Markets hopeful ahead of Trump speech

Global markets were mostly higher for a second day as investors waited for a crucial speech from US President Donald Trump.

President Trump is due to speak at 9.00pm EDT (12.00pm AEDT). Markets are hoping for clarity around a potential deal between the US and Iran as the war nears its sixth week.

US equities gained for a second session, with the benchmark S&P 500 up 0.7%, while the US dollar fell. However, oil prices remained persistently high, with Brent and WTI crude both holding above USD100 per barrel.

In FX, a weaker USD drove moves. AUD/USD gained 0.4%, while NZD/USD rose 0.1%.

The euro and British pound were the best performers.

In Asia, USD/CNH fell 0.2%, while USD/SGD lost 0.3%. USD/JPY was flat.

Away from geopolitics, markets are looking ahead to Friday’s US non‑farm payrolls report. After a stronger‑than‑expected ADP reading, markets are expecting 65k new jobs, with the unemployment rate seen steady at 4.4%.

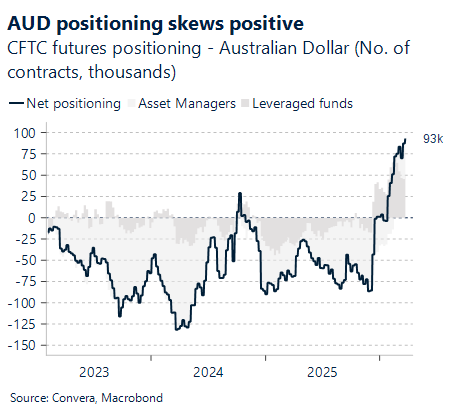

Aussie higher as cost pressures drive inflation worries

Australia’s S&P Global manufacturing PMI slipped into contraction in March, falling to 49.8 from 51.0. New orders dropped for the first time in five months as demand cooled and business confidence weakened.

Cost pressures intensified, with input prices jumping to their highest level in three and a half years, largely due to disruptions linked to the Middle East conflict. New export orders provided a rare bright spot, rising at the fastest pace since May 2021, but weaker domestic demand continued to weigh on overall activity.

Whether AUD/USD can extend its recovery will hinge on how long geopolitical tensions keep energy and input costs elevated.

AUD/USD has rebounded over the past two sessions. The next hurdle sits near the 50‑day average at 0.6964, followed by the 21‑day average at 0.6981.

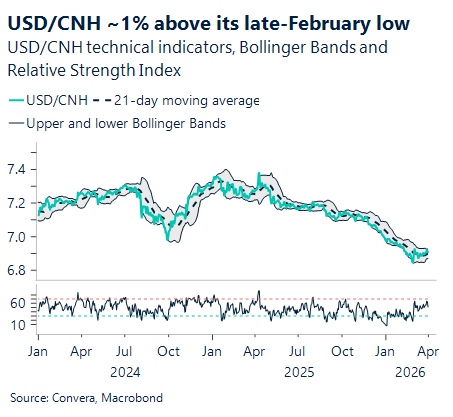

USD/CNH at three‑week lows as China loses momentum

China’s RatingDog manufacturing PMI eased to 50.8 in March, below expectations and down from 52.1. The official PMI showed a modest improvement at 50.4, but the broader picture remains mixed.

RatingDog flagged a tougher operating environment, with policymakers opting for a flexible 4.5%–5% growth target while stopping short of large‑scale support measures. At the same time, geopolitical strains are keeping oil prices elevated and raw material markets unstable, which is likely to push imported costs higher.

USD/CNH has pulled back as the USD softened. The next resistance area comes in near the 50‑day average at 6.9160, followed by the 100‑day average at 6.9624.

