- Shutdown standoff. The clock continues to tick on the US government shutdown, which has dragged into its third week, threatening broader economic fallout.

- Inflation miss. US inflation rose less than expected to 3% in September, sending yields lower and hitting the dollar across the board.

- Fed cuts cemented. Markets are fully pricing in a cut by the Federal Reserve over the coming days and 50bp in total by year-end. However, without any jobs data at hand, it will be hard to speculate much beyond the December meeting.

- Trade tensions. Trump ending trade talks with Canada adds to the grim outlook for CAD, but optimism over upcoming US-China trade talks has helped buoy global risk sentiment.

- USD resilience. The US dollar’s rebound extends, suggesting traders see recent trade headlines as more bark than bite and are betting that fundamentals will ultimately override the noise.

- Earnings roar. Strong industrials offset tech misses; 85% of S&P 500 firms beat profit estimates, further supporting risk appetite.

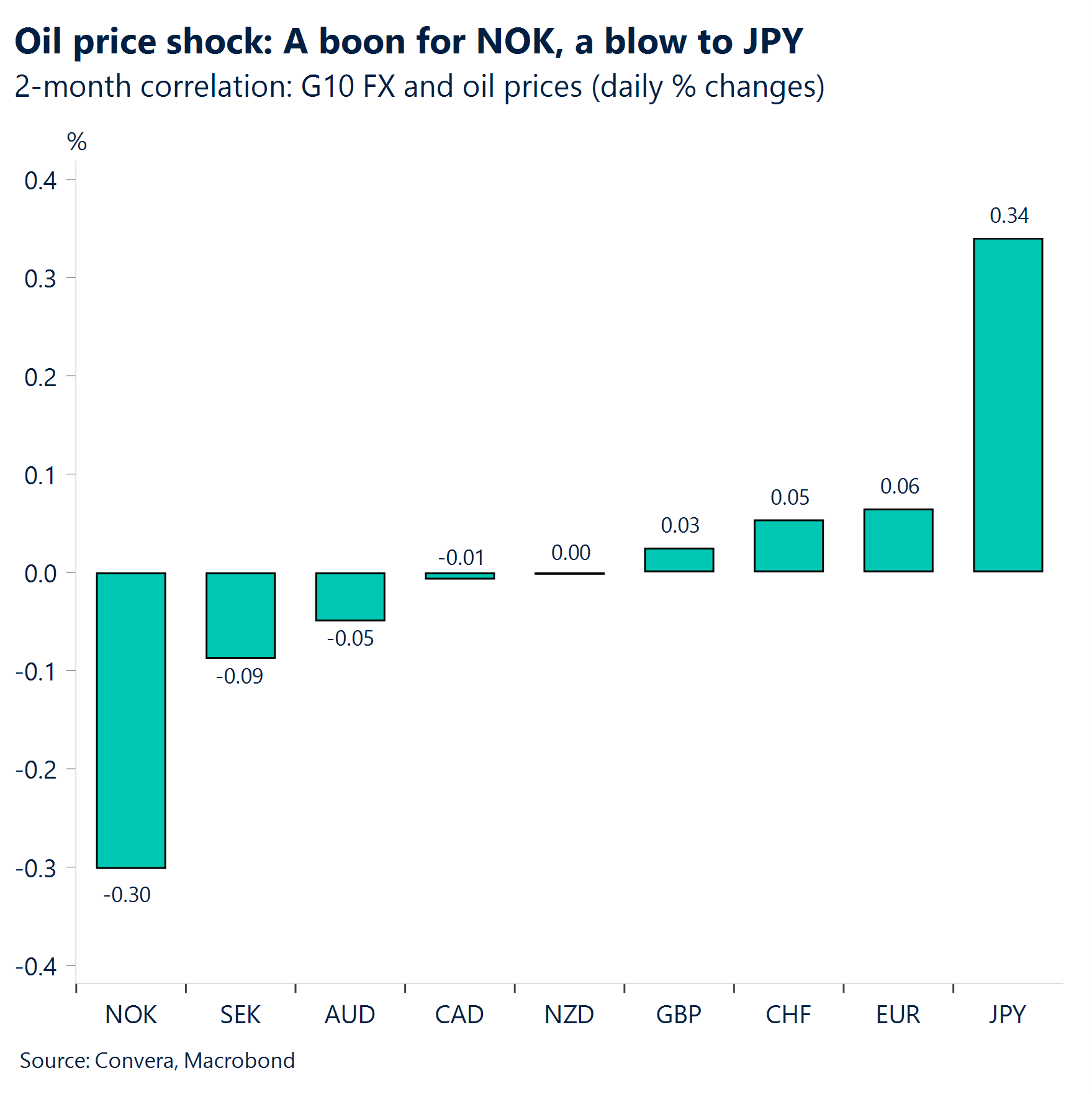

- Crude comeback. The spillover from US sanctions on Russia is pushing oil prices higher – up over 7% in a week – and that’s becoming a more potent FX driver. So far, the impact has been clearest in a rallying Norwegian krone and renewed pressure on the Japanese yen.

Global Macro

Metals melt down

US-China trade tensions. Reports that the White House was considering further export curbs related to US software products for China renewed concerns about an escalation in trade friction, particularly impacting the tech sector. President Trump and President Xi Jinping are expected to meet in Asia next week.

Inflation. The US CPI came in cooler than expected. Both the headline and core 12-month CPI changes came in slightly below forecasts at 3.0%. This almost certainly points to another rate cut from the Fed next week. In the UK, the annual inflation rate unexpectedly held steady at 3.8% in September (below 4% forecast), while Canada’s rate accelerated to 2.4% (above 2.3% forecast), creating a divergent picture that fueled bets for a Bank of England rate cut but tempered similar expectations for the Bank of Canada.

