USD: Trading the headlines

Markets continue parsing conflict headlines, with attention fixed on the Strait of Hormuz and its restricted passage since the conflict began. Reports of a trickle of vessels getting through, the release of emergency oil stockpiles, and rising flows from Saudi Arabia’s Yanbu port as a Hormuz bypass have helped calm oil prices, which fell 5% yesterday. The US dollar index – the DXY – also trimmed recent advances, slipping 0.7% – its first daily drop after three consecutive days of gains – while both stocks and bonds rebounded. The moves carry elements of both technical washouts after several weeks of directional trading and genuine market indecision: with long‑term growth and inflation expectations still anchored, headline‑driven swings between risk‑on and risk‑off are amplified, feeding into increasingly erratic price action.

That said, the conflict in the region continues to show no signs of concrete de-escalation, with Iran striking new targets across the Persian Gulf, including a key UAE oil hub yesterday. Meanwhile, Donald Trump is increasing pressure on allies to help the US reopen the strait by sending warships to escort commercial vessels – an implicit signal that he has no intention of ending the conflict for now. So far, US partners have resisted, seeking to avoid deeper involvement and further escalation.

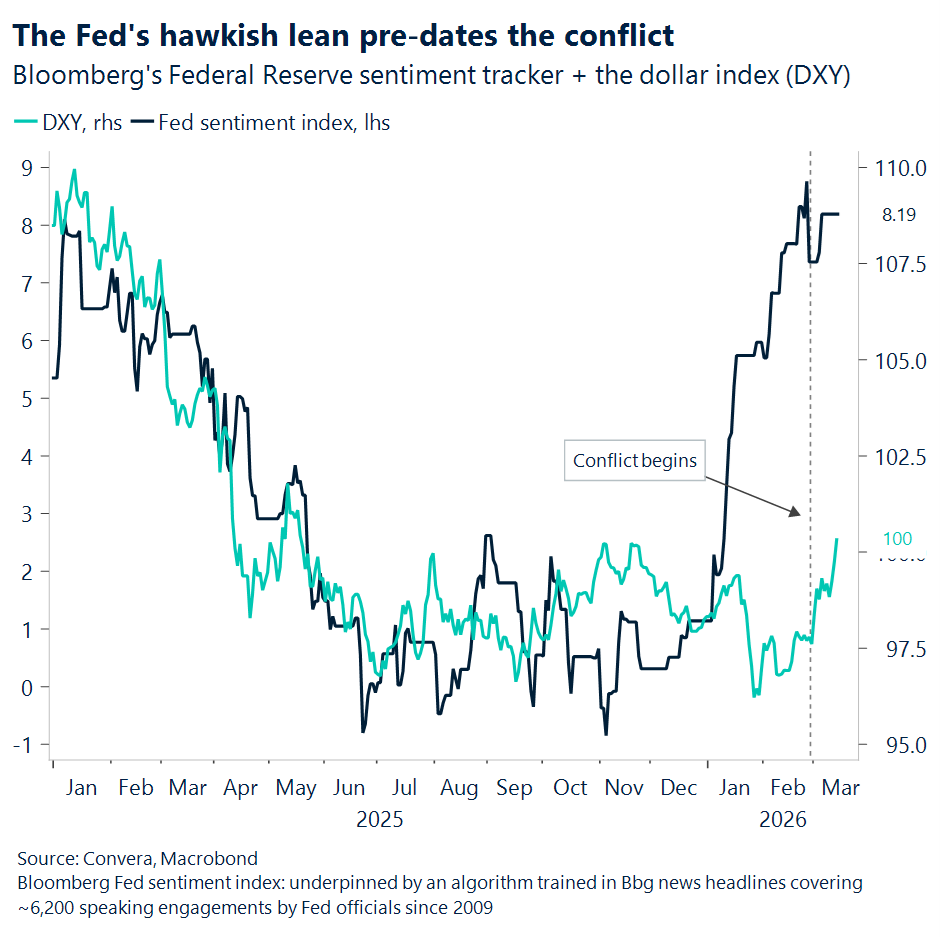

The dollar index hovers just under the 100 mark, with a push back above likely this week on continued conflict risk, supported by a more hawkish Fed tone. At the Fed policy meeting on Wednesday, we expect hints of a more prolonged pause before further easing later in the year. Recent FOMC messaging has shown heightened vigilance over inflation risks, while the labour market appears to be stabilising. Recent soft prints (see February’s jobs report) may have been distorted by adverse weather conditions, leaving the Fed focused squarely on upside inflation risks, now also exacerbated by the conflict.