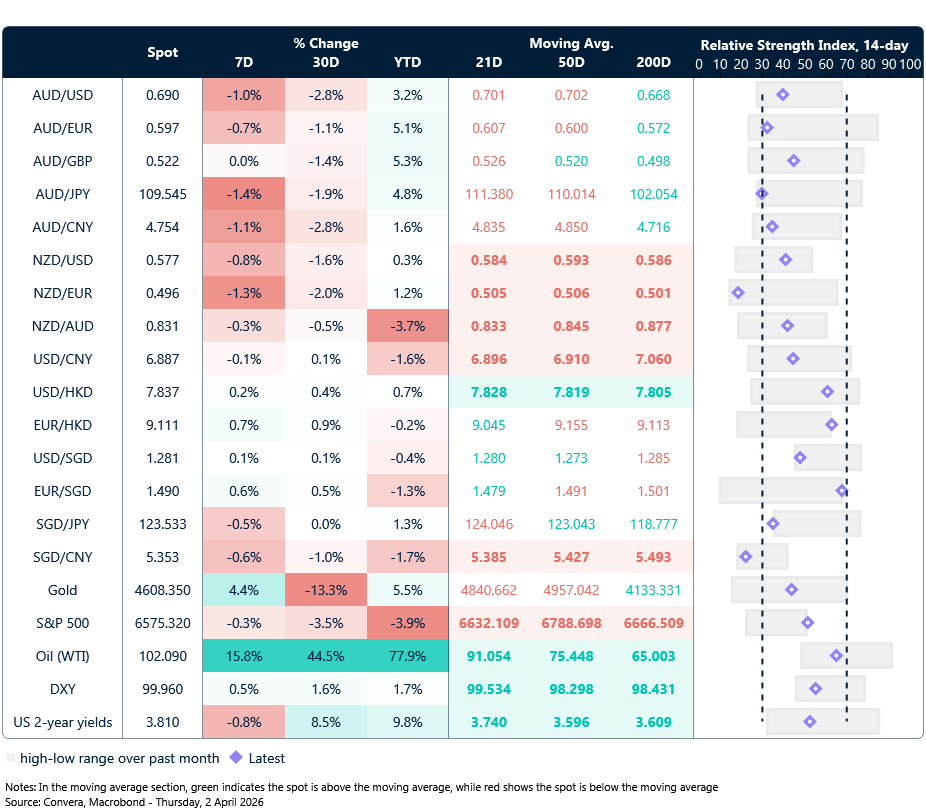

Greenback extends drop from ten-month highs

Table: seven-day rolling currency trends and trading ranges

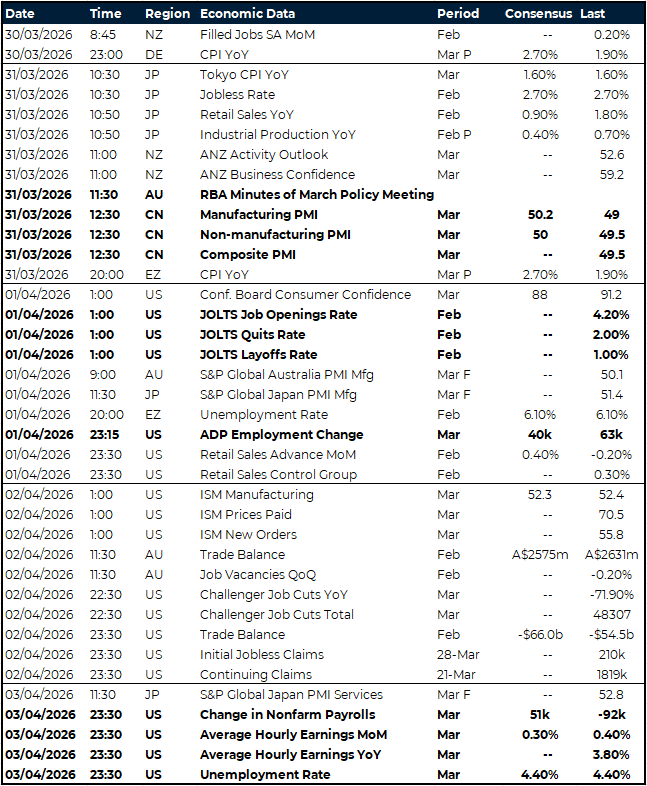

Key global risk events

Calendar: 30 March – 3 April

All times AEDT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.