual lockstep between EUR/USD and GBP/USD, with correlation at its lowest in roughly four years — a sign sterling’s vulnerability is increasingly home‑grown.

Still, sterling avoided a seventh straight monthly decline versus the euro, hinting the downtrend may be stalling. Moreover, GBP/USD usually climbs in the month of December, but this is contingent on a broad-based equity rally.

There’s no notable UK data is due this week, but BoE speakers are in focus: Dinghra (arch‑dove) and Mann (arch‑hawk) could sway rate expectations and sterling pricing.

Sterling crosses are starting to look oversold

Table: Currency trends, trading ranges and technical indicators

Key global risk events

Calendar: December 1-5

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.