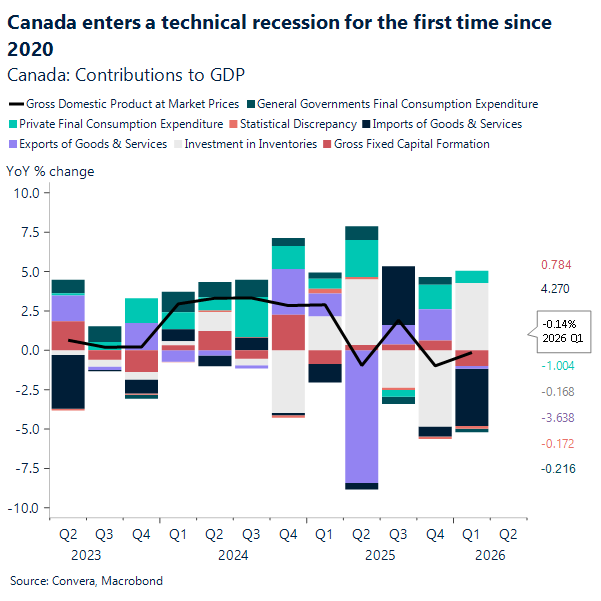

CAD: Canada enters technical recession following weak quarter

The Canadian economy has officially slipped into a technical recession. Real gross domestic product fell by 0.1% on an annualized basis during the first quarter, following a revised 1% contraction late last year. This surprise decline completely missed the 1.5% annualized increase anticipated by both the Bank of Canada and forecasters. We have not seen two consecutive quarters of negative growth since the 2020 pandemic, and before that, the 2015 oil crash. Alongside a looser job market, this data paints a noticeably softer picture of the economy as ongoing US trade tensions, lack of productivity impulse and softening domestic demand continue to squeeze domestic businesses.

Weak spending across the board heavily drove this recent economic contraction. Business capital investment posted its fifth consecutive decline, shrinking 3% on an annualized basis due to lower spending on engineering structures. Government capital investment also shrank by an annualized 9.6% after a previous surge in military spending. Interestingly, while weapons outlays dropped, the C$8.3 billion spent still remains well above historical averages. Meanwhile, the household saving rate dropped to a two-year low of 3.5% as consumers faced a tough financial environment with reduced investment earnings and higher interest payments.

Final domestic demand edged down by 0.1% during the first quarter of the year. This subtle dip reflects a complex tug-of-war happening within the broader economy. On one side, we saw noticeable drops in both business and government capital investments heavily pulling the figures down. On the other side, resilient household spending tried to counterbalance those investment declines. Ultimately, that consumer effort fell just short of keeping overall domestic demand in positive territory. Everyday consumers actually stepped up their spending, pushing household consumption up by 0.4% during the first quarter. Shoppers focused their wallets heavily on everyday necessities, leading to higher expenditures on food and financial services. However, this growth was visibly tempered by a clear pullback in big-ticket purchases and discretionary travel. Fewer Canadians opted to travel abroad, and there was a noticeable decrease in the purchase of new vehicles.

This cautious approach makes perfect sense when you look at the mounting financial pressures facing average households. While disposable income managed a modest 0.6% increase, nominal consumption expenses rose at a faster 0.9% pace. This growing imbalance effectively forced the household saving rate down to a two-year low of 3.5%. Consumers are simply stretching their dollars further to cover rising costs, especially since the household consumption deflator climbed 0.6% due to sticky food and energy prices.

As a direct result of this sluggish domestic data, the Canadian Dollar has noticeably weakened, with the USD/CAD trading back above 1.38 following yesterday’s reversal on softer than expected US data. Furthermore, implied probabilities now show the market expects only one rate hike by December of this year. This revised outlook stands in sharp contrast with prior forecasts, as before this weak GDP print, markets anticipated a rate hike around the upcoming October meeting.

USD: DXY stays range bound

The USD DXY Index still looks restrained from a technical perspective, and the bigger picture remains one of a market trying to stabilise. The USD DXY Index is trading near 99.03. That leaves the index below the 20 month moving average at 100.94 and well below the 50 month moving average at 103.05. Price is also sitting just under the 100 month moving average at 99.70, which adds another layer of resistance close to spot. By contrast, the 200 month moving average at 92.66 remains far below the market and continues to define the long run floor. After the sharp slide from the late 2024 highs near 109, the monthly candles increasingly point to consolidation, with repeated failures to build momentum above the 100 level.

