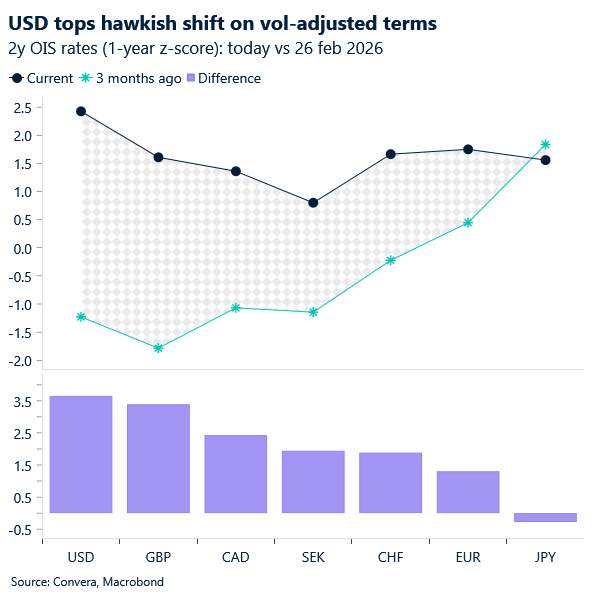

USD: Dollar range-bound as narratives struggle to advance

The Dollar Index – the DXY – has failed to reclaim the 99.400 mark since mid-May, as markets appear increasingly willing to look through bouts of re-escalation – Monday night’s US-Israeli strikes being the latest example – while continuing to cling to the de-escalation story. Meanwhile, the US dollar is becoming more responsive to the growth and rates narrative. This week’s bull steepening – with the front end of the curve falling more than the long end – following some unwinding of Friday’s sharpest Fed hawkish repricing since early 2025, may have contributed to the greenback’s paralyised posture.

That said, the move still feels more positioning-driven than fundamentally warranted. While markets are leaning on the de-escalation narrative, a more sustained unwind likely requires more concrete progress on peace. This is especially true as markets increasingly shift their focus to the macro and policy implications of the conflict, which makes any unwind in the dollar/Treasuries dynamic inherently stickier in the near term. It is useful reminder that both the April CPI and PPI reports came in above expectations, and that markets priced in one full 25bp rate hike on Friday. Against this backdrop, we struggle to see the DXY breaking decisively below the 98 handle just yet.

A more forceful bullish impulse also appears unlikely in the near term either, given the lingering de-escalation narrative, coupled with the still relatively homogeneous “tough talk” from G10 central banks that masks a more dovish-leaning macro backdrop (see eurozone).

Instead, more subdued DXY price action in the lower 99 range appears more likely, as markets await more tangible progress from the de-escalation narrative.

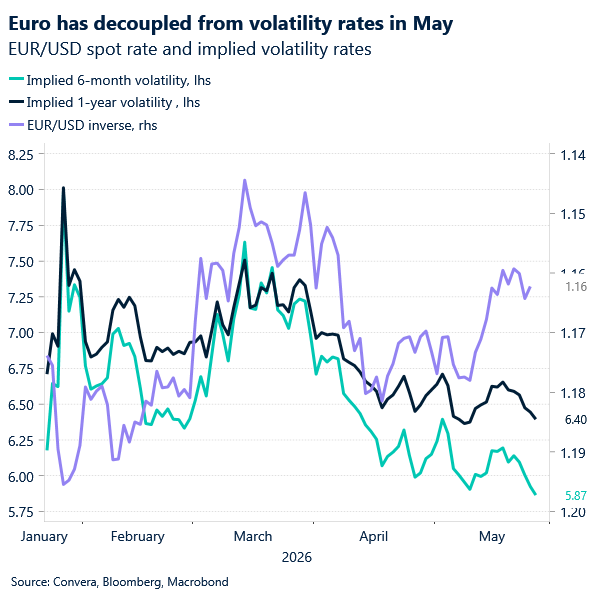

EUR: Losing carry in a low-vol world

EUR/USD continues to trade in a narrow 1.16–1.18 range, with price action increasingly subdued as FX volatility grinds lower. Despite ongoing uncertainty surrounding the Middle East, markets have become notably desensitised to conflicting headlines, with geopolitical developments generating diminishing marginal impact on the currency pair.