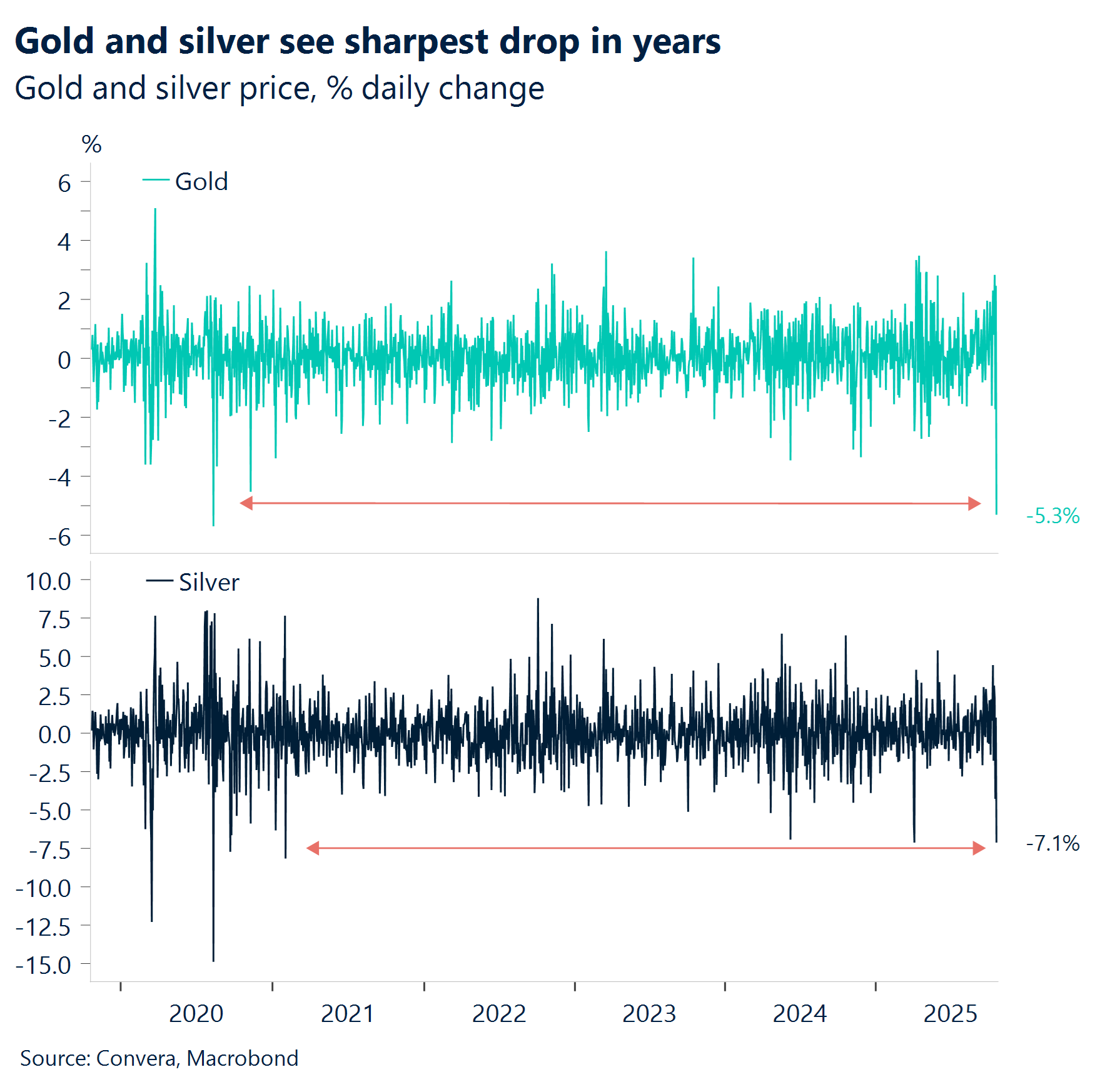

Momentum stalled. Gold and silver, fell 5.3% and 7.1% respectively in a single day, marking one of their sharpest drops in nearly five years.

US corporate earnings season update. Q3 US corporate earnings provided a mixed outlook for equity markets. Strong results from industrials (e.g., Honeywell, Union Pacific) and T-Mobile offered support. However, major tech disappointments dragged sentiment, notably a rare earnings miss from Netflix and a significant stock drop for Tesla following a sharp narrowing of profit margins. Despite individual misses, approximately 85% of S&P 500 firms reporting so far have surpassed profit estimates, placing the overall season on track for the best performance since 2021.

