GBP: Pound loses its floor

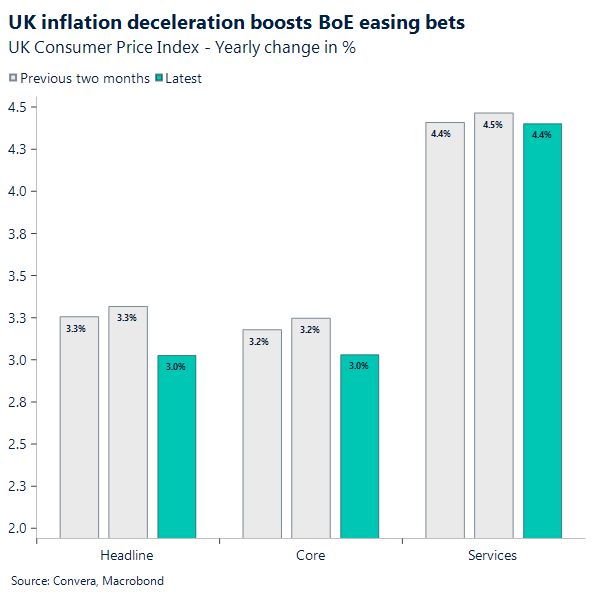

Sterling weakened across major pairs yesterday after a softer than anticipated labour market report, before steadying ahead of this morning’s inflation release. The data showed further signs of easing, but not enough to satisfy markets. Headline inflation fell from 3.4% to 3% as expected, while core and services measures fell by 0.1 percentage point to 3.1% and 4.4% respectively, which was not as low as consensus (3% and 4.3% expected). While the moderation broadly validates the Bank of England’s dovish tilt, anchored in its projected disinflation path, stickiness in service inflation will have piqued hawks’ attention. Price action in GBP/USD and GBP/EUR remained relatively muted.

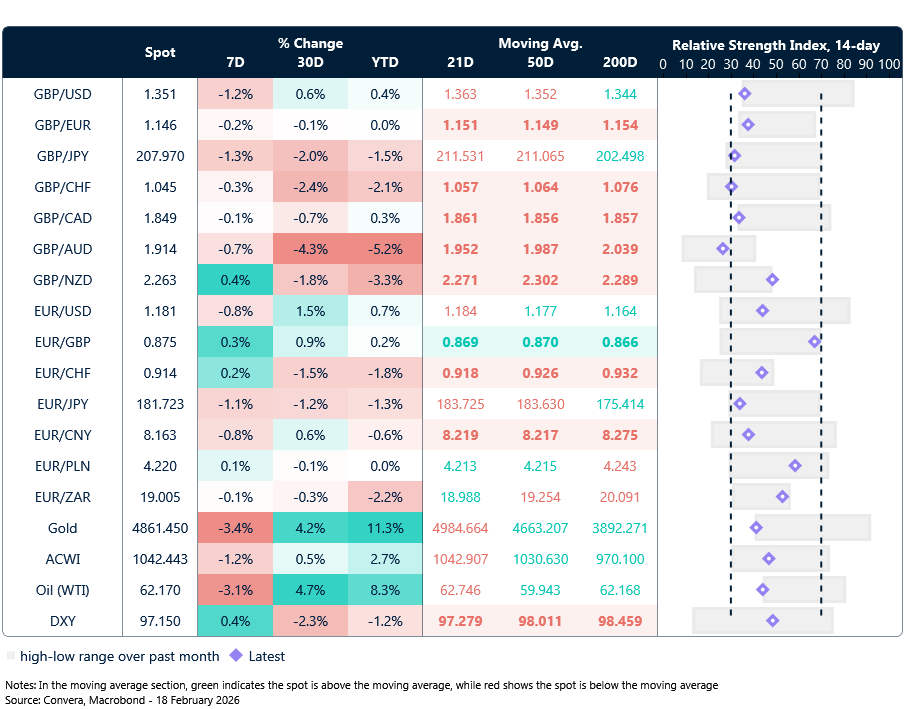

This is unsurprising. We had noted that the expected drop in headline inflation was large and already priced in, limiting the scope for additional bearish pressure unless the print surprised to the downside. Sterling also absorbed heavier selling in yesterday’s session, setting the bar higher for fresh downside momentum. In fact. GBP/EUR closed below the 100‑day moving average yesterday, which had held as key support since December, while also closing below the most recent higher low at 1.1440 from 9 February. This marks the invalidation of the steady bullish uptrend the pair had been on since November. While this evolution in the pair’s technical setup is not necessarily indicating an imminent bearish reversal, it is signalling growing vulnerability to downside risks for sterling.