This low‑volatility backdrop has important implications for positioning. In an environment where directional conviction is limited, carry considerations tend to dominate, and here the euro is losing ground. While the single currency briefly benefited from a relatively attractive rate profile earlier in the spring, that support has eroded. Market pricing for ECB tightening has been scaled back meaningfully, with expectations falling from around 85bp at end‑April to closer to 55bp currently.

At the same time, the macro picture has softened. Euro‑area data surprises have deteriorated sharply relative to the US, reinforcing a widening growth and policy divergence. Real yield differentials have moved back in the dollar’s favour, and underlying economic momentum remains more resilient in the US than in the eurozone.

What is notable, however, is that EUR/USD has yet to fully reflect this shift. The dominant pro‑risk market narrative – characterised by firm equities and compressed volatility -continues to suppress broader dollar strength, allowing the euro to hold its ground despite weaker fundamentals. This creates a growing disconnect. Rates and growth differentials point to euro downside, but the risk‑supportive environment is preventing a more decisive move.

For now, EUR/USD remains range‑bound. But as carry regains importance and macro divergence persists, the balance of risks is gradually tilting lower, even if the adjustment remains slow in a compressed volatility regime.

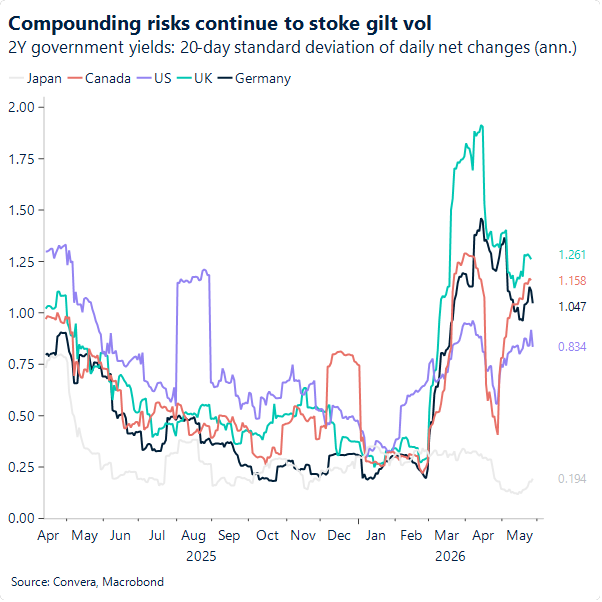

GBP: Gilt volatility keeps GBP on edge

As well put by my colleague George Vessey in yesterday’s note on the pound, “sterling looks stable but not strong.” The unwinding of the political risk premium appears to be fading, with GBP/EUR reapproaching the familiar 1.16 resistance line and settling just below it. Some may argue this has been quite a swift rebound, given the rather bleak local election outcome for the Labour Party and the heightened risks of a leadership challenge to PM Keir Starmer that followed. There is a significant element of this having already been well priced in, while reassurances on fiscal discipline from Andy Burnham have helped curb further gilt sell-offs driven purely by domestic pressures.

The positioning clean-up has been accompanied by a gradual unwind of hawkish market bets on the BoE’s 2026 policy outlook, which had stemmed from the de-escalation narrative. Markets now price in just under two hikes by year-end, down from highs of around three earlier in May. The UK bond market therefore continues to appear susceptible to more volatile moves, driven by the compounding effects of geopolitical tensions and domestic politics. Risks for further downside, however, appear more subdued rather than fully dissipated, suggesting that additional gilt sell-offs remain possible. Sterling, in turn, remains vulnerable, albeit asymmetrically, as bouts of geopolitical re-escalation tend to affect euro markets to a similar magnitude.

