USD: From war premium to peace trade

Global equities reached new highs as signs the US and Iran may extend the ceasefire helped markets unwind war-related risk premia. The MSCI All Country Index has erased its roughly 9% conflict-era drawdown, while Brent crude is down nearly 20% this month and the US dollar index sits close to six‑week lows.

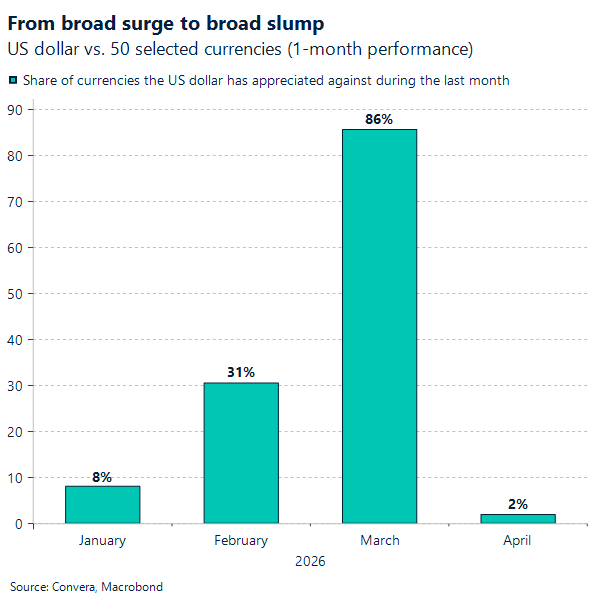

The dollar remains under pressure as markets continue to price a more constructive geopolitical outcome, steadily stripping out the premium that built through March. With investors increasingly inclined to believe that renewed talks between the US and Iran can prevent a fresh escalation, demand for defensive dollar exposure has faded, while firmer equities, lower volatility and a retreat in oil have all reinforced the move back towards risk-sensitive assets. That broader reversal is also visible in the cross-section: after appreciating against almost 90% of our 50-currency basket in March, the USD has risen against just 2% so far this month, with the heaviest G10 losses concentrated against the Antipodeans, the Scandis and sterling.

What matters more is that the recent move still looks more tactical than structural. Some of the March dollar strength had clearly become crowded, leaving the currency vulnerable once the geopolitical backdrop began to improve. But the broader market was never positioned for an outright dollar squeeze higher over a longer horizon. That helps explain why the reversal has been sharp without yet suggesting a deeper regime shift.

The rates backdrop still argues against a fuller dollar collapse. US inflation remains stickier than in most peer economies, and the Fed has shown little urgency in forcing inflation rapidly back to target. As long as the US retains a relative yield advantage, the dollar may stay vulnerable to near-term optimism, but it is unlikely to become unanchored from medium-term support.

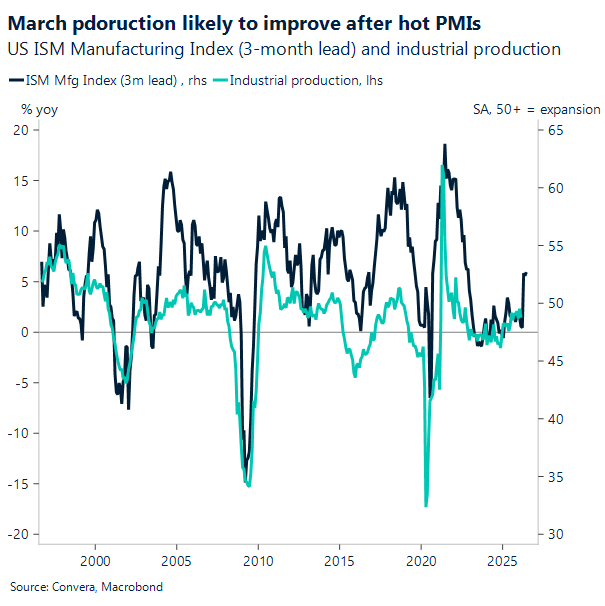

On the data front, March industrial production is expected to rise 0.1% m/m, easing from February’s pace. Survey and labour data suggest factory activity remains on an improving trajectory, even as supply-chain disruptions continue to pose near-term risks.

EUR: Sentiment improves, but proof still pending

The week has so far seen a steady mending of optimism, as both the US and Iran have refrained from resuming strikes while showing an inclination toward further talks. President Trump’s comments earlier in the week – that the war may be “close to over” and that discussions between the two sides could resume “over the next two days” – helped lift market sentiment. Iran’s apparent consideration of pausing shipments through the Strait, in order to avoid testing the US naval blockade and jeopardising renewed negotiations, has so far been interpreted as one of its clearest non‑verbal signals of “willingness to talk.”

That said, markets are growing increasingly impatient, and yesterday’s reversal of March’s trends – USD lower, EUR higher – proved more muted and contained. Against the backdrop of highly volatile headline flows that have whipsawed sentiment throughout March, investors have become more demanding of substantive evidence that talks are genuinely progressing and, most importantly, that the strait is close to re-opening.