That technical picture fits a macro backdrop that is turning less supportive for the dollar. The latest US data carry a clear message. First quarter GDP was revised lower again, real incomes are fading, and inflation is still elevated enough to erode purchasing power. Even with equities at record highs, the wealth effect looks too narrow to carry the broader consumer. Higher income households can still spend, helped by asset gains, but the middle and lower parts of the income distribution are under more visible strain. Gasoline prices and broader living costs are absorbing a larger share of income, and that pressure is now showing up in the hard data. Tax refund support appears to have run its course, while inflation near 4% continues to squeeze real demand. In that setting, the dollar loses one of its cleaner bullish foundations, since the US economy does not look decisively stronger than the rest of the pack.

The household side of the story is especially important for the second half of the year. Personal income was flat in April, yet personal spending still rose 0.5%. That gap suggests consumers may be leaning on savings to keep activity going. At the same time, real incomes have fallen in five of the past seven months, and the saving rate has moved lower as households draw down reserves. A sharp decline in auto spending adds to the sense that consumers are becoming more selective and more defensive. That is not the profile of an economy gaining speed. It is the profile of one that is trying to hold up under pressure. Inflation has eased only modestly, with monthly core prices softer but the annual core rate still sticky at 3.3%. Durable goods were firmer on the surface, yet core capital goods orders fell, which hints at caution from firms as well. The combined signal is messy, but not dollar bullish in a clean way.

From a technical standpoint, DXY needs a monthly close back above 99.70 and then above 100.94 to improve the tone. A stronger move through that resistance band would shift attention toward 103.05, which is the larger barrier on the chart. Until that happens, the market still looks trapped in a broad corrective phase. Recent candles suggest buyers are willing to defend the high 97s and low 98s, but they have not shown enough strength to reclaim the moving averages overhead. As long as that pattern holds, rallies are likely to look more like recoveries inside a range that’s held up for a year now.

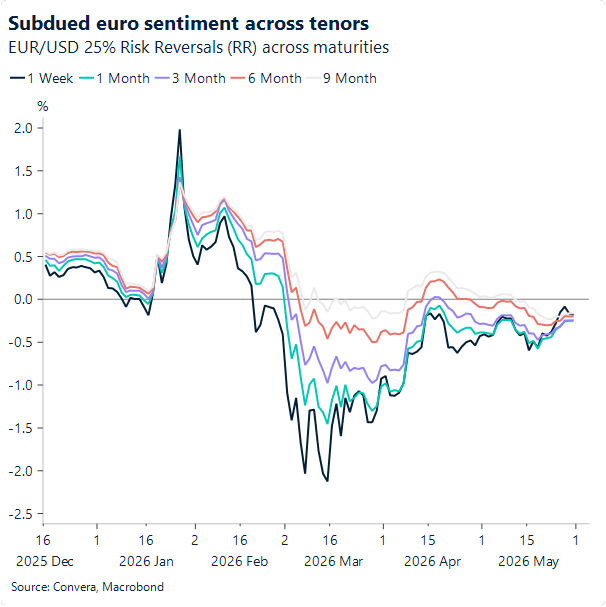

EUR: Euro sentiment turns subdued

Options markets point to euro sentiment becoming more uniformly subdued across different time horizons. Risk reversals across tenors – which reflect relative hedging demand for EUR versus USD strength – show a preference for the latter. The more compressed range, as the chart below indicates, suggests an increasingly unanimous view and may point to less exciting price action ahead, under the base case that the impasse over Hormuz drags on.

There is also a rates story that lacks much excitement from the euro side. Markets are pricing in almost a full 25bp hike for June, but the extent to which forward guidance remains hawkish is likely to be quite limited, given the highly uncertain outlook, the softer macro backdrop compared with 2022, and the largely insurance-based nature of the expected hike. In other words, this could be the ECB’s only hike this year, delivered primarily to demonstrate its commitment to keeping inflation anchored.