Against this backdrop, the near-term outlook for GBP/EUR appears relatively quieter compared to GBP/USD, where the geopolitical “add-on” is likely to be expressed more forcefully. For the week, we see 1.15 as a comfortable range for GBP/EUR to navigate, while GBP/USD could breach 1.35 should de-escalation momentum build more convincingly from here.

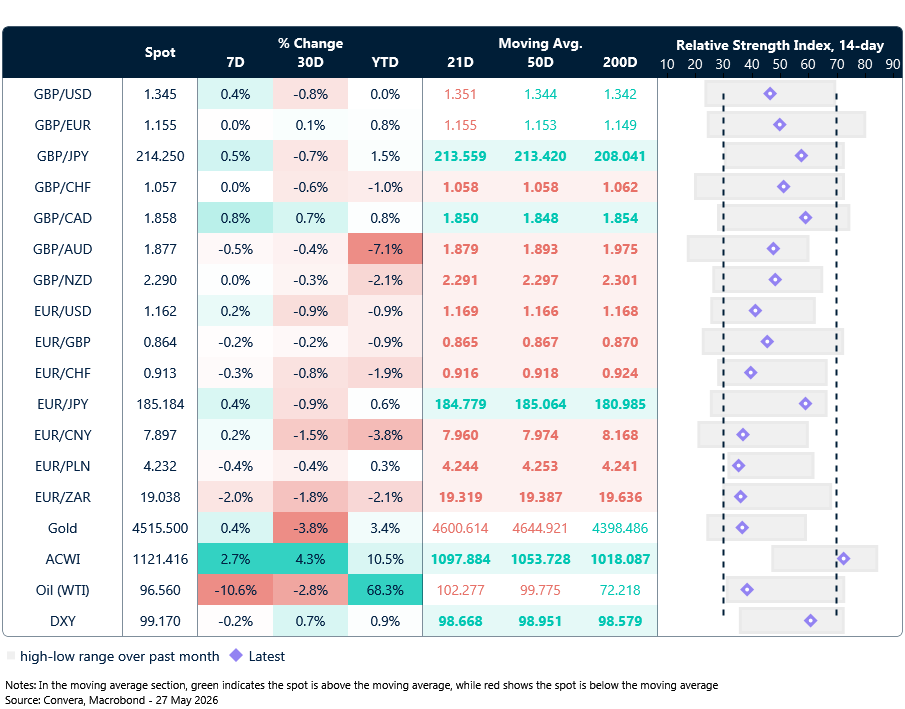

Market snapshot

Table: Currency trends, trading ranges & technical indicators

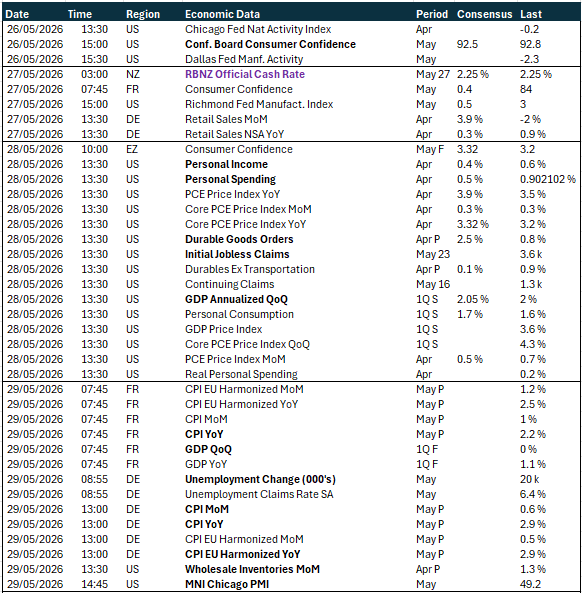

Key global risk events

Calendar: May 25-29

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.