US shutdown. The 24-day US government shutdown, now the second-longest in history, shows no sign of ending. Its continuation poses a growing risk of measurably harming the broader economy.

Week ahead

Rate roulette

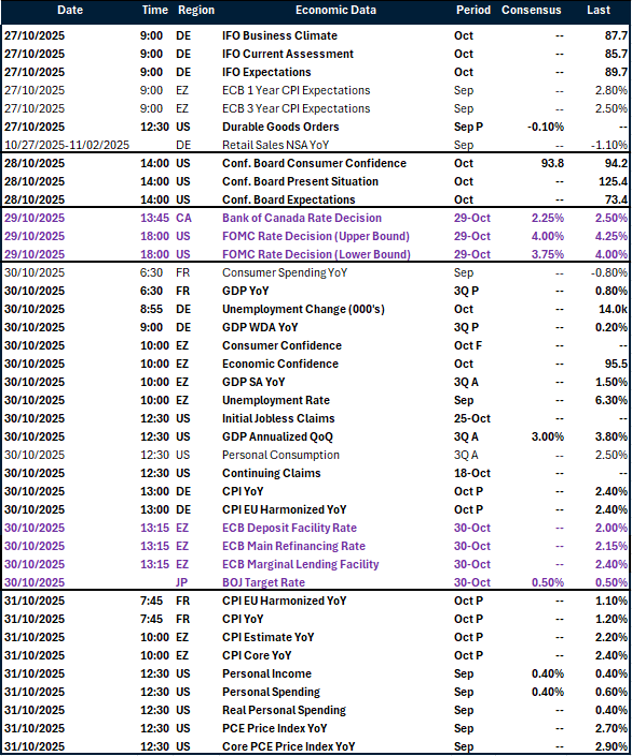

Shutdown’s data blackout. The U.S. government shutdown continues. Having started on October 1st, today marks its 24th day – making it the second-longest in U.S. history, surpassed only by the 35-day shutdown of 2018–2019. The data drought is set to deepen next week, stripping markets of key releases such as Q3 GDP, personal spending, and jobless claims.