Today, markets will parse May’s preliminary inflation readings for Germany and France, which will feed into next week’s aggregate print. Should a significant downside surprise fail to materially shift pricing for a hike in two weeks, it would reinforce the view that the move is more symbolic than substantively effective.

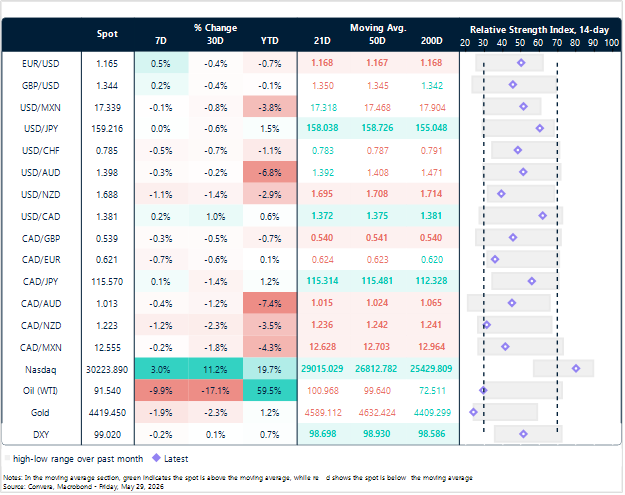

Market snapshot

Table: Currency trends, trading ranges & technical indicators

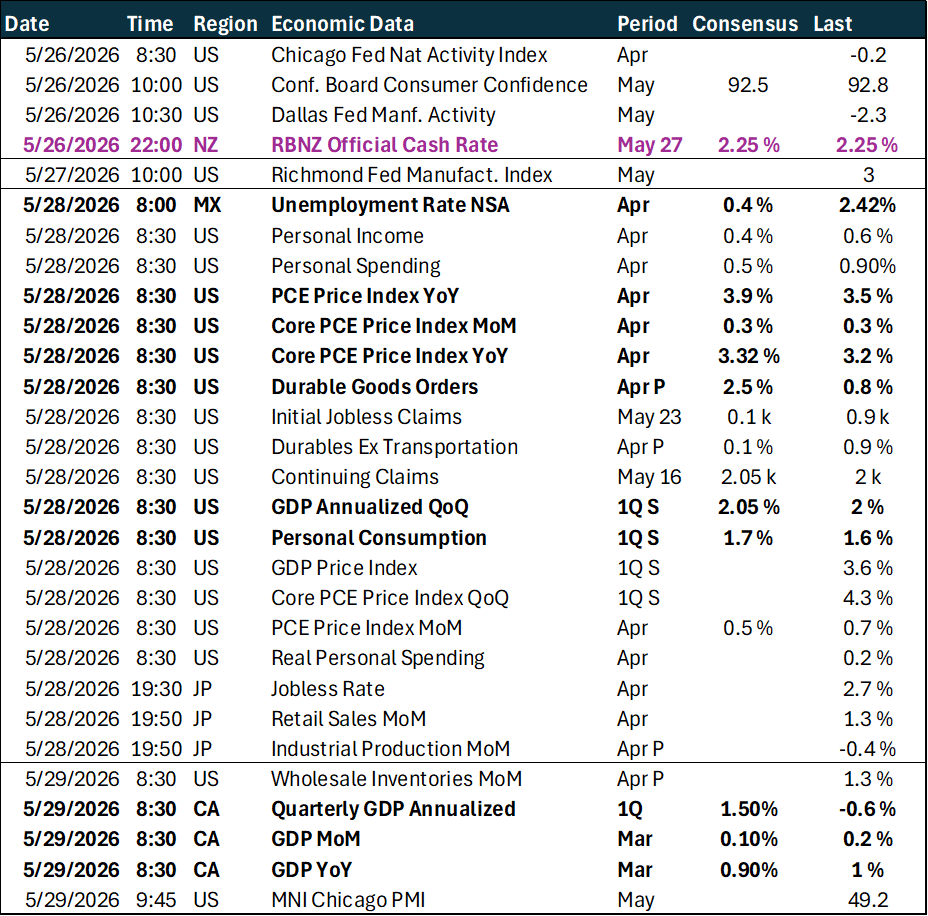

Key global risk events

Calendar: May 25 – 29

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.