EUR: Oil still calls the shots for EUR/USD

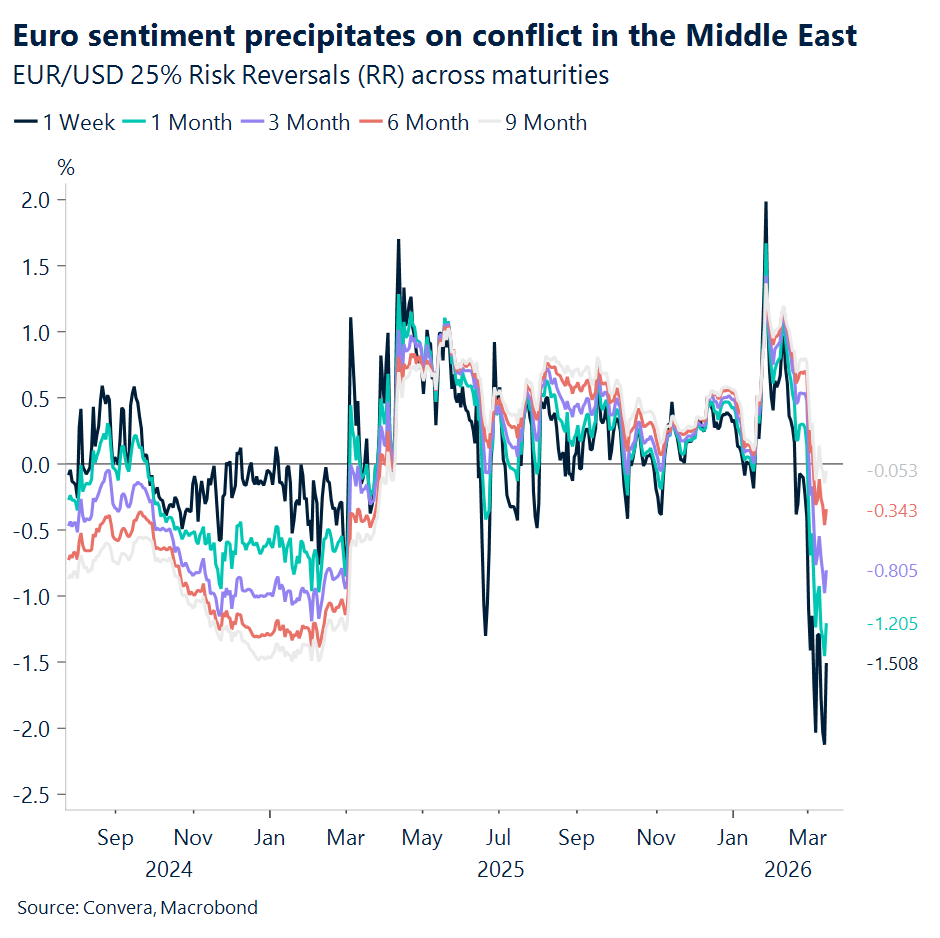

EUR/USD pared some losses yesterday on fragile market optimism after touching lows last seen in August 2025 near the 1.14 mark. A test of this level still looks likely this week, driven by another leg higher in oil and a more forceful bearish FX pass‑through from hawkish Fed signals than from a hawkish ECB. The rates‑driven FX pressure appears justified: an easing bias at the Fed means any hawkish recalibration tends to have deeper FX implications than the ECB’s stance, where roughly 40 bps of hikes are already priced in by year‑end – especially with both central banks expected to remain non‑committal at this stage.