Rate week, risky signals. It’s a pivotal week on the policy front, with Canada, Japan, the US, and the eurozone all set to announce rate decisions. For the ECB and the Fed, we expect – alongside broader consensus – a hold from the former and a cut from the latter. Crucially, we anticipate the Fed will pair the cut with cautious messaging, emphasizing that nothing is guaranteed for the December meeting- especially in light of the ongoing data blackout.

Eyes on the board. Amid the data blackout, Conference Board sentiment indicators will take centre stage. With October as the reference period, they’ll offer a crucial read on how the ongoing shutdown may have clouded consumer sentiment and expectations for the future.

Eurozone hard data pulse. Several hard data prints are due across the eurozone, including Germany and France. These releases will be key to gauging economic momentum and price pressures across the bloc, with the ECB remaining firmly focused on inflation for now.

FX Views

Dollar digs in

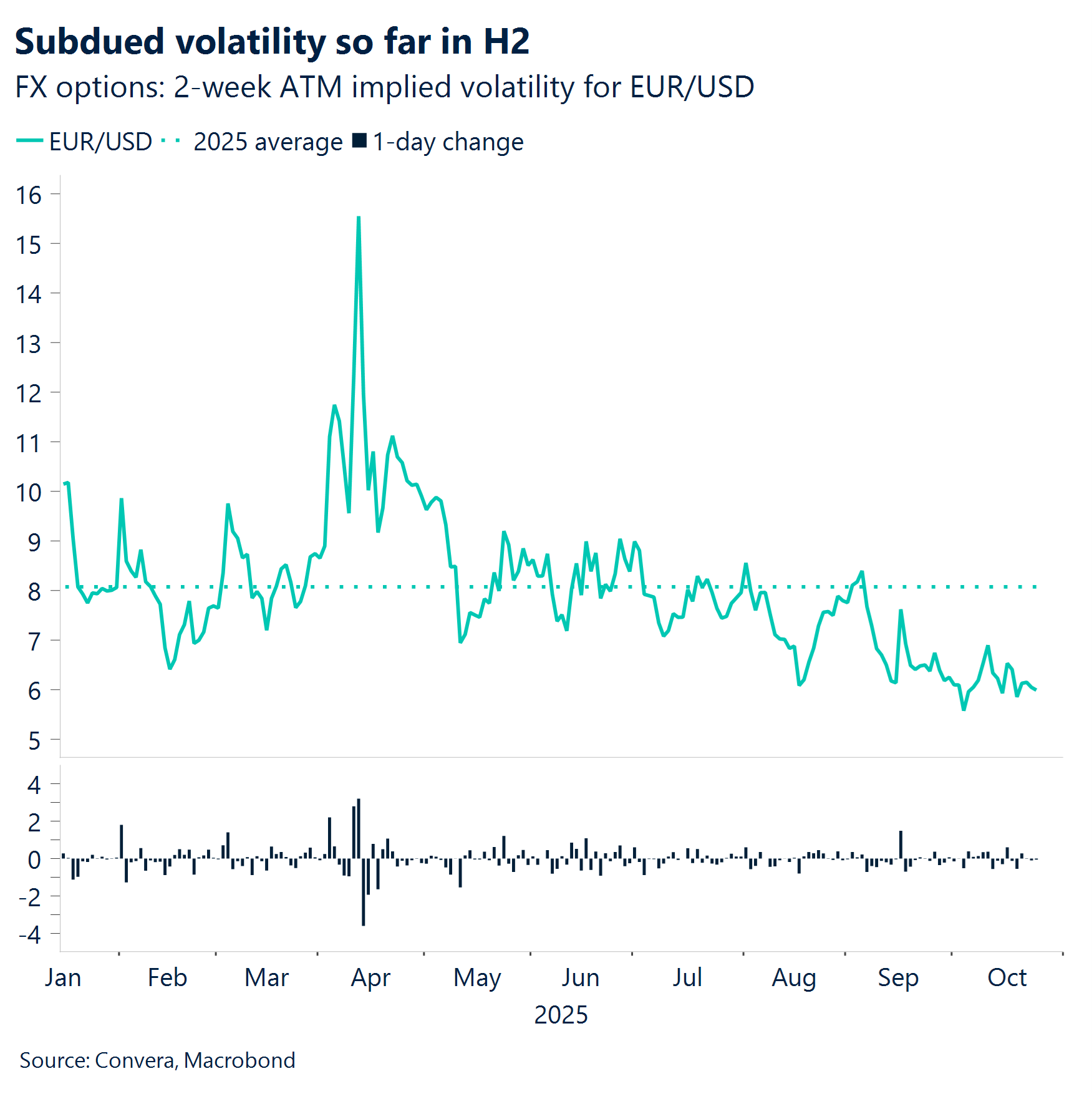

USD Dollar finds strength in the void. The dollar index is up 0.6% week-to-date, as this week brought fewer headline risks to shake confidence in the greenback – think credit concerns and China-US trade tensions from the week prior. The dollar’s recent resilience also stems from the lack of fresh data due to the ongoing shutdown. In Q3 earnings season, with the majority of S&P constituents beating analysts’ estimates, investors are taking this as a proxy for economic resilience – discounting, for now, what feels like a distant past of poor labour market data. This optimism inflates expectations, with the dollar likely to trend lower once data resumes and starts to disappoint. That said, the one-and-only BLS release – the inflation report – today missed expectations, sending yields and the dollar slightly lower across the board as Fed bets on two Fed rate cuts before year-end were cemented. That said, we continue to expect a stronger dollar into month-end: alongside a likely cut, cautious language is expected to follow – just as we saw in September, when such messaging helped lift the dollar.

EUR Catalyst vacuum, downside risk. The euro traded lower against the dollar this week, down 0.4%, and over 1% month-to-date. France’s political risk premium remains elevated, as evidenced by the FR-DE 10-year spread still hovering around 80 basis points. S&P Global’s downgrade of France last Friday set the euro on a softer path for the week, reigniting concerns over the bloc’s second-largest economy and its still-fragile political backdrop. The euro’s descent was also justified by the absence of fresh catalysts from the very forces that fuelled its rally in the first half of 2025 – namely, USD weakness, whether via macro data or monetary policy. With the government shutdown ongoing, the Fed has now entered its blackout period ahead of the October policy meeting. EUR/USD is treading water at 1.16, but supported by the softer US inflation print preventing a break below this key level.