In GBP/USD, the pair found support at the 50‑day moving average yesterday after falling 0.4%, with the dollar drawing strength from renewed Middle East tensions. That support looks less robust than the technical structure in GBP/EUR, as the move lower in cable continues to be driven by an unwinding of crowded shorts against the dollar. For the remainder of the week, retail sales and PMIs on Friday will be key. The latest readings were a pleasant surprise, and a confirmation of that momentum could help limit sterling’s vulnerability to further selling for the week.

USD: Steady ahead of key Fed signals

The US dollar index has firmed above 97, helped in part by a sharp slide in the New Zealand dollar after the RBNZ held rates steady and markets pared back tightening bets. Attention now turns to the Fed’s meeting minutes, which land against a backdrop of strong jobs data and softer inflation that have shaped expectations around how quickly policymakers can pivot.

Geopolitics adds another layer: the US and Iran reached an understanding on “guiding principles” in their indirect nuclear talks, though a full agreement remains distant. Oil’s inability to rebound has capped USD upside, while US equity futures and Asian stocks have stabilised as the AI‑driven sell‑off eases.

US durable goods and industrial production are in focus today, offering a timely read on the strength of US demand and manufacturing at a moment when markets are primed to trade weak data asymmetrically. Softer prints would reinforce the view that the economy is losing momentum and keep the dollar under pressure, while any resilience would challenge the dovish narrative that has taken hold. We also have the Fed’s minutes from last month’s meeting to digest — a chance to gauge how aligned policymakers really were around the recent shift in tone and whether the bar for rate cuts is lower than Powell suggested.

EUR: Lagarde expected leave ECB early

The euro is slightly softer this morning, with only a muted reaction to reports that ECB President Christine Lagarde may step down before her term ends in 2027. The lack of market response suggests investors are weighing not just the prospect of a more hawkish successor, but also the risk of a leadership vacuum at a delicate point in the policy cycle. Isabel Schnabel has been floated as a potential candidate, though Lagarde has previously noted that legal advice indicates sitting Executive Board members may be ineligible for the presidency.

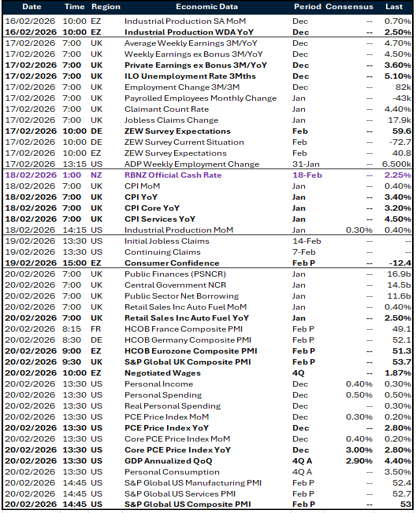

On the data front, Germany’s ZEW survey slipped to 58.3 in February from January’s four‑year high, well below expectations. The broadly steady but softer reading underscores how fragile the recovery remains in Europe’s largest economy, with structural drags in industry and investment still unresolved.

Near term, EUR/USD continues to trade above fair value and looks vulnerable to a drift lower in the absence of a clear catalyst. That said, with US data hardly convincing, sellers still lack a strong fundamental case for a sustained break lower. A dip through the 21‑day moving average around 1.1839 wouldn’t surprise, but the broader bullish configuration remains intact for now, with the February lows near 1.1766 offering solid support.

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

Calendar: February 16-20

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.