It remains unclear how a return to a no‑conflict scenario would ultimately affect the US dollar. As the mechanical lift tied to rising energy prices and deleveraging flows dissipates, USD sentiment is likely to remain soft, with the Iran conflict simply adding to the broader list of “erratic policy events” that have weighed on the dollar since Trump took office last year (think “Liberation Day”). That said, market memory is often short, and investors have also shown signs of having grown more accustomed to Trump’s modus operandi since the start of his second term. We believe the US macro outlook – and how it absorbs any fading conflict‑driven drag – will remain the more pressing focus for markets, helping to keep the downside in the dollar contained should the US growth engine continue to show resilience.

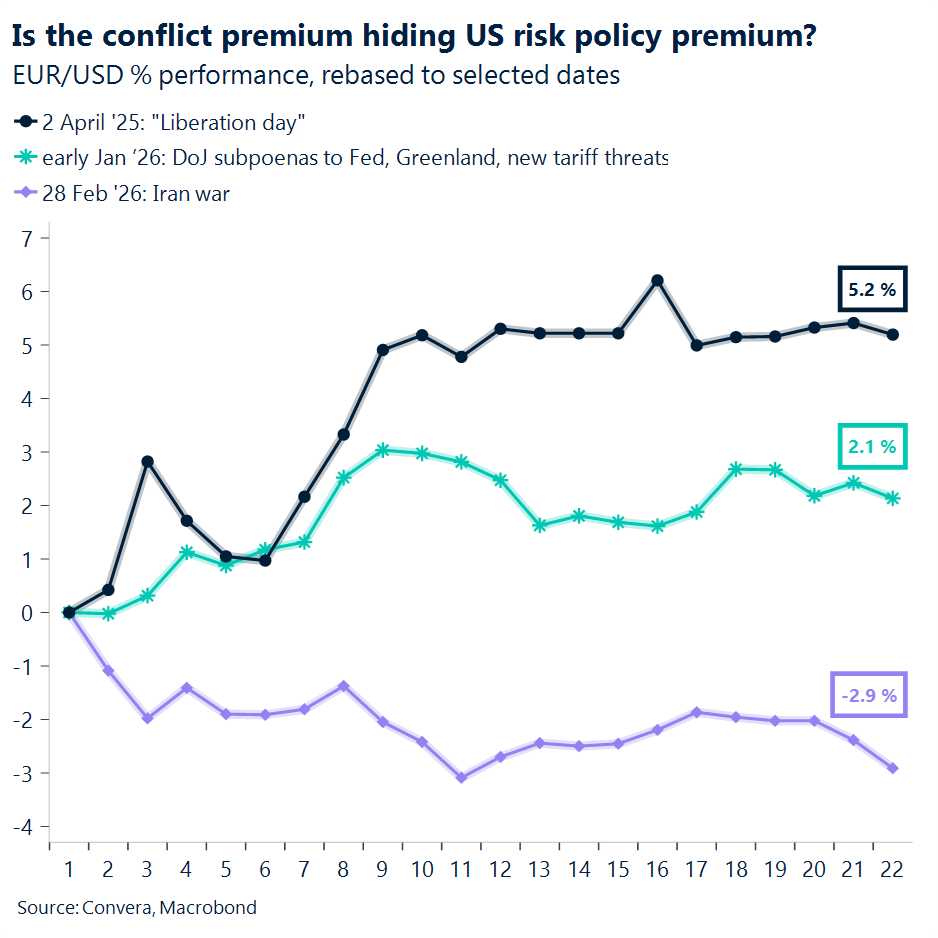

For now, EUR/USD has stopped short of breaking through 1.18 – understandably so, as more concrete signs of de‑escalation are still warranted. The level has acted as key resistance since the pair’s post‑“Liberation Day” (2 April 2025) price action, reinforcing the view that a sufficiently strong catalyst to justify a clean breakout has yet to materialise.

GBP: Pre‑war GDP surprise, but outlook fragile

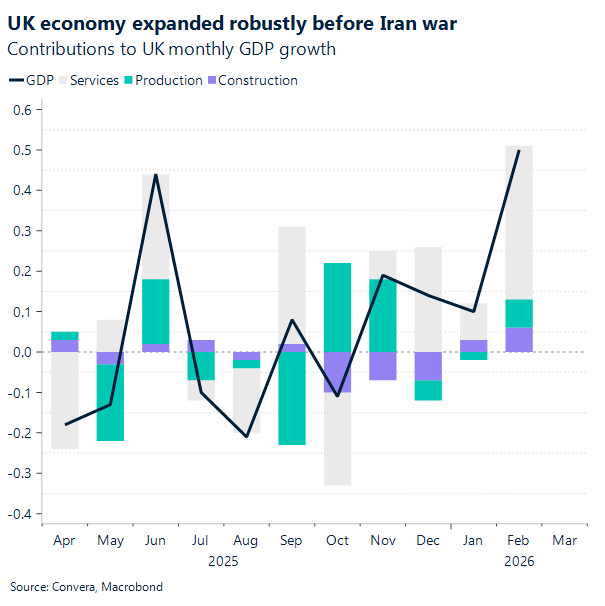

Sterling received a modest additional lift this morning following a stronger‑than‑expected UK GDP print. GBP had already been supported by falling oil prices and improved global risk appetite, unwinding much of its conflict‑era losses against the dollar and extending gains toward 1.36.