That said, the dominant force on EUR/USD remains oil prices for now, with the influence of rate differentials on FX price action having diminished significantly since the conflict began. There is a mechanical push lower on EUR/USD due to heightened demand for dollars given their dominance in oil markets, but also a sentiment‑driven layer that weighs on the euro as hopes for a 2026 eurozone rebound – partly tied to Germany’s spending commitments – fade. The backdrop suggests that even if oil‑linked bearish pressure on EUR/USD eases as marginal USD demand dissipates, a more sluggish eurozone growth outlook as a result of a prolonged conflict would still dampen euro sentiment, limiting the scope for any meaningful domestically-driven rebound in the pair.

GBP: Options skew flag downside risk

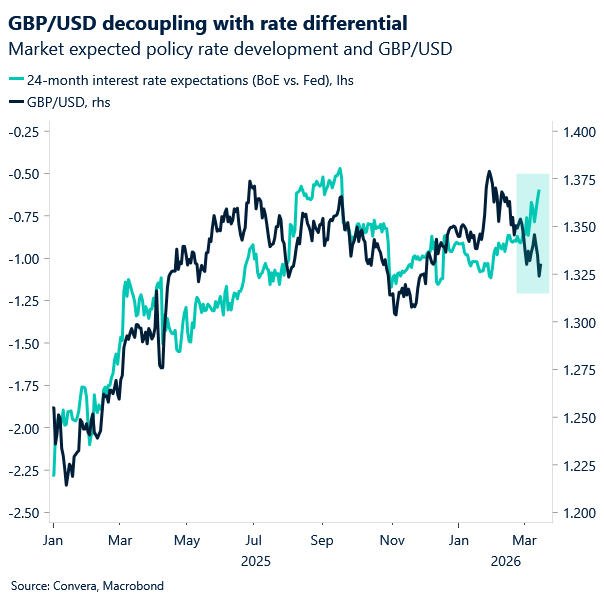

Sterling is still outperforming many European peers as markets rapidly reprice the Bank of England (BoE) cycle. What looked like 50bp of cuts priced for the year has flipped into roughly 17bp of hikes, with traders treating the BoE as one of the most responsive central banks to renewed inflationary pressure. This has helped GBP/EUR climb towards €1.16 – up over 1.4% this month. But rate differentials aren’t doing all the heavy lifting — the pound’s underperformance against commodity‑linked FX makes clear that terms‑of‑trade dynamics, not policy alone, are steering the broader GBP narrative.

The hawkish turn reflects genuine concern among some policymakers that inflation was never fully contained, yet the macro backdrop tempers that narrative. A looser labour market and tighter fiscal stance than in 2022 both reduce the risk of persistent second‑round inflation, limiting how far the BoE can lean into its hawkish instincts.

That helps explain why sterling’s resilience is selective. GBP/USD is down roughly 1.4% month‑to‑date, unable to break its run of lower highs and now back below $1.33. If the energy shock proves short‑lived, support should emerge in the low 1.30s. But a prolonged conflict and sustained pressure on energy prices would revive the vulnerabilities that defined the 2022 sell‑off.

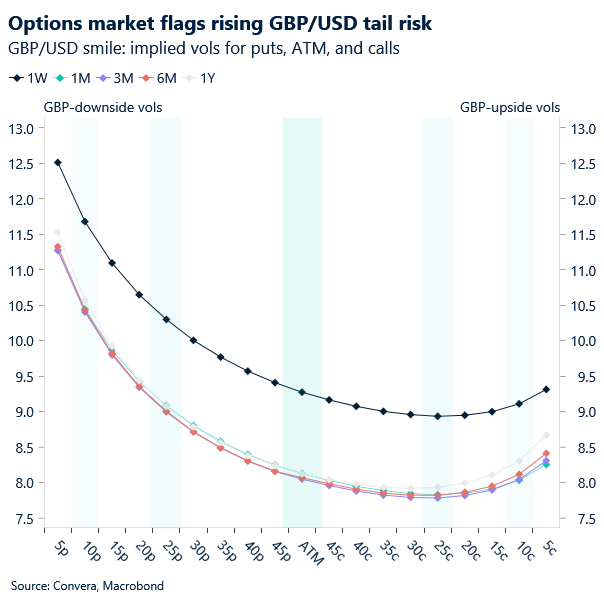

The options market is telling the same story. The GBP/USD smile has developed a pronounced left‑leaning tail, with a steep downside slope that signals traders are paying up for protection against sharp sterling weakness. The weekly tenor is even more skewed, reflecting concern about near‑term gap risk and headline‑driven volatility. In short, the market sees asymmetric risks tilted firmly to the downside, consistent with the broader terms‑of‑trade shock weighing on the pound.