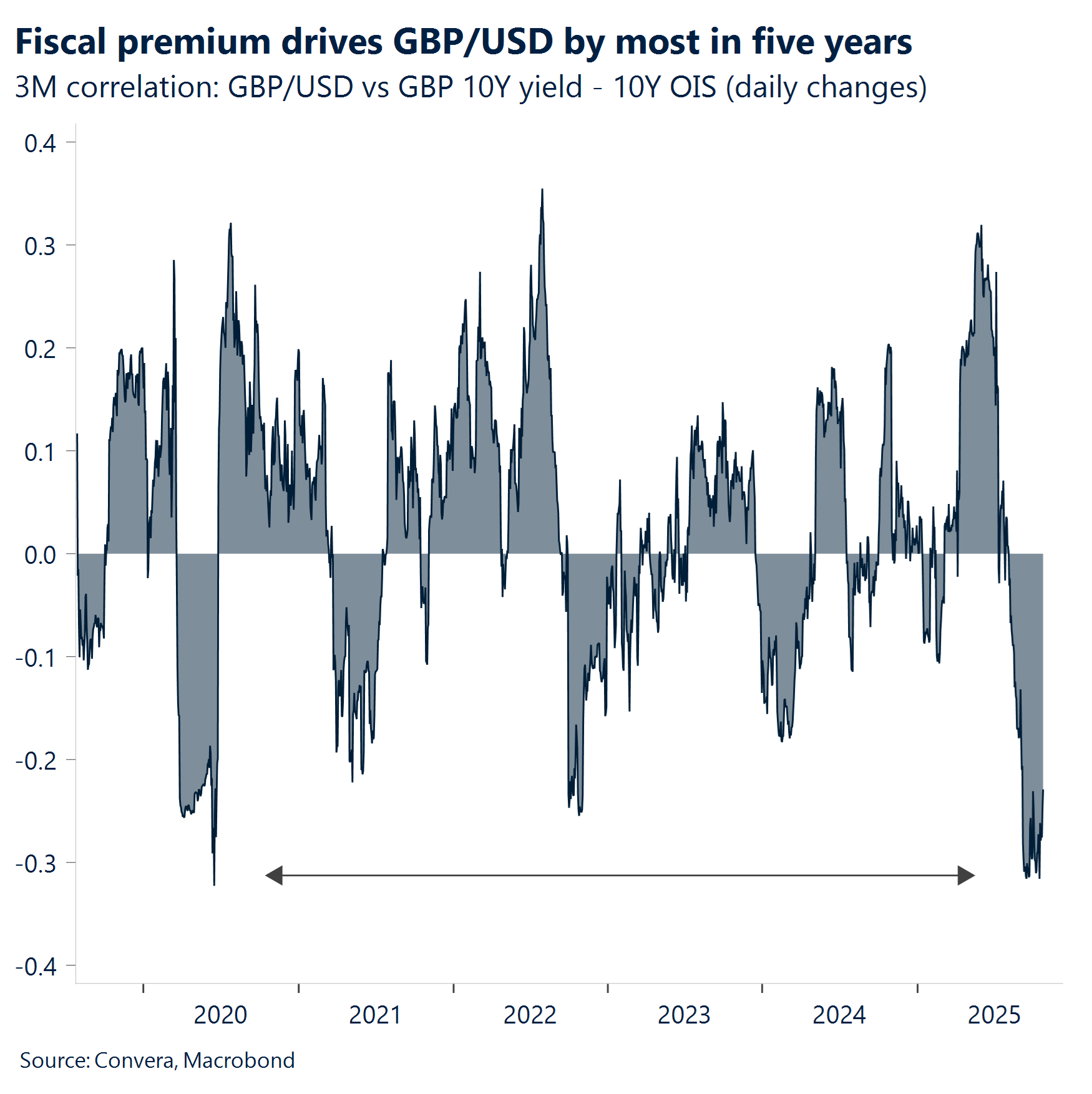

GBP On edge amid mixed signals. Sterling traded in choppy fashion this week as conflicting macro signals muddied the outlook. Softer-than-expected UK inflation reignited BoE easing bets, pushing December rate cut odds to nearly 70% and triggering a rally in front-end gilts. Yet stronger-than-forecast retail sales and a pickup in consumer confidence offered a counterweight, suggesting UK consumption remains resilient and potentially tempering dovish expectations. The pound’s reaction has been nuanced. While lower rates typically weigh on the currency, the UK still boasts one of the highest terminal rates in the G10, limiting downside. GBP/USD remains above its 200-day moving average near $1.32 — a key technical pivot. A break below would expose the August low at $1.31, with $1.30 the next major support. Options markets show rising demand for downside protection ahead of November’s Budget risk event. With sentiment fragile and macro risks building, sterling remains vulnerable to further weakness despite pockets of economic strength.

CHF Swiss missive. The Swiss National Bank’s first-ever policy summary offered little surprise, reaffirming its reluctance to cut rates below zero and showing limited concern over US tariffs. While the SNB reiterated its readiness to intervene in FX markets, it gave no fresh insight into its stance on the franc — a signal that policymakers remain cautious but not dovish. Thus, the franc continues to outperform, gaining around 1.1% against the euro so far in October and the only major to strengthen versus the USD this month. Elevated geopolitical risks and policy uncertainty abroad have reinforced the franc’s role as a safe-haven asset, driving demand and pushing EUR/CHF to near decade lows. Traders are increasingly paying up for put options that bet on EUR/CHF falling, rather than calls that anticipate a rebound — a clear sign of directional bias and protection against further CHF upside.