February GDP rose 0.5% m/m, well above the 0.1% consensus, and the strongest monthly increase since January 2024, highlighting that underlying momentum in the UK economy was firmer than appreciated ahead of the Middle East escalation. Growth was broad‑based, led by a fourth consecutive expansion in services, with production and construction also contributing.

That said, the data largely reflects pre‑war conditions and does little to offset the forward‑looking risks. A prolonged conflict threatens to hit the UK disproportionately via higher energy costs, renewed inflation pressure, and tighter financial conditions. With inflation risks still skewed to the upside and growth forecasts being downgraded, the macro backdrop remains fragile. As such, while today’s GDP surprise offers near‑term support for sterling, it is unlikely to materially alter the medium‑term outlook unless geopolitical risks continue to ease.

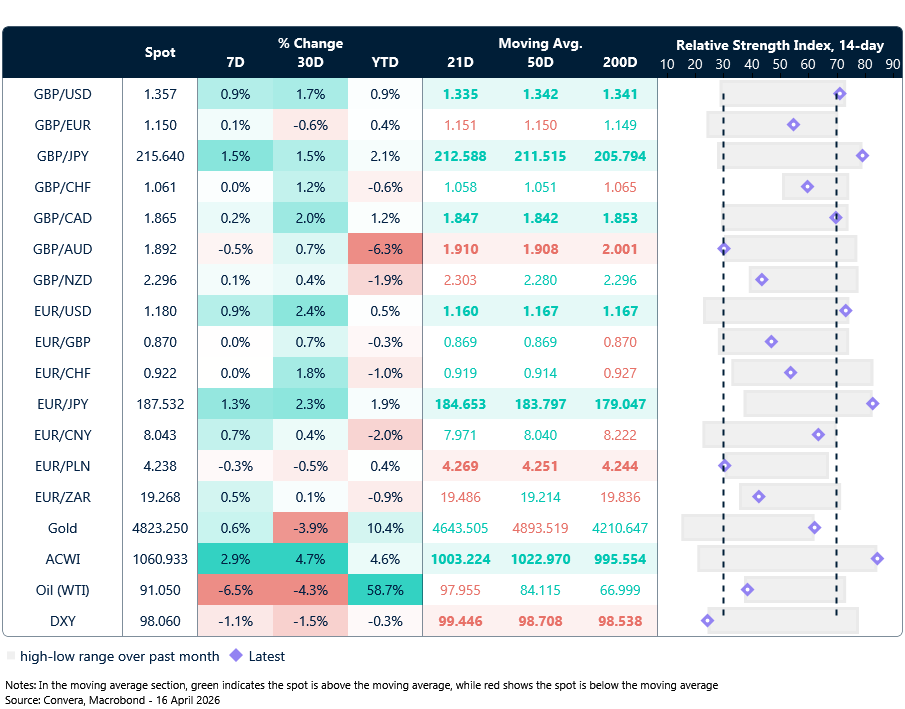

Market snapshot

Table: Currency trends, trading ranges & technical indicators

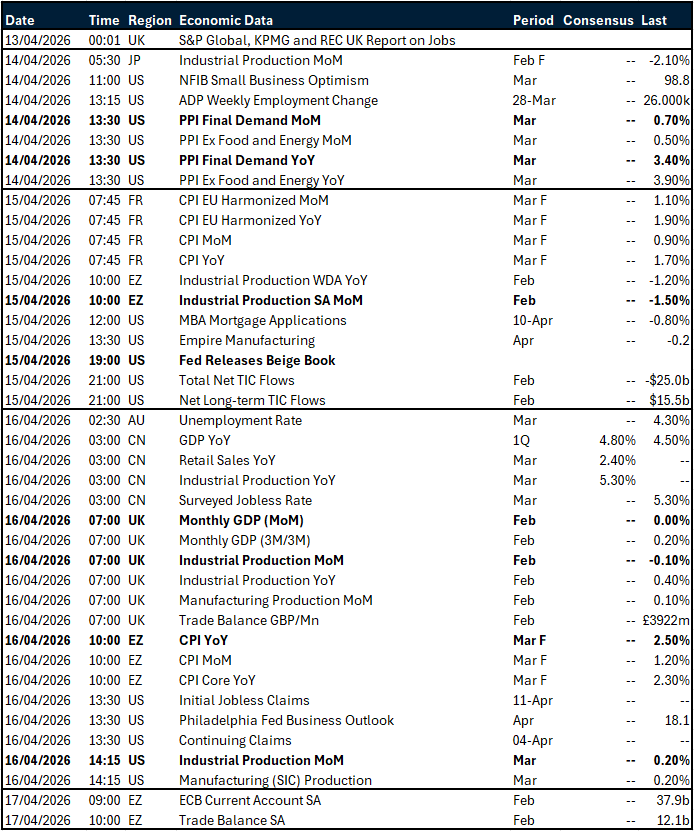

Key global risk events

Calendar: April 13-17

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.