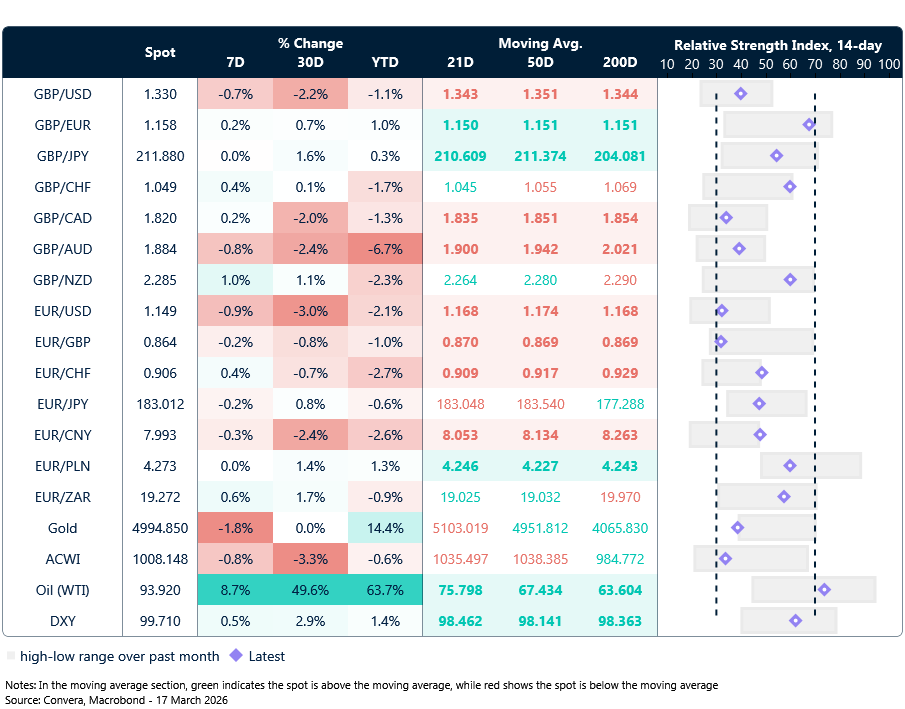

Market snapshot

Table: Currency trends, trading ranges & technical indicators

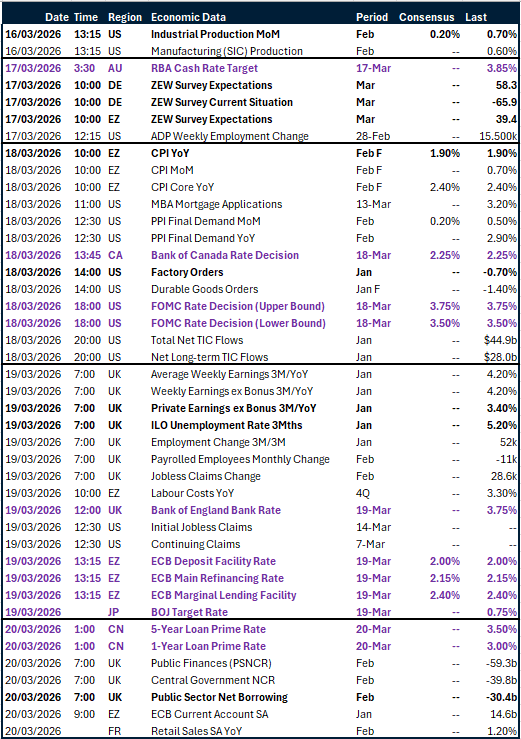

Key global risk events

Calendar: March 16-20

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.