CNH Steady as she goes The remarkable low volatility nature of the Chinese yuan that has defined the market in 2025 has continued with the currency reaching a one-month highs during the week. Amid ongoing political tensions between the US and China, the People’s Bank of China appears to be pursuing a “steady as she goes” approach in managing the yuan. USD/CNH remains in a clear downtrend, trading below key moving averages. The coming week could be a turning point for US-China relations, with President Trump scheduled to meet Chinese President Xi on the sidelines of the APEC summit on Thursday. However, past meetings have failed to materialize, keeping uncertainty elevated. For USD/CNH, topside targets are at 7.15 and downside targets at 7.10.

JPY Takaichi win hits yen The Japanese yen fell sharply over the past week following Sanae Takaichi’s historic win as Japan’s first female prime minister. Her pro-stimulus stance, support for “Abenomics,” and criticism of Bank of Japan rate hikes have sparked expectations of looser monetary policy, weighing on the JPY. USD/JPY surged back toward 153.00 — its highest level in two weeks — as traders priced in wider yield differentials and a delay in BoJ tightening. The next key level is seen at 153.30, marking eight-month highs. The yen’s biggest losses were against the commodity currencies. All eyes now turn to next Thursday’s Bank of Japan decision, which will be pivotal.

CAD Wobbling around 1.40. The Canadian Dollar’s recovery below the significant 1.40 level proved fleeting. However, a slightly softer-than-expected US CPI release offered a brief reprieve, nudging the USD/CAD pair back to 1.401. The pair is now poised to continue challenging the 1.40s range in anticipation of next week’s crucial Bank of Canada meeting. While a cut is expected, analysts remain split on whether it’s justified. With the target rate at 2.5%, near terminal, the September uptick in headline and core inflation may not be enough to prompt action. If the BoC holds, it would be a welcome surprise for Loonie bulls. A rate cut could prove the relief momentary and send the USD/CAD back at its highest level this month at 1.408.

AUD Steady against USD, mixed elsewhere. The Australian dollar held steady versus the US dollar over the past week but showed a more mixed performance across other markets. It posted strong gains against the Japanese yen and British pound, while slipping against Scandinavian currencies and the New Zealand dollar. With limited domestic data and little direction from the US, the Aussie largely responded to developments in other jurisdictions. AUD/USD remains in a short-term downtrend, trading below key 8- and 21-day moving averages and recently capped by resistance at 0.6525. Downside targets are to 0.6450. Looking ahead, upcoming inflation data could spark volatility in the AUD, with September-quarter CPI figures due on Wednesday. Headline annual inflation is forecast to climb from 2.1% to 3.0%, which would make a rate cut on 4 November less likely.

MXN Consolidation continues. The Mexican peso continues to trade within a relatively narrow range, but with a pattern of gradually higher highs, now approaching the 18.50 level. However, despite repeated attempts to break above the 50-day Simple Moving Average (SMA), the Mexican Peso has remained below this key medium-term trend indicator since April. There’s been broader weakness in emerging-market currencies, which briefly extended losses following a Reuters report that the Trump administration is considering restrictions on exports to China involving U.S.-origin software. The USD/MXN pair, which had posted strong year-to-date gains on the back of robust carry trade appeal, has now entered a phase of choppy, sideways consolidation around the 18.40 mark. While recent geopolitical tensions, including the U.S.-China trade spat, briefly pushed the Peso higher, its retreat reflects a return to low-volatility trading, with support from Mexico’s solid macro fundamentals and interest rate differential likely keeping the pair range-bound in the near term. For the short-term, the USD/MXN is expected to continue this range-bound crawl, holding year-to-date gains at 